Videos

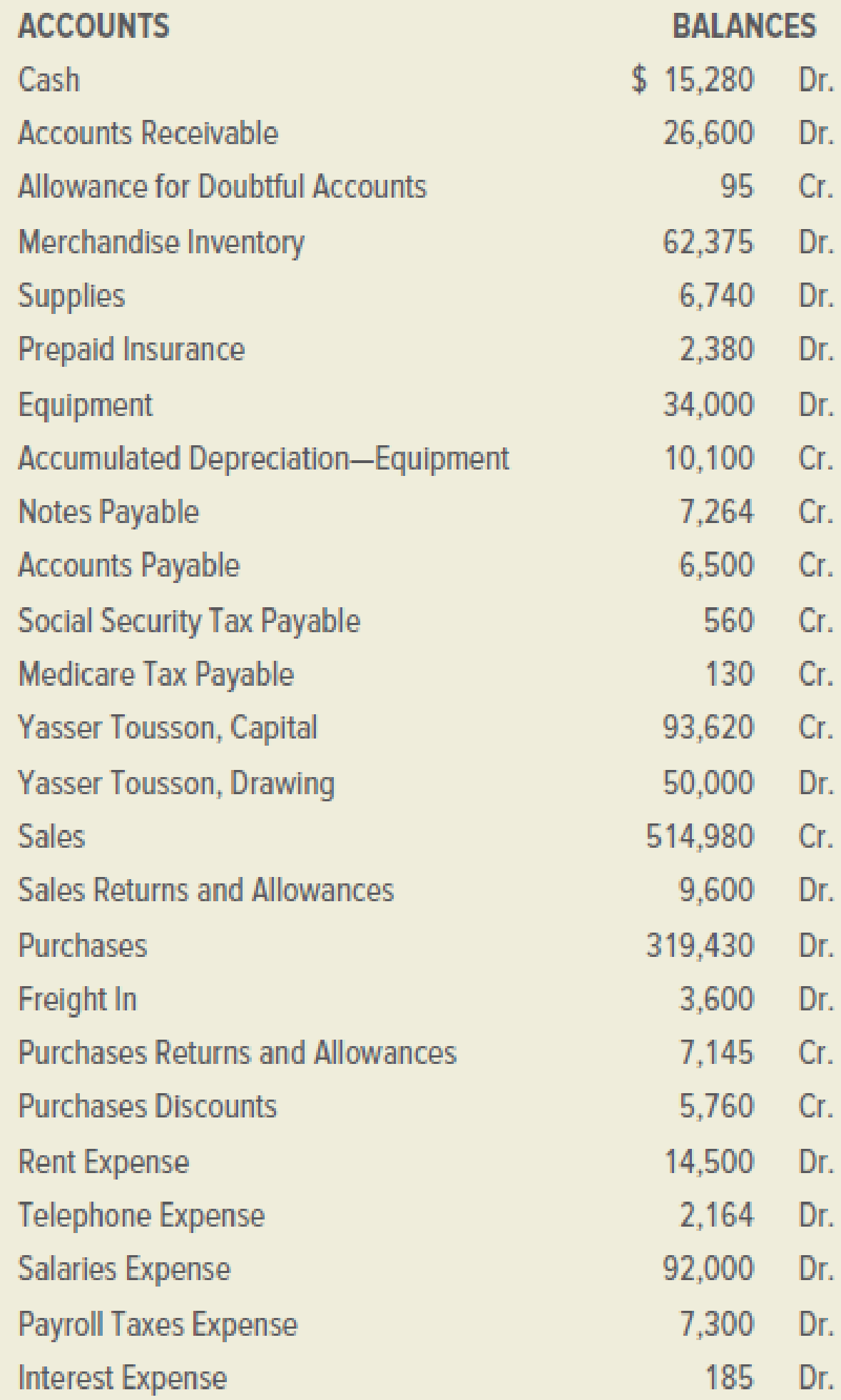

Programs Plus is a retail firm that sells computer programs for home and business use. On December 31, 2019, its general ledger contained the accounts and balances shown below:

The following accounts had zero balances:

The data needed for the adjustments on December 31 are as follows:

a.–b. Ending merchandise inventory, $67,850.

c. Uncollectible accounts, 0.5 percent of net credit sales of $245,000.

d. Supplies on hand December 31, $1,020.

e. Expired insurance, $1,190.

f.

g. Accrued interest expense on notes payable, $325.

h. Accrued salaries, $2,100.

i. Social Security Tax Payable (6.2 percent) and Medicare Tax Payable (1.45 percent) of accrued salaries.

INSTRUCTIONS

- 1. Prepare a worksheet for the year ended December 31, 2019.

- 2. Prepare a classified income statement. The firm does not divide its operating expenses into selling and administrative expenses.

- 3. Prepare a statement of owner’s equity. No additional investments were made during the period.

- 4. Prepare a classified balance sheet. All notes payable are due within one year.

- 5. Journalize the

adjusting entries . Use 25 as the first journal page number. - 6. Journalize the closing entries.

- 7. Journalize the reversing entries.

Analyze: By what percentage did the owner’s capital account change in the period from January 1, 2019, to December 31, 2019?

1.

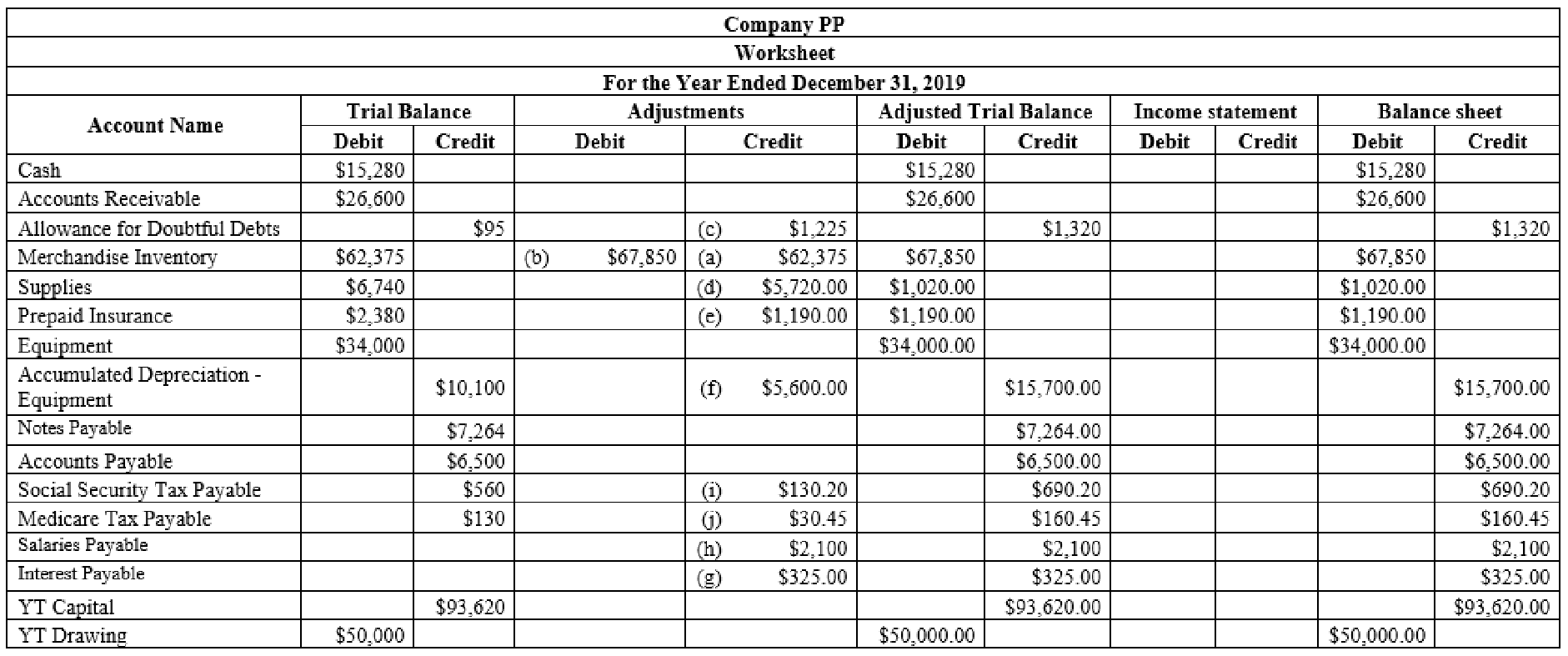

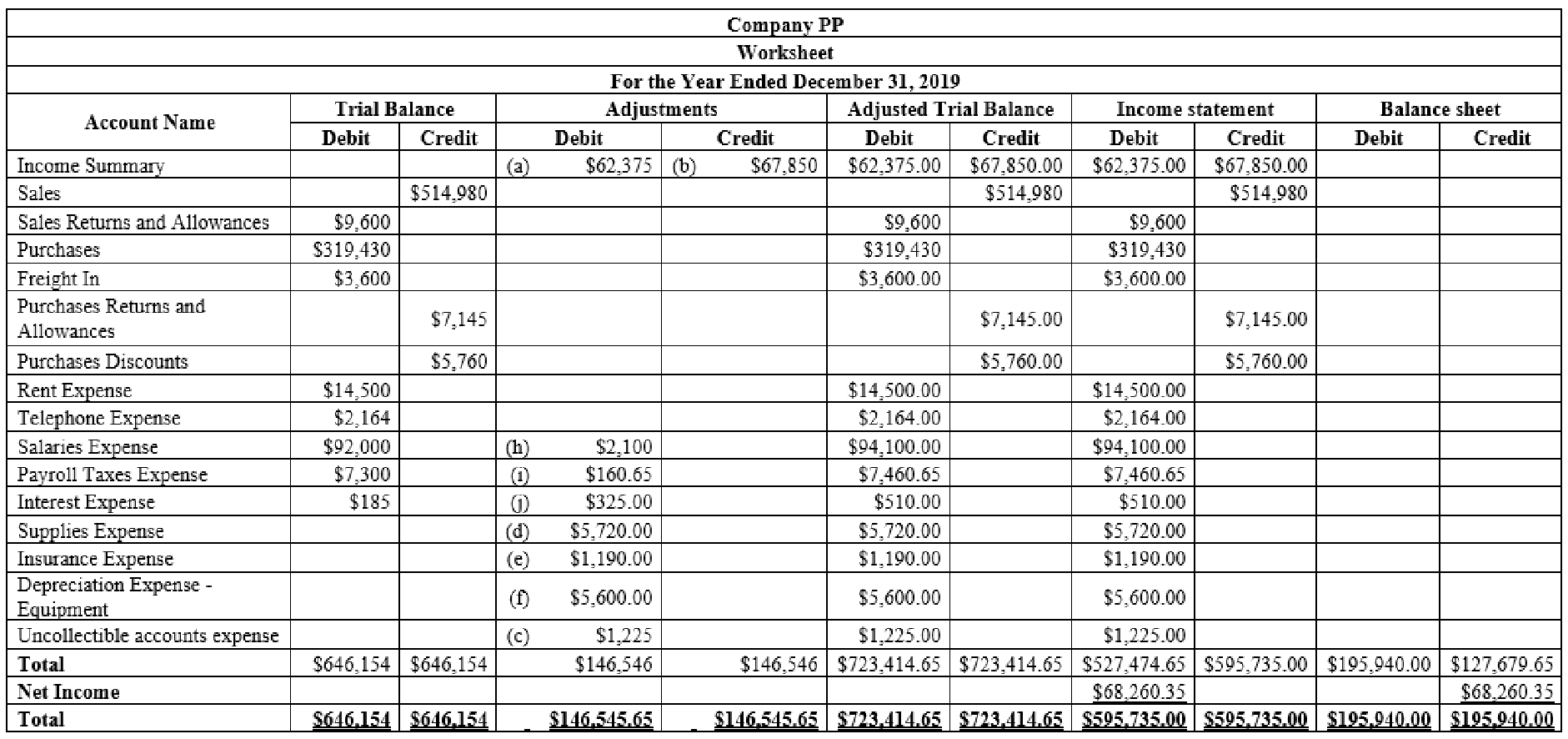

Prepare the worksheet and complete the sections of Trial balance, adjustments and compute the changes to the BW Capital that will be shown in the statement of owner's equity.

Explanation of Solution

Worksheet: A worksheet is the used in the preparation of the financial statement. It is a pre-defined form, having multiple columns, used in the adjustment process.

Prepare the worksheet for the year ended December 31, 2019.

Figure (1)

Figure (2)

2.

Show the Classified Income Statement.

Explanation of Solution

Classified Income statement: The classified income statement is a financial statement that shows the revenues, expenses with various classifications and sub-totals. The classified income statement is used for complex income statement as its more easily understandable.

Prepare the classified income statement:

| Company PP | ||||

| Income Statement | ||||

| Year Ended December 31, 2019 | ||||

| Particulars | Amount ($) | Amount ($) | Amount ($) | Amount ($) |

| Operating Revenue | ||||

| Sales | $514,980 | |||

| Less: Sales Returns and Allowances | $9,600 | |||

| Net Sales | $505,380 | |||

| Cost of Goods Sold | ||||

| Merchandise Inventory, January 1, 2019 | $62,375 | |||

| Purchases | $319,430 | |||

| Freight In | $3,600 | |||

| Delivered Cost of Purchases | $323,030 | |||

| Less: Sales Returns and Allowances | $7,145 | |||

| Purchases Discount | $5,760 | $12,905 | ||

| Net Delivered Cost of Purchases | $310,125 | |||

| Total Merchandise Available for sale | $372,500 | |||

| Less: Merchandise Inventory, closing | $67,850 | |||

| Cost of Goods Sold | $304,650 | |||

| Gross Profit on Sales | $200,730 | |||

| Operating Expenses | ||||

| Rent expense | $14,500 | |||

| Telephone Expense | $2,164 | |||

| Salaries Expense | $94,100 | |||

| Payroll Taxes Expense | $7,460.65 | |||

| Supplies Expense | $5,720 | |||

| Insurance Expense | $1,190 | |||

| Depreciation Expense - Equipment | $5,600 | |||

| Uncollectible Accounts Expense | $1,225 | |||

| Total Operating Expenses | $131,959.65 | |||

| Income from Operations | $68,770.35 | |||

| Other Expense | ||||

| Interest Expense | $510.00 | |||

| Net income for the year | $68,260.35 | |||

Table (1)

3.

Show the Statement of Owner's equity.

Explanation of Solution

Statement of owner's’ equity: This statement reports the beginning owner’s equity and all the changes which led to ending owner's’ equity.

Prepare the Statement of owner's’ equity:

| Company PP | ||

| Statement of Owner's Equity | ||

| Year Ended December 31, 2019 | ||

| Particulars | Amount ($) | Amount ($) |

| YT Capital, January 1, 2019 | $93,620 | |

| Net income for the year | $68,260.35 | |

| Deduct - Withdrawals | $50,000.00 | |

| Increase in Capital | $18,260.35 | |

| YT Capital, December 31, 2019 | $111,880.35 | |

Table (2)

4.

Show the Classified Balance Sheet and compute the percentage change in the owner’s capital in the accounting year 2019.

Explanation of Solution

Classified balance sheet: The main elements of balance sheet assets, liabilities, and stockholders’ equity are categorized or classified further into sections, and sub-sections in a classified balance sheet. Assets are further classified as current assets, long-term investments, property, plant, and equipment (PPE), and intangible assets. Liabilities are classified into two sections current and long-term. Stockholders’ equity comprises of common stock and retained earnings. Thus, the classified balance sheet includes all the elements under different sections.

Prepare the classified balance sheet:

| Company PP | |||

| Balance Sheet | |||

| December 31, 2019 | |||

| Particulars | Amount ($) | Amount ($) | Amount ($) |

| Assets | |||

| Current Assets | |||

| Cash | $15,280 | ||

| Accounts receivable | $26,600 | ||

| Less: Allowance for Doubtful Debts | $1,320 | $25,280 | |

| Merchandise Inventory | $67,850 | ||

| Prepaid expenses | |||

| Supplies | $1,020 | ||

| Prepaid insurance | $1,190 | $2,210 | |

| Total Current Assets | $110,620 | ||

| Plant and Equipment | |||

| Equipment | $34,000 | ||

| Less: Accumulated Depreciation | $15,700 | $18,300 | |

| Total Plant and Equipment | $18,300 | ||

| Total Assets | $128,920 | ||

| Liabilities and Owner's Equity | |||

| Current Liabilities | |||

| Notes Payable | $7,264 | ||

| Accounts payable | $6,500 | ||

| Interest Payable | $325 | ||

| Social Security Tax Payable | $690.20 | ||

| Medicare Tax Payable | $160.45 | ||

| Salaries Payable | $2,100 | ||

| Total Current Liabilities | $17,039.65 | ||

| Owner's Equity | |||

| YT Capital | $111,880.35 | ||

| Total Liabilities and Owner's Equity | $128,920 | ||

Table (3)

Compute the percentage increase in owner’s capital:

The percentage increase in the owner’s capital is 19.5%.

5.

Journalize the adjusting entries as on December 31, 2019.

Explanation of Solution

Adjusting entries: Adjusting entries are those entries which are recorded at the end of the year, to update the income statement accounts (revenue and expenses) and balance sheet accounts (assets, liabilities, and stockholders’ equity) to maintain the records according to accrual basis principle.

Pass the adjusting entry for the given transaction:

| General Journal | Page - 25 | |||

| Date | Description | Post Ref. | Debit | Credit |

| 2019 | ||||

| December 31 | Income Summary | $62,375 | ||

| Merchandise Inventory | $62,375 | |||

| (To record the beginning inventory) | ||||

| December 31 | Merchandise Inventory | $67,850 | ||

| Income Summary | $67,850 | |||

| (To record the closing inventory) | ||||

| December 31 | Uncollectible Accounts Expense | $1,225 | ||

| Allowance for Doubtful Accounts | $1,225 | |||

| (To record the estimated loss on the net credit sale) |

Table (4)

| General Journal | Page - 26 | |||

| Date | Description | Post Ref. | Debit | Credit |

| 2019 | ||||

| December 31 | Supplies Expense | $5,720 | ||

| Supplies | $5,720 | |||

| (To record the Supplies used) | ||||

| December 31 | Insurance expense | $1,190 | ||

| Prepaid Insurance | $1,190 | |||

| (To record the prepaid insurance) | ||||

| December 31 | Depreciation Expense - Equipment | $5,600 | ||

| Accumulated Depreciation - Equipment | $5,600 | |||

| (To record the depreciation on equipment) | ||||

| December 31 | Interest expense | $325 | ||

| Interest Payable | $325 | |||

| (To record the interest payable) | ||||

| December 31 | Salaries Expense | $2,100 | ||

| Salaries Payable | $2,100 | |||

| (To record the salaries payable) | ||||

| December 31 | Payroll Taxes Expense | $160.65 | ||

| Social Security Tax Payable | $130.20 | |||

| Medicare Tax Payable | $30.45 | |||

| (To record the taxes on accrued wages) |

Table (5)

6.

Journalize the closing entries as on December 31, 2019.

Explanation of Solution

Closing entries: The journal entries prepared to close the temporary accounts to Retained Earnings account are referred to as closing entries. The revenue, expense, and dividends accounts are referred to as temporary accounts because the information and figures in these accounts is held temporarily and consequently transferred to permanent account at the end of accounting year.

Pass the closing entries:

| General Journal | Page - 27 | |||

| Date | Description | Post Ref | Debit | Credit |

| 2019 | ||||

| December 31 | Sales | $514,980 | ||

| Purchases Returns and allowances | $7,145 | |||

| Purchases Discounts | $5,760 | |||

| Income Summary | $527,885 | |||

| (To record the closing entry for the income) | ||||

| December 31 | Income Summary | $465,099.65 | ||

| Sales Returns and Allowances | $9,600 | |||

| Purchases | $319,430 | |||

| Freight In | $3,600 | |||

| Rent Expense | $14,500 | |||

| Telephone Expense | $2,164 | |||

| Salaries Expense | $94,100.00 | |||

| Payroll Taxes Expense | $7,460.65 | |||

| Supplies Expense | $5,720 | |||

| Insurance expense | $1,190 | |||

| Depreciation Expense - Warehouse Equipment | $5,600 | |||

| Uncollectible Accounts Expense | $1,225 | |||

| Interest Expense | $510 | |||

| (To record the closing entry for the expenses) |

Table (6)

| General Journal | Page - 28 | |||

| Date | Description | Post Ref | Debit | Credit |

| 2019 | ||||

| December 31 | Income Summary | $68,260.35 | ||

| YT Capital | $68,260.35 | |||

| (To record the closing entry for the capital) | ||||

| December 31 | YT Capital | $50,000 | ||

| YT Drawings | $50,000 | |||

| (To record the closing entry for the capital) |

Table (7)

7.

Journalize the reversing entries as on January 1, 2020.

Explanation of Solution

Reversing entries: Reversing entries are those entries which are recorded at the beginning of the year, to reverse or set right the adjusting entries made in the end of the previous accounting year, in order to maintain the records according to accrual basis principle.

Pass the reversing entries:

| General Journal | Page - 29 | |||

| Date | Description | Post Ref | Debit | Credit |

| 2020 | ||||

| January 1 | Interest Payable | $325 | ||

| Interest Expense | $325 | |||

| (To record the reversing entry for interest payable) | ||||

| January 1 | Salaries Payable | $2,100 | ||

| Salaries Expense - Office | $2,100 | |||

| (To record the reversing entry for salaries payable) | ||||

| January 1 | Social Security Tax Payable | $130.20 | ||

| Medicare Tax Payable | $30.45 | |||

| Payroll Taxes Expense | $160.65 | |||

| (To record the reversing entry for payroll taxes payable) |

Table (8)

Want to see more full solutions like this?

Chapter 13 Solutions

COLLEGE ACCOUNTING (LL)W/ACCESS>CUSTOM<

- Post the following November transactions to T-accounts for Accounts Payable and Inventory, indicating the ending balance (assume no beginning balances in these accounts). A. purchased merchandise inventory on account, $22,000 B. paid vendors for part of inventory purchased earlier in month, $14,000 C. purchased merchandise inventory for cash, $6,500arrow_forwardPost the following November transactions to T-accounts for Accounts Payable, Inventory, and Cash, indicating the ending balance. Assume no beginning balances in Accounts Payable and Inventory, and a beginning Cash balance of $36,500. A. purchased merchandise inventory on account, $16,000 B. paid vendors for part of inventory purchased earlier in month, $12,000 C. purchased merchandise inventory for cash, $10,500arrow_forwardPalisade Creek Co. is a merchandising business that uses the perpetual inventory system. The account balances for Palisade Creek Co. as of May 1, 2019 (unless otherwise indicated), are as follows: During May, the last month of the fiscal year, the following transactions were completed: Instructions 1. Enter the balances of each of the accounts in the appropriate balance column of a four-column account. Write Balance in the item section and place a check mark () in the Posting Reference column. Journalize the transactions for May, starting on Page 20 of the journal. 2. Post the journal to the general ledger, extending the month-end balances to the appropriate balance columns after all posting is completed. In this problem, you are not required to update or post to the accounts receivable and accounts payable subsidiary ledgers. 3. Prepare an unadjusted trial balance. 4. At the end of May, the following adjustment data were assembled. Analyze and use these data to complete (5) and (6). 5. (Optional) Enter the unadjusted trial balance on a 10-column end-of-period spreadsheet (work sheet), and complete the spreadsheet. 6. Journalize and post the adjusting entries. Record the adjusting entries on Page 22 of the journal. 7. Prepare an adjusted trial balance. 8. Prepare an income statement, a statement of owners equity, and a balance sheet. 9. Prepare and post the closing entries. Record the closing entries on Page 23 of the journal. Indicate closed accounts by inserting a line in both Balance columns opposite the closing entry. Insert the new balance in the owners capital account. 10. Prepare a post-closing trial balance.arrow_forward

- The accounts and their balances in the ledger of Markeys Mountain Shop as of December 31, the end of its fiscal year, are as follows: Data for the adjustments are as follows. Assume that Markeys Mountain Shop uses the perpetual inventory system. a. Merchandise Inventory at December 31, 140,357. b. Store supplies inventory (on hand) at December 31, 540. c. Depreciation of building, 3,400. d. Depreciation of store equipment, 3,800. e. Salaries accrued at December 31, 1,250. f. Insurance expired during the year, 1,480. Required 1. Complete the work sheet after entering the account names and balances onto the work sheet. Ignore this step if using CLGL. 2. Journalize the adjusting entries. If using manual working papers, record adjusting entries on journal page 63.arrow_forwardOn December 31, the end of the year, the accountant for Fireside Magazine was called away suddenly because of an emergency. However, before leaving, the accountant jotted down a few notes pertaining to the adjustments. Journalize the necessary adjusting entries. Assume that Fireside Magazine uses the periodic inventory system. ab. A physical count of inventory revealed a balance of 199,830. The Merchandise Inventory account shows a balance of 202,839. c. Subscriptions received in advance amounting to 156,200 were recorded as Unearned Subscriptions. At year-end, 103,120 has been earned. d. Depreciation of equipment for the year is 12,300. e. The amount of expired insurance for the year is 1,612. f. The balance of Prepaid Rent is 2,400, representing four months rent. Three months rent has expired. g. Three days salaries will be unpaid at the end of the year; total weekly (five days) salaries are 4,000. h. As of December 31, the balance of the supplies account is 1,800. A physical inventory of the supplies was taken, with an amount of 920 determined to be on hand.arrow_forwardA firm is preparing to make adjusting entries at the end of the accounting period. The balance of the merchandise inventory account is 200,000. If the firm is using the periodic inventory system, what does this balance represent?arrow_forward

- A merchandising company shows 8,842 in the Supplies account on the preadjusted trial balance. After taking inventory of the actual supplies, the company still owns 3,638. a. How much was used or expired? b. Write the adjusting entry.arrow_forwardOn January 1, Incredible Infants sold goods to Babies Inc. for $1,540, terms 30 days, and received payment on January 18. Which journal would the company use to record this transaction on the 18th? A. sales journal B. purchases journal C. cash receipts journal D. cash disbursements journal E. general journalarrow_forwardThe trial balance of Jillson Company as of December 31, the end of its current fiscal year, is as follows: Here are the data for the adjustments. ab. Merchandise Inventory at December 31, 54,845.00. c. Store supplies inventory (on hand), 488.50. d. Insurance expired, 680. e. Salaries accrued, 692. f. Depreciation of store equipment, 3,760. Required Complete the work sheet after entering the account names and balances onto the work sheet.arrow_forward

- A firm is preparing to make adjusting entries at the end of the accounting period. The balance of the merchandise inventory account is 100,000. If the firm is using the perpetual inventory system, what does this balance represent?arrow_forwardOn December 31, 2019, the balances of the accounts appearing in the ledger of Wyman Company are as follows: Instructions 1. Does Wyman Company use a periodic or perpetual inventory system? Explain. 2. Prepare a multiple-step income statement for Wyman Company for the year ended December 31, 2019. The merchandise inventory as of December 31, 2019, was 305,000. The adjustment for estimated returns inventory for sales for the year ending December 31, 2019, was 30,000. 3. Prepare the closing entries for Wyman Company as of December 31, 2019. 4. What would the net income have been if the perpetual inventory system had been used?arrow_forwardReview the following transactions and prepare any necessary journal entries for Tolbert Enterprises. A. On April 7, Tolbert Enterprises contracts with a supplier to purchase 300 water bottles for their merchandise inventory, on credit, for $10 each. Credit terms are 2/10, n/60 from the invoice date of April 7. B. On April 15, Tolbert pays the amount due in cash to the supplier.arrow_forward

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College