Concept explainers

Videos

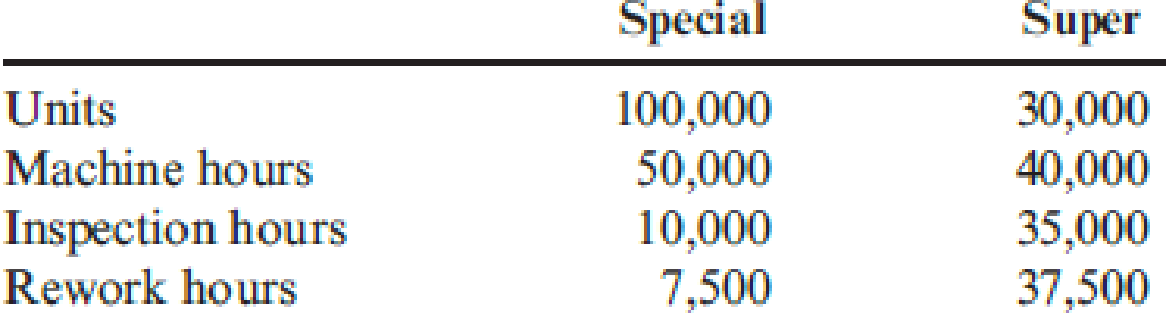

Harvey Company produces two models of blenders: the “Super Model” (priced at $400) and the “Special Model” (priced at $200). Recently, Harvey has been losing market share with its Special Model because of competitors offering blenders with the same quality and features but at a lower price. A careful market study revealed that if Harvey could reduce the price of its Special Model to $180, it would regain its former share of the market. Management, however, is convinced that any price reduction must be accompanied by a cost reduction of the same amount so that per-unit profitability is not affected. Earl Wise, company controller, has indicated that poor

The consumption patterns of the two products are as follows:

Harvey assigns overhead costs to the two products using a plantwide rate based on machine hours.

Required:

- 1. Calculate the unit overhead cost of the Special Model using machine hours to assign overhead costs. Now, repeat the calculation using ABC to assign overhead costs. Did improving the accuracy of cost assignments solve Harvey’s competitive problem? What did it reveal?

- 2. Now, assume that in addition to improving the accuracy of cost assignments, Earl observes that defective supplier components are the root cause of both the inspection and rework activities. Suppose further that Harvey has found a new supplier that provides higher-quality components such that inspection and rework costs are reduced by 50 percent. Now, calculate the cost of the Special Model (assuming that inspection and rework times are also reduced by 50 percent) using ABC. The relative consumption patterns also remain the same. Comment on the difference between ABC and ABM.

Trending nowThis is a popular solution!

Chapter 12 Solutions

Cornerstones of Cost Management (Cornerstones Series)

- Harvey Company produces two models of blenders: the “Super Model” (priced at $400) and the “Special Model” (priced at $200). Recently, Harvey has been losing market share with its Spe-cial Model because of competitors offering blenders with the same quality and features but at a lower price. A careful market study revealed that if Harvey could reduce the price of its Special Model to $180, it would regain its former share of the market. Management, however, is con-vinced that any price reduction must be accompanied by a cost reduction of the same amount so that per-unit profitability is not affected. Earl Wise, company controller, has indicated that pooroverhead costing assignments may be distorting management’s view of each product’s cost and,therefore, the ability to know how to set selling prices. Earl has identified the following overheadactivities: machining, inspection, and rework. The three activities, their costs, and practicalcapacities are as follows: Activity Cost…arrow_forwardQuality Chairs Inc. (QC) manufactures chairs for industrial use. Laura Winters, the Vice President for Marketing at QC, concluded from market analysis that sales were dwindling for QC's standard three-foot chair due to aggressive pricing by competitors. QC's chairs sold for $890 whereas the competition's comparable chair was selling for $750. Winters determined that a price drop to $750 would be necessary to regain market share and reach a targeted annual sales level of 10,000 chairs. Cost data based on sales of 10,000 chairs: Budgeted Quantity Actual Quantity Actual Cost Direct materials (board feet) 89,700 81,200 $ 1,258,500 Direct labor (hours) 72,200 74,625 876,700 Machine hours (hours) 12,250 12,100 251,700 Finishing and packing (hours) 7,350 7,250 126,700 The current profit per unit is: Multiple Choice $588. $638. $813. $788. $738.arrow_forwardQuality Chairs Inc. (QC) manufactures chairs for industrial use. Laura Winters, the Vice President for Marketing at QC, concluded from market analysis that sales were dwindling for QC's standard three-foot chair due to aggressive pricing by competitors. QC's chairs sold for $550 whereas the competition's comparable chair was selling for $495. Winters determined that a price drop to $495 would be necessary to regain market share and reach a targeted annual sales level of 10,000 chairs.Cost data based on sales of 10,000 chairs: Budgeted Quantity Actual Quantity Actual Cost Direct materials (board feet) 88,000 79,500 $ 1,250,000 Direct labor (hours) 71,350 73,775 875,000 Machine hours (hours) 11,400 11,250 250,000 Finishing and packing (hours) 6,500 6,400 125,000 In order to reduce costs so as to reach the desired target cost, Quality Chairs should also focus on reducing the cost of: Multiple Choice Mechanical…arrow_forward

- Tool Industries manufactures large workbenches for industrial use. Sam Hartnet, the Vice President for marketing at Tool Industries, concluded from market analysis that sales were dwindling for Tool's workbenches due to aggressive pricing by competitors. Tool's workbench sells for $1,440 whereas the competition's comparable workbench sells for $1,300. Sam determined that a price drop to $1,300 would be necessary to protect its market share and maintain an annual sales level of 13,600 workbenches. Cost data based on sales of 13,600 workbenches: Budgeted Quantity Actual Quantity Actual Cost Direct materials (pounds) 178,000 171,000 $ 3,453,000 Direct labor (hours) 74,000 73,000 826,500 Machine setups (number of setups) 1,200 1,000 253,000 Mechanical assembly (machine hours) 29,400 282,750 3,756,000 The current cost per unit is (rounded to the nearest whole dollar): Multiple Choice $560. $495. $437. $609. $417.arrow_forwardTool Industries manufactures large workbenches for industrial use. Sam Hartnet, the Vice President for marketing at Tool Industries, concluded from market analysis that sales were dwindling for Tool's workbenches due to aggressive pricing by competitors. Tool's workbench sells for $1,140 whereas the competition's comparable workbench sells for $1,060. Sam determined that a price drop to $1,060 would be necessary to protect its market share and maintain an annual sales level of 13,000 workbenches.Cost data based on sales of 13,000 workbenches: Budgeted Quantity Actual Quantity Actual Cost Direct materials (pounds) 175,000 168,000 $ 3,450,000 Direct labor (hours) 72,800 71,500 825,000 Machine setups (number of setups) 900 880 250,000 Mechanical assembly (machine hours) 273,000 281,250 3,750,000 If the profit per unit is maintained, the target cost per unit is (rounded to the nearest whole dollar): Multiple Choice $489. $557. $516. $424.…arrow_forwardQuality Industries manufactures large workbenches for industrial use. Yewell Hartnet, the Vice President for marketing at Quality Industries, concluded from market analysis that sales were dwindling for Quality's workbenches due to aggressive pricing by competitors. Quality's workbench sells for $1,690 whereas the competition's comparable workbench sells for $1,500. Yewell determined that a price drop to $1,500 would be necessary to protect its market share and maintain an annual sales level of 14,100 workbenches. Cost data based on sales of 14,100 workbenches: Budgeted Quantity Actual Quantity Actual Cost Direct materials (pounds) 180,500 173,500 $ 3,455,500 Direct labor (hours) 75,000 74,250 827,750 Machine setups (no. of setups) 1,450 1,100 255,500 Mechanical assembly (machine hours) 31,150 284,000 3,761,000 If the profit per unit is maintained, the target cost per unit is (rounded to the nearest whole dollar):arrow_forward

