The correct option for given situation where price taking firm’s optimal output level is required to be selected.

Answer to Problem 1MCQ

Option e is correct answer.

Explanation of Solution

Explanation for correct option:

d.

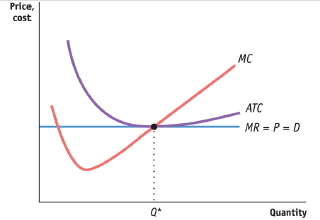

Firm should produce such level of output at which marginal cost is equal to the price and the marginal revenue which is shown below:

At this level of output, the price taking firm will maximize its profit. Therefore, option e is correct.

Explanation for incorrect options:

a.

The firm that is price taker should produce optimal quantity so that profit of the firm can be maximized. The marginal cost should not be equal to the total cost if it is so then firm will incur losses. If firm produces up to the point where MC is greater than price then it will incur loss. Therefore, option a is incorrect.

b.

The firm’s marginal cost should be equal to the price to attain optimal level of output. If the marginal cost is equal to

c.

The firm that possess marginal cost equivalent to average fixed cost then it will not necessarily earn maximum profit. The firm should select the output level at which it maximizes the profit. The firm produces at the level where P = MC to seek maximum profit. Therefore, option c is incorrect.

d.

Firm whose marginal revenues are equal to the marginal cost then it earns maximum profit. Pice of the product should also be equal to the marginal cost if firm seeks maximum profit at the output level. Therefore, option d is incorrect.

Introduction: The price taking firms can reduce the cost of production if they produce the correct amount of products. In other words, profit can be maximized if quantity produced is at minimum cost.

Want to see more full solutions like this?

Chapter 11R Solutions

Krugman's Economics For The Ap® Course

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education