ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

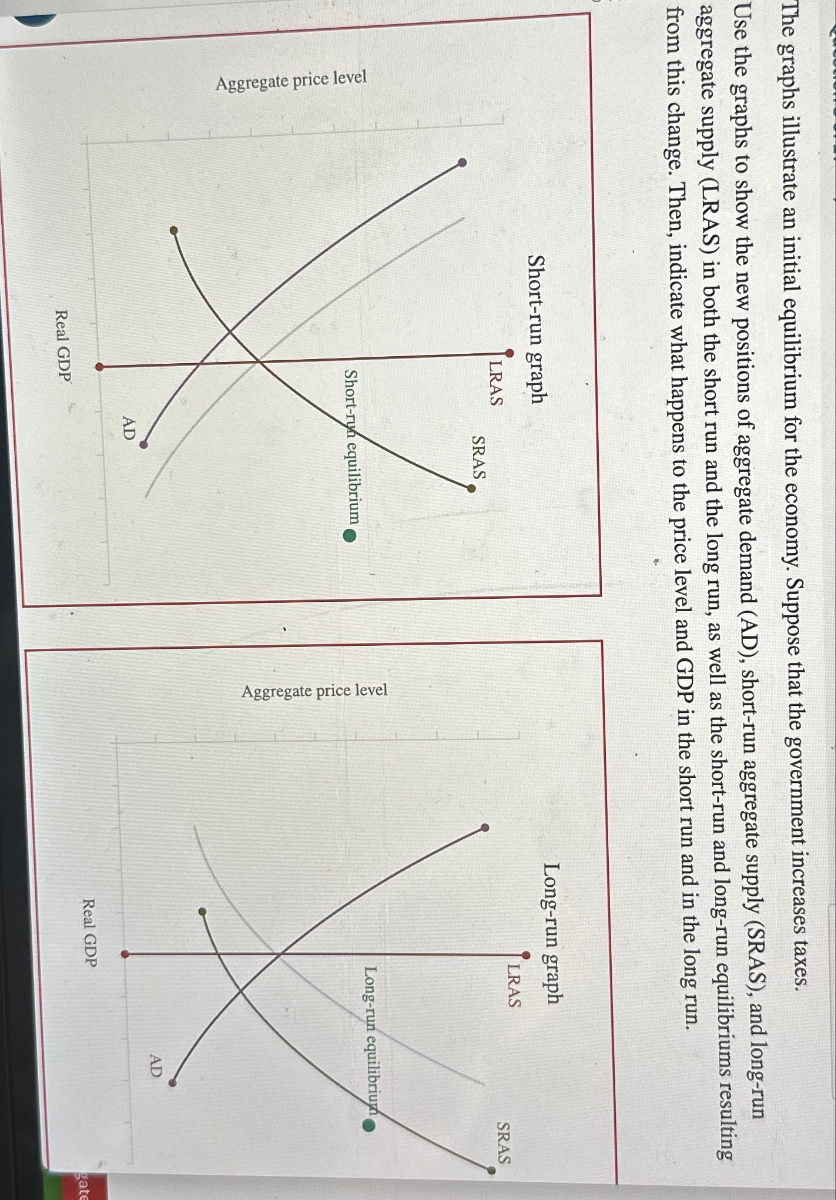

Transcribed Image Text:The graphs illustrate an initial equilibrium for the economy. Suppose that the government increases taxes.

Use the graphs to show the new positions of aggregate demand (AD), short-run aggregate supply (SRAS), and long-run

aggregate supply (LRAS) in both the short run and the long run, as well as the short-run and long-run equilibriums resulting

from this change. Then, indicate what happens to the price level and GDP in the short run and in the long run.

Aggregate price level

Short-run graph

LRAS

SRAS

Short-run equilibrium

Real GDP

AD

Aggregate price level

Long-run graph

LRAS

Long-run equilibrium

Real GDP

AD

SRAS

gate

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 4 steps with 4 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- A technological improvement raises productivity. On the following graph indicate the short run and long run effects of this change on the economy, assuming policymakers take no action. In the short run, the price level blanks and output blank. In the long run, the price level will be blank and output will be blank compared to the initial equilibrium prior to the changearrow_forwardH1.arrow_forwardThe following graph shows the aggregate demand curve in a hypothetical economy. Assume that the economy's money supply remains fixed. PRICE LEVEL (CPI) 180 T 150 140 130 120 110 100 90 80 0 Aggregate Demand 100 200 300 400 500 600 REAL GDP (Billions of dollars) 700 800 (?) Which of the following are reasons the aggregate demand curve is downward sloping? Check all that apply. A higher price level makes domestically produced goods more expensive than foreign goods. A lower price level leads to a lower interest rate. A higher price level decreases consumption through the substitution effect. As the aggregate price level rises, the purchasing power of households' saving balances will demanded to This phenomenon is known as the effect. causing the quantity of outputarrow_forward

- Explain, in detail, how the adjustment to macroeconomic equilibrium occurs when spending is less than production. Be sure to discuss how inventories play a crucial role in the adjustment process. State what happens to GDP and employment during the adjustment process.arrow_forward5arrow_forwardAssume initially an economy is at its long run equilibrium. Then, price of oil in theworld increases. What will happen to real GDP and aggregate price level in the short runequilibrium following the increase in price of oil? Use the Aggregate Demand – AggregateSupply model to answer the question.arrow_forward

- Suppose the people of Canada has reduced their spending on goods and services from the United States. What will be the effect on real GDP and the price level in the short run? In the long run? Show your results graphically.arrow_forwardQuestion: The attached picture shows the aggregate demand/aggregate supply situation in the U.S. What is the value of actual GDP? What is the value of the GDP deflator? Assume that people and businesses become pessimistic about the future of the economy; how will this affect the graph above in the short run? (i.e., which curve(s) will shift, and in which direction?) After the short-run event in part b, what will happen to actual GDP? What will happen to the price level? After the short-run event in part b, describe how the economy is doing in terms of the business cycle (i.e., recession, full employment, expansion). What long-run adjustments will be made in this economy as a result of the short-run changes in part c? How will the curve(s) shift in response to these long-run adjustments? After the long-run adjustments in part e, describe how the economy is doing in terms of the business cycle (i.e., recession, full employment, expansion).arrow_forwardThe graph shows an economy in macroeconomic equilibrium. Now, three things occur: The world economy goes into an expansion, domestic businesses expect future profits to rise, and the government increases its expenditure on goods and services as international tensions increase. On the graph, draw one new curve that shows the combined effect of the three events. Label it. Draw a point at the new macroeconomic equilibrium. >>> Draw only the objects specified in the question.arrow_forward

- # I am guessing, the price of imports will decrease is wrong.arrow_forwardAnswer both questions that need to be answered and the second question has a graph that’s needs to be answered as well.arrow_forwardSuppose our economy is in macroeconomic equilibrium (also called "general equilibrium") with an upward-sloping aggregate supply curve and a downward-sloping aggregate demand curve. An increase in aggregate demand will: Question 5 options: a) Increase aggregate supply. b) Decrease the price level. c) Causes the aggregate supply to shift to the right. d) Increase real GDP. e) Reduce the number of discouraged workers in the unemployment rate.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education