ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

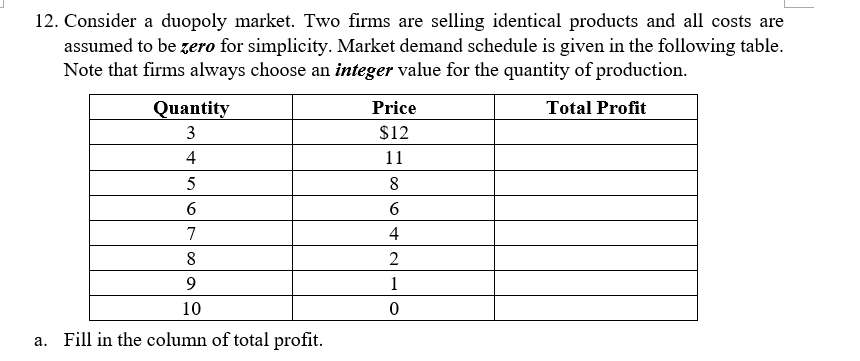

Transcribed Image Text:12. Consider a duopoly market. Two firms are selling identical products and all costs are

assumed to be zero for simplicity. Market demand schedule is given in the following table.

Note that firms always choose an integer value for the quantity of production.

Quantity

Price

Total Profit

3

$12

4

11

5

8

6

6.

7

4

8

2

1

10

a. Fill in the column of total profit.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- 3. The components of marginal revenue Alex's Fire Engines is the sole seller of fire engines in the fictional country of Pyrotania. Initially, Alex produced eight fire engines, but he has decided to increase production to nine fire engines. The following graph shows the demand curve Alex faces. As you can see, to sell the additional engine, Alex must lower his price from $80,000 to $40,000 per fire engine. Note that while Alex gains revenue from the additional engine he sells, he also loses revenue from the initial eight engines because he sells them all at the lower price. Use the purple rectangle (diamond symbols) to shade the area representing the revenue lost from the initial eight engines by selling at $40,000 rather than $80,000. Then use the green rectangle (triangle symbols) to shade the area representing the revenue gained from selling an additional engine at $40,000. dollars per fire engine) PRICE (Thousands Alex 200 180 160 140 120 100 80 60 40 20 0 0 + 1 True + False 2 + 4…arrow_forwardPlease see the images of the article below and help answer questions. 3. Interpret this statement: "[Economists] see individuals and businesses as interchangeable atoms, not as unique creators. Their theories describe an equilibrium state of perfect competition because that is what's easy to model, not because it represents the best of business." Is the statement correct? Do economists have theories of monopoly and oligopoly as well? Does economic theory contend that for every product, the market for the product should be perfectly competitive? Does economic theory recommend that under certain conditions, products or production processes should be patented?arrow_forward3. The components of marginal revenue Bob's Fire Engines is the sole seller of fire engines in the fictional country of Pyrotania. Initially, Bob produced five fire engines, but he has decided to increase production to six fire engines. The following graph shows the demand curve Bob faces. As you can see, to sell the additional engine, Bob must lower his price from $160,000 to $120,000 per fire engine. Note that while Bob gains revenue from the additional engine he sells, he also loses revenue from the initial five engines because he sells them all at the lower price. Use the purple rectangle (diamond symbols) to shade the area representing the revenue lost from the initial five engines by selling at $120,000 rather than $160,000. Then use the green rectangle (triangle symbols) to shade the area representing the revenue gained from selling an additional engine at $120,000. PRICE (Thousands of dollars per fire engine) 200 180 160 140 120 100 80 60 40 20 0 + 0 1 2 Bob in this scenario.…arrow_forward

- E3arrow_forwardion 4 of 20 The accompanying graph depicts the marginal cost (MC), average total cost (ATC), and marginal revenue (MR) curves A Perfectly Competitive Firm for a perfectly (or purely) competitive firm. 20 19 MC Move point A to identify the profit maximizing price and 18 17 quantity for this firm. 16 15 14 ATC 13 MR = D 12 11 10 9 8 6 5 4 3 A 1 0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 Quantity Price and Costarrow_forwardRefer to Figure K.. If there were four identical firms in this competitive industry, which of the following price-quantity combinations would be on the market supply curve? Point A B C D (A) A and C only B) Bonly C) B and D only D) A only Price (Dollars) 4 4 Quantity (Units) 16 32 32 6 6 8 64 64arrow_forward

- solve botharrow_forwardThe makers of Tylenol pain reliever do a lot of advertising and have very loyal customers. In contrast, the makers of generic acetaminophen do no advertising, and their customers shop only for the lowest price. Assume that the marginal costs of Tylenol and generic acetaminophen are the same and constant. a) Draw a diagram showing Tylenol's demand, marginal revenue and marginal cost curves. Label Tylenol's price and mark-up over marginal cost. b) Repeat part (a) for a producer of generic acetaminophen. How do the diagrams differ? Which company has the bigger mark-up? Explain. c) How might barriers to entry influence the behaviour of the makers of Tylenol? d) What factors would affect the extent to which the makers of Tylenol could engage in predatory or destroyer pricing to force out competitors in this market?arrow_forward1) Briefly explain how the total revenue for a profit-seeking film is determined 2)Briefly explain what is meant by the term "fixed costs" and provide three examples of same. What determines a firm's level of fixed costs? 3)Contrast the rold of fixed costs and variable costs in economic decisions about future prodiction 4)Briefly compare and contrast the perceived demand curve for a monopolitically competitive firm and a perfectly competitive firm. 5)Briefly explain what quantity a profit maximizing monopolistic competitor will seek. Why not this type of competitive frim is productively efficient?arrow_forward

- Question 21 A firm is a price taker only when the market is perfectly competitive. only when the market is perfectly competitive or monopolistic. Oonly when the market is perfectly competitive or monopolistically competitive. when the market is perfectly competitive, monopolistically competitive, or monopolistic. Question 22arrow_forwardPArt C D E last partsarrow_forwardnot use ai please don'tarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education