ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

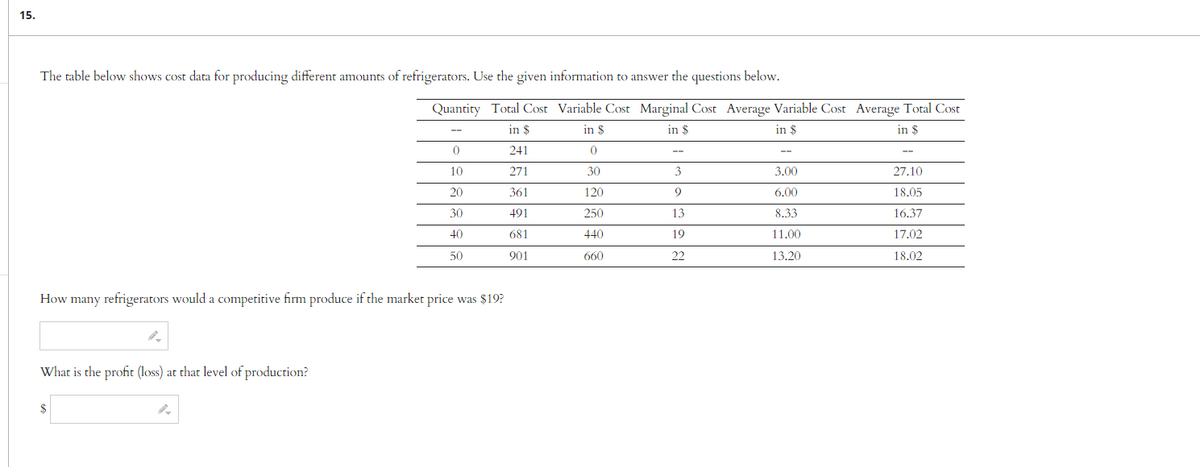

Transcribed Image Text:15.

The table below shows cost data for producing different amounts of refrigerators. Use the given information to answer the questions below.

Quantity Total Cost Variable Cost Marginal Cost Average Variable Cost Average Total Cost

in $

in $

in $

in $

in $

241

0

271

30

361

120

491

250

681

440

901

660

0

10

What is the profit (loss) at that level of production?

20

30

40

50

How many refrigerators would a competitive firm produce if the market price was $19?

3

9

13

19

22

3.00

6.00

8.33

11.00

13.20

27.10

18.05

16.37

17.02

18.02

Transcribed Image Text:16.

The table below shows cost data for producing different amounts of DVD player. Use the information in the table to find the missing costs for each quantity.

Marginal Cost in $

Quantity Total Cost in $

105

0

How many DVD player would a competitive firm produce if the market price was $130?

If the firm is currently producing 920, it should

Oincrease

Oreduce

Omaintain

quantity produced.

By doing so, it would

Oincrease

Oreduce

Omaintain

profit.

230

460

690

920

1150

7005

25405

55305

99005

151905

9.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- All informs includedarrow_forwardThe graph below shows the marginal cost (MC), average variable cost (AVC), and average total cost (ATC) curves for a firm in a competitive market. These curves imply a short-run supply curve that has two distinct parts. One part, not shown, lies along the vertical axis (quantity-0); this represents a condition of production shutdown. Where is the other part? Use the straight-line tool to drawit. To refer to the graphing tutorial for this question type, please click here Price and cost 18 15 14 13 12 10 19/21 SUBMIT ANSWER 13 OF 21 QUESTIONS C OMPLETED 28 MacBook Pro 금□ F7 F8 F9 F1o F2 F3 F5arrow_forwardFirm Profit, Loss, and Shut Down Based upon the graph, answer the following questions: 1) What is the production level that will maximize the profit for the firm? 2) What is the profit-maximizing price the firm will charge? 3) Will the firm incur an economic gain or economic loss? 4) What will the dollar amount of economic gain or economic loss be? 5) What will be the price and quantity where the firm will shut down?arrow_forward

- Use the table Costs for Alina's Apple Pies. If Alina's Apple Pies operates in a perfectly competitive market and the market price for a pie is $18, how many pies should Alina's Apple Pies produce and what is the economic profit or loss per unit?arrow_forwardAmos McCoy is currently raising corn on his 100-acre farm and earning an accounting profit of $100 per acre. However, if he raised soybeans, he could earned an accounting profit of $200 per acre. Is he currently earning an economic profit?arrow_forwardThe following graph plots daily cost curves for a firm operating in the competitive market for demin overalls. Hint: Once you have positioned the rectangle on the graph, select a point to observe its coordinates. PRICE (Dollars per overalls) 50 10 10 5 0 MC 2 ATC 8 18 QUANTITY (Thousands of overallises per day) AVC 10 20 Profit or Loss In the short run, given a market price equal to $15 per overalls, the firm should produce a daily quantity of On the preceding graph, use the blue rectangle (circle symbols) to fill in the area that represents profit or loss of the firm given the market price of $15 and the quantity of production from your previous answer. Note: In the following question, enter a positive number regardless of whether the firm earns a profit or incurs a loss. The rectangular area represents a short-run thousand per day for the firm. $ overallses.arrow_forward

- Use the table below to answer the following questions: Quantity Demand (Price) Marginal Revenue Marginal Cost Average Cost 1 $1200 1200 500 500 2 1100 1000 275 388 3 1000 800 225 333 4 900 600 250 313 5 800 400 400 330 6 700 200 500 358 7 600 0 700 407 What is this firm’s profit-maximizing price? What is its profit-maximizing output? What is the firm’s average profit? What is the firm’s total profit? If at least one consumer is willing to pay $1200 for this product, why won’t the monopolist charge $1200?arrow_forwardConsider the business whose Total Cost and Total Revenue for various quantities of a particular product are shown in the table below. Quantity Total Cost Total Revenue 0 100 0 1 250 500 2 350 950 3 500 1350 4 725 1700 5 1000 2000 6 1400 2250 Use the Profit-Maximizing Rule to explain the quantity that this business should produce to maximize its profits. Answer must both state the number to produce and an explanation of how you used the profit-maximizing rule to arrive at that number.arrow_forwardA young Thomas Edison makes 20 light bulbs a week in his dorm room. The parts for each light bulb cost $2.25. He sells each light bulb for $5.25. General Electric offers Thomas an executive job that pays $55.00 a week. Thomas’s weekly economic profit from making light bulbs is equal to: Instructions: Enter your answer as a whole number. If you are entering a negative number include a minus sign. $arrow_forward

- 50 MC ATC 40 30 MR 10 10 20 30 40 Quantity (per day) The figure above shows a perfectly competitive firm. The firm is operating; that is, the firm has not shut down. a) What is the output level should the firm produce to maximize the profit? b) What is the price does the firm charge at this output level? Price and costs (dollars) 20arrow_forwardThe graph shows the Cost curves for a profit maximizing firm in a competitive market. If the market price is $30 and the firm produces at the profit maximum quantity, what is the amount of the total fix costarrow_forwardUsing the Diagram above, answer the following questions: b). Suppose this firm produces 15 units of output. What is the variable cost of producing this level of output? What is the firm’s AVC of production when it produces 15 units of output. Explain your answer fully.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education