Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

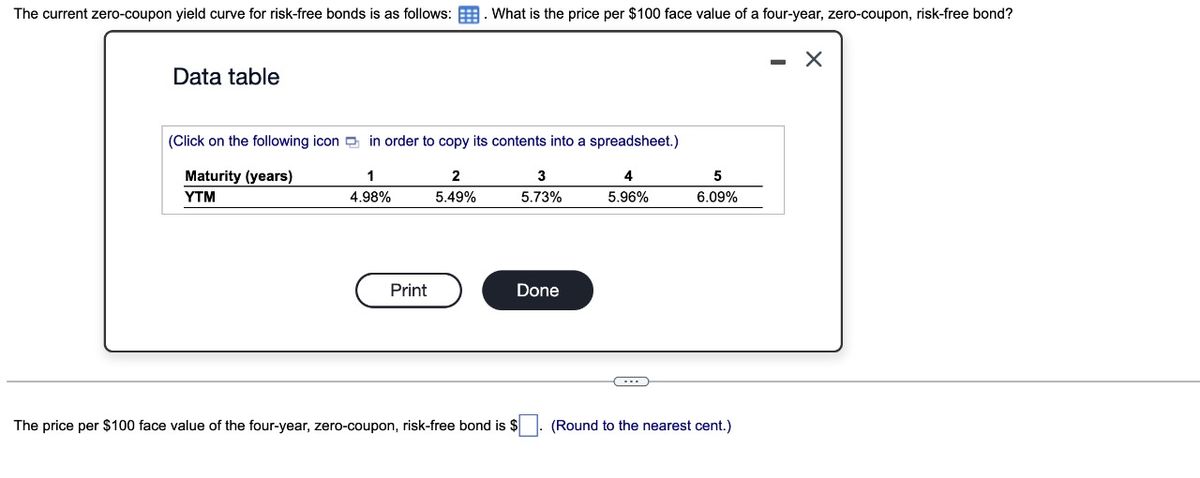

Transcribed Image Text:The current zero-coupon yield curve for risk-free bonds is as follows: . What is the price per $100 face value of a four-year, zero-coupon, risk-free bond?

Data table

(Click on the following icon in order to copy its contents into a spreadsheet.)

Maturity (years)

YTM

1

2

3

4

5

4.98%

5.49%

5.73%

5.96%

6.09%

Print

Done

The price per $100 face value of the four-year, zero-coupon, risk-free bond is $

(Round to the nearest cent.)

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- The Excel file Portfolio Bond Immunization Data contains information about three bonds. Use this data to: Yield to maturity (Expected/Current) 9% Number of Years to Future Liability 9.00 Future Liability $7,500 Bond 1 Bond 2 Bond 3 Coupon rate 6.00% 7.000% 8.00% Maturity 12 18 24 Face value 1,000 1,000 1,000 Compute the amount to be invested to meet the future liability noted in the data. This future liability is due in 9 years. Find a combination of Bond 1 and Bond 2 having a target duration of 9 years. Find a combination of Bond 1 and Bond 3 having a target duration of 9 years. Perform an analysis using a data table and an accompanying graph to determine which portfolio would be preferred to attempt to immunize this obligation. Construct a data table by varying the yield to maturity that shows the value of each portfolio at the end of 9 years. Based on your data table, construct a graph that demonstrates the performance of these…arrow_forwardBond prices. Price the bonds from the following table with semiannual coupon payments: a. Find the price for the bond in the following table: (Round to the nearest cent.) Years to Yield to Par Value $1,000.00 Data table (Click on the following icon in order to copy its contents into a spreadsheet.) Yield to Maturity 8% Par Value Coupon Rate $1,000.00 $1,000.00 $5,000.00 $1,000.00 5% 7% 6% 9% Print Years to Maturity 20 30 10 10 HTTP Done 5% 9% 11% Price ? ? ? ? - Xarrow_forwarda. Find the price for the bond in the following table: (Round to the Years to Data Table Cancel Coupon Rate 12% Par Value Maturity $1,000.00 30 (Click on the following icon in order to copy its contents into a spreadsheet.) Yield to Years to Maturity Maturity 12% Par Value Coupon Rate Price $1,000.00 $5,000.00 12% 30 11% 15 11% $5,000.00 10% 10 6% $1,000.00 8% 20 7% Print Donearrow_forward

- 4. Suppose the current zero-coupon yield curve for risk-free bonds is as follows: Maturity (years) YTM 1 3 4 3.25% 3.50% 3.90% 4.25% 4.40% The price per $100 face value of a three-year, zero-coupon, risk-free bond is closest to: A) $93.80 B) $90.06 C) $89.16 D) $86.39arrow_forward***YTC, YTM, and holding period yield they all refer to the r in the formula: P=C*[1-1/(1+r)^t]/r + F/(1+r)^t. They are just different expressions under different circumstances. 9. What is the yield to call (YTC) of a 30-year 6% bond selling for $940? The call deferment period for the bond is 10 years. Call premium=30. [Hint: It means that your N=10*2=20, and your face value=1030] 10. What is the yield to call (YTC) of a 20-year 8% bond selling for $1030? The call deferment period for the bond is 5 years. Call premium=40. [Hint: It means that your N=5*2=10, and your face value=1040] 11. Still considering the same bond as question 10, suppose you buy it today, but expect to sell it in 2 years at a YTM=4%. That is, you expect the yield to maturity on this bond to be 4% when you sell it in 2 years. What price do you expect to sell it for? What is your expected holding period yield if you buy it today and sell it at the expected sell price? 12. What is the holding period yield on a 30-year…arrow_forwardUse the same set of data to answer questions 13-15. Complete your calculation in Excel. Par value Coupon rate Frequency 2 per year Yield-to-maturity 6% Term to maturity 3 years $102.74 What's the price of the bond? $106.81 $100.00 $97.62 4% $94.58arrow_forward

- Explain why are the bond prices for A and B different or the same? Explain your answer clearly.arrow_forwardCompute yield-to-maturity for the following zero-coupon bonds: 1-year zero-coupon bond, traded currently at 980 dollars 2-years zero-coupon bond, traded currently at 920 dollars 3-years zero-coupon bond, traded currently at 840 dollars Assume that all 3 bonds have the same nominal: 1000 dollars. Using YTMs calculated plot the yield curve.arrow_forwardPlease see attached. Defintion: Coupon is the regular interest payment of a bond.arrow_forward

- Please answer all 4 price bonds with explanations thxarrow_forwardData table ↑ The current zero-coupon yield curve for risk-free bonds is as follows: What is the price per $100face value of a two-year, zero-coupon, risk-free bond? The price per $100 face value of the two-year, zero-coupon, risk-free bond is $ (Click on the following icon in order to copy its contents into a spreadsheet.) Maturity (years) