ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

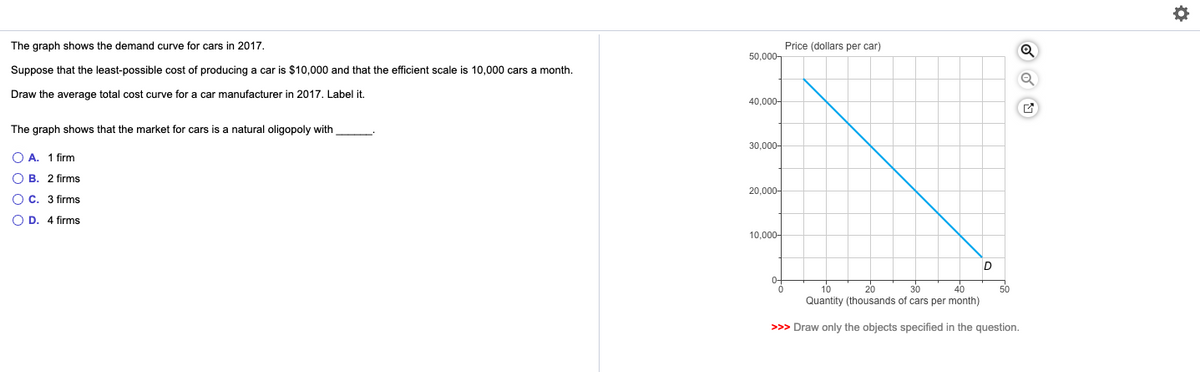

Transcribed Image Text:The graph shows the demand curve for cars in 2017.

Suppose that the least-possible cost of producing a car is $10,000 and that the efficient scale is 10,000 cars a month.

Draw the average total cost curve for a car manufacturer in 2017. Label it.

The graph shows that the market for cars is a natural oligopoly with

O A. 1 firm

OB. 2 firms

OC. 3 firms

OD. 4 firms

50,000-

40,000-

30,000-

20,000-

10,000-

0-

Price (dollars per car)

0

D

30

Quantity (thousands of cars per month)

>>> Draw only the objects specified in the question.

50

Q

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 4 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- 1. Two firms produce identical products at zero cost, and they compete by setting prices. If each firm charges a low price, the both firms earn profits of zero. If each firm charges a high price, then each firm earns profits of $30. if one firm charges a high price and the other firm charges a low price, the firm that charges the lowest price earns profits of $50 and the firm charging the highest price earns profits of zero. a. Write this game in normal form. b. Suppose the game is infinitely repeated. Can the players sustain the "collusive outcome" as a Nash equilibrium if the interest rate if 50 percent?arrow_forward5. Duopolist firms 1 and 2 compete on price with some market differentiation. Demand for firm ie{1, 2} is q, = 2 – 2p, + p, Neither firm has costs. a. Find the best response functions for each firm in the static game. b. Find the unique Nash equilibrium prices in the static game. c. Are prices strategic complements or strategic substitutes? Briefly explain. d. Does Firm 1 want Firm 2 to increase or decrease p,?arrow_forward12. Consider a duopoly market. Two firms are selling identical products and all costs are assumed to be zero for simplicity. Market demand schedule is given in the following table. Note that firms always choose an integer value for the quantity of production. Quantity Price Total Profit 3 $12 4 11 5 8 6 6. 7 4 8 2 1 10 a. Fill in the column of total profit.arrow_forward

- Briefly discuss the forces that have increased the level of competition faced by firms in the modern-day U.S. economy and elsewhere.arrow_forwardThe market for agricultural products such as wheat or corn would best be described by which market model? O monopolistic competition Opure competition Opure monopoly oligopolyarrow_forwardExplain why it is not possible for a monopoly firm to maximise its profits by charging a price in the price region where demand is inelastic, even though there are no direct substitutes for its product. Also explain how a monopoly will be able to charge a higher price than a firm producing the good under perfect, oligopolistic, or monopolistic competitionarrow_forward

- I need help with econ multiple hw questions asap! 93) As the number of firms change in an oligopoly market, what will it become? A. As the number of firms increases, the market approaches a monopoly market equilibrium B. As the number of firms increases, the market approaches a competitive market equilibrium C. As the number of firms decreases, the market approaches a socially optimal equilibrium. D. As the number of firms decreases, the market approaches a cartel equilibrium. 92) Refer to the attached Table 40. If both stores follow a dominant strategy, what will SuperDuper Saver's growth-related profits be? A. $25 B. $250 C. $85 D. $50arrow_forwardCoke and Pepsi dominate the cola market. Suppose that the marginal cost of making cola is $2. Assume also that the demand for cola is given by the following table: Price $8 7 6 5 4 3 2 1 Quantity 5 cans 6 7 8 9 10 11 12 Suppose Coke and Pepsi both supply cola. They form a cartel and agree to cooperate on how much soda to produce. In this cartel case, how many bottles of cola would be sold? Type your answer...arrow_forwardAir Canada and WestJet recently cut their prices for flights between Toronto and Edmonton to $199. In response, Porter Airlines cut its price from $239 to $199 for flights between Toronto and Edmonton in order to remain competitive. Based on this example, what degree of competition exists in the airline industry? Select one: O a. monopolistic competition O b. oligopoly O C. perfect competition O d. not enough information to answer O e. Monopoly Barrow_forward

- 7. Suppose that the inverse market demand for pumpkins is given by P = $10-0.050. Pumpkins can be grown by any- one at a constant marginal cost of $1. ena. If there are lots of pumpkin growers in town so that the pumpkin industry is competitive, how many pumpkins will be sold, and what price will they sell for? b. Suppose that a freak weather event wipes out the pumpkins of all but two producers, Linus and Lucy. Mesob 0 17050arrow_forwardQUESTION 1 Press F11 to exit full screen Which firm would earn profit in the long-run? O a monopolist firm. O a monopolistically competitive firm. O an oligopoly firm. O a perfectly competitive firm. QUESTION 2 Refer to the graph below for a monopolistically competitive firm. ↑Price MC 160 140 ATC 123.33 Demand 90 56.67 MR 100 133.33 154.92 Quantity If the above firm chose to produce at 100 units then the firm will be O earning a profit O incurring a loss O there is no profit and no loss O the firm can earn, profit, loss or break evenarrow_forwardKate and Alice are small-town ready-mix concrete duopolints. The market demand tunction is o- 20,000 - 200Pwhere Pis the price of a cubic yard of concrete and Ois the number of cubic yards demanded per year. Marginal cost is sa0 per cubic yard. Suppose Kate onters the market first and chooses her output belore Alice. What is the difference in Alice's profit when Kata enters the market tirst, compared to when they simultanecusly select ther outputa? When Kate entors the markat first, Alice's profit is $3,888.a0 lower. O When Kate enters the market fest, Alice's profit is 513,333.33 lower. O When Kate enters the market first, Alice's profit is $5,000 lower. O When Kate onters the market first, Alice's proft is $1.111.11 higher,arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education