ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

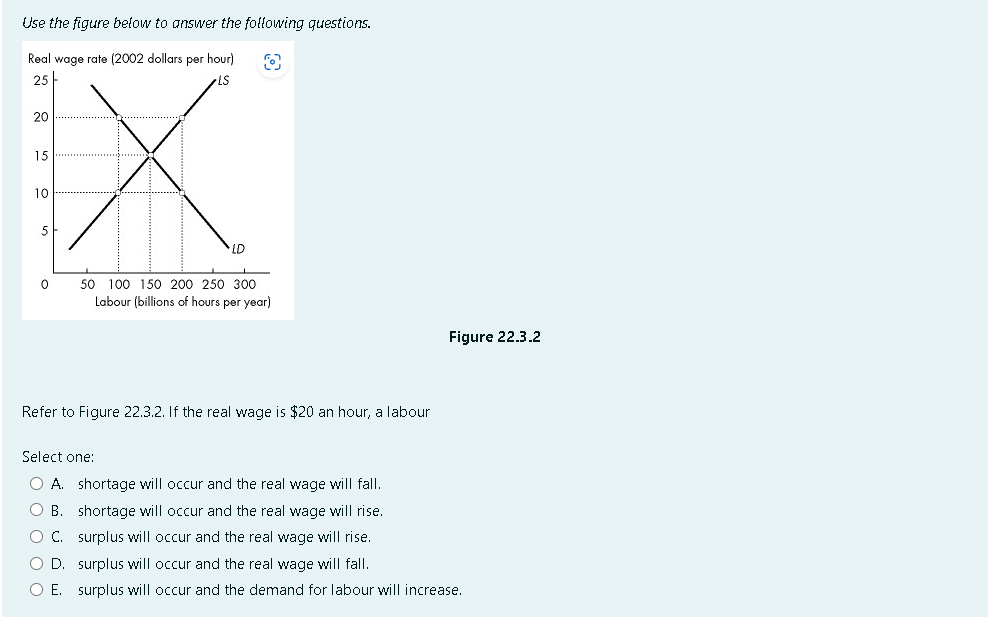

Transcribed Image Text:Use the figure below to answer the following questions.

Real wage rate (2002 dollars per hour) O

25

·IS

15

X

20

5

0

50 100 150 200 250 300

Labour (billions of hours per year)

Refer to Figure 22.3.2. If the real wage is $20 an hour, a labour

Figure 22.3.2

Select one:

O A. shortage will occur and the real wage will fall.

O B. shortage will occur and the real wage will rise.

O C.

surplus will occur and the real wage will rise.

O D. surplus will occur and the real wage will fall.

O E. surplus will occur and the demand for labour will increase.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Shoes What is the equation of the price line? O 150-*Shoes O 30-*Shoes O 30-*Butter O 150+ 5 Butter 30 120'000 100'000 Consider the same scenario as Question 31. Suppose that the government allows 15'000 foreign workers to enter the country. What happens to the equilibrium wage (in the short run)? W 30'000 O It will be greater than 120'000 It will be less than 100'000 O It will be equal to 100'000 O It will be greater than 100'000 150 70'000 Butter Sarrow_forwardQUESTION 4 You are given the following data of a labor market for an imaginary economy? Quantity Supplied 6,000 Hourly Wages Quantity Demanded $8 10,000 $10 9,000 7,000 $12 8,000 8,000 $13 7,000 9,000 $15 6,000 10,000 Assume that the government of this economy imposed a minimum wage of $10. As a result O 9,000 people will be employed. O 8,000 people will be employed. O 2,000 people will be unemployed. O zero people will be unemployed.arrow_forwardF18arrow_forward

- 2. Plotting the supply of labor In Detroit, 120 people are willing to work an hour as cashiers if the wage is $20 per hour. For each additional $5 that the wage rises above $20, an additional 30 people are willing to work an hour. For wages of $20, $25, $30, $35, and $40 per hour, plot the daily labor supply curve for cashiers on the following graph. WAGE RATE (Dollars per hour) 50 45 40 35 30 25 20 15 10 5 0 D 30 60 90 120 150 180 210 240 270 QUANTITY OF LABOR (Number of workers) 300 What is one explanation for why this labor supply curve is upward sloping? O Wages have to increase to accommodate union pressure. Firms are willing to hire more cashiers at a lower wage. O The opportunity cost of leisure increases as wages increase. O Unemployment benefits are steadily declining. Supplyarrow_forwardIf you observed the equilibrium wage rate increasing while equilibrium employment increased, which of the following would be a possible explanation? There was: O a decrease in labor demand an increase in labor supply O a decrease in labor supply an increase in labor demand * Previous Next ASUSarrow_forward37arrow_forward

- 6. Plotting the supply of labor In Providence, 120 people are willing to spend an hour working as pizza makers for an hourly wage of $20. For each additional $5 that the wage increases above $20, an additional 30 people are willing to spend an hour working. For hourly wages of $20, $25, $30, $35, and $40, plot the daily labor supply curve for pizza makers on the following graph. WAGE (Dollars per hour) 50 45 40 35 30 25 20 15 10 5 0 0 + 30 60 90 120 150 180 210 LABOR (Number of workers) 240 270 300 Supply What is one explanation for why this labor supply curve is upward sloping? The opportunity cost of leisure increases as wages increase. O Unemployment benefits are steadily declining. Wages have to increase to accommodate union pressure. O Firms are willing to hire fewer pizza makers at a higher wage.arrow_forward57arrow_forwardLO LL 50 45 40 20 15 WAGE (Dollars per hour) 6. Plotting the supply of labor In Philadelphia, 180 people are willing to work an hour as hostesses if the wage is $20 per hour. For each additional $5 that the wage rises above $20, an additional 45 people are willing to work an hour. For wages of $20, $25, $30, $35, and $40 per hour, plot the daily labor supply curve for hostesses on the following graph. Supply 35 25 5. 06 135 180 225 270 315 405 450 LABOR (Number of workers) What is one explanation for why this labor supply curve is upward sloping? MacBook Pro #3 24 2. 4. R M B. Narrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education