- Quality Chairs Incorporated (QC) manufactures chairs for industrial use. Laura Winters, the Vice President for Marketing at QC, concluded from market analysis that sales were dwindling for QC's standard three-foot chair due to aggressive pricing by competitors. QC's chairs sold for $580 whereas the competition's comparable chair was selling for $525. Winters determined that a price drop to $525 would be necessary to regain market share and reach a targeted annual sales level of 10,000 chairs. Cost data based on sales of 10,000 chairs: Budgeted Quantity Actual Quantity Actual Cost Direct materials (board feet) 90,100 81,300 $ 1,280,000 Direct labor (hours) 73,800 76,300 905,000 Machine hours (hours) 12,800 12,600 280,000 Finishing and packing (hours) 8,100 7,900 155,000 The current cost per unit is: Multiple Choice $262.00. $312.00. $412.00. $462.00. $487.00.arrow_forwardGreenview Dairies produces a line of organic yogurts for sale at supermarkets and specialty markets in the Southeast. Economic conditions and changing tastes have resulted in slowing demand growth. After recently expanding capacity, the company is now operating at 65 percent of the new capacity. The company is considering dropping one of the yogurt flavors, mixed berry, in hopes of improving profitability. If the mixed berry variety is dropped, the revenue associated with it will be lost and the related variable costs saved. The production manager estimates that the fixed costs will also be reduced by 30 percent. The following quarterly product line income statements (in thousands of dollars) are available: Product Sales Variable costs Contribution margin Fixed costs allocated to each product line Operating profit (loss) Vanilla $21,790 14,700 $7,090 3,095 $3,995 Peach $33,840 26,465 $7,375 4,655 $2,720 Mixed Berry $28,380 25,490 Complete this question by entering your answers in the…arrow_forwardThe Chromosome Manufacturing Company produces two products, X and Y. The company president, Gene Mutation, is concerned about the fierce competition in the market for product X. He notes that competitors are selling X for a price well below Chromosome's price of P12.70. At the same time, he notes that competitors are pricing product Y almost twice as high as Chromosome's price of P12.50. Mr. Mutation has obtained the following data for a recent time period: PRODUCT X PRODUCT Y Number of Units 11,000 3,000 Direct Materials Cost Per Unit 3.23 3.09 Direct Labor Cost Per Unit 2.22 2.10 Direct Labor Hours 10,000 2,500 Machine Hours 2,100 2,800 Inspection Hours 80 100 Purchase Orders 10 10 Mr. Mutation has learned that overhead costs are assigned to products on the basis of direct labor hours. The overhead costs for his time period consisted of the following items: Overhead Cost Item Amount Inspecting Costs…arrow_forward

- The Chromosome Manufacturing Company produces two products, X and Y. The company president, Gene Mutation, is concerned about the fierce competition in the market for product X. He notes that competitors are selling X for a price well below Chromosome's price of P12.70. At the same time, he notes that competitors are pricing product Y almost twice as high as Chromosome's price of P12.50. Mr.Mutation has obtained the following data for a recent time period: Product X Product Y Number of units 11,000 3,000 Direct Materials cost per unit P3.23 P3.09 Direct Labor cost per unit P2.22 P2.10 Direct Labor hours 10,000 2,500 Machine hours 2,100 2,800 Inspection hours 80 100 Purchase orders 10 10 Mr. Mutation has learned that overhead costs are assigned to products on the basis of direct labor hours. The overhead costs for his time period consisted of the following items: Overhead Cost item Amount Inspection Costs P16,200 Purchasing Costs 8,000 Machine Cost…arrow_forwardMaxwell Company produces a variety of kitchen appliances, including cooking ranges and dishwashers. Over the past several years, competition has intensified. In order to maintain—and perhaps increase—its market share, Maxwell’s management decided that the overall quality of its products had to be increased. Furthermore, costs needed to be reduced so that the selling prices of its products could be reduced. After some investigation, Maxwell concluded that many of its problems could be traced to the unreliability of the parts that were purchased from outside suppliers. Many of these components failed to work as intended, causing performance problems. Over the years, the company had increased its inspection activity of the final products. If a problem could be detected internally, then it was usually possible to rework the appliance so that the desired performance was achieved. Management also had increased its warranty coverage; warranty work had been increasing over the years. DAVID…arrow_forwardPeterson Corporation is considering implementing a JIT production system. The new system would reduce current average inventory levels of $2,000,000 by 75%, but it would require a much greater dependency on the company’s core suppliers for on-time deliveries and high-quality inputs. The company’s operations manager, John Leung, is opposed to the idea of a new JIT system. He is concerned that the new system (a) will be too costly to manage; (b) will result in too many stock outs; and (c) will lead to the layoff of his employees, several of whom are currently managing inventory. He believes that these layoffs will affect the morale of his entire production department. The management accountant, Susan Chow, is in favour of the new system, due to the likely result in cost savings. John wants Susan to revise her cost saving estimation because he is concerned that top management will give more weight to financial factors and not give due consideration to nonfinancial factors such as employee…arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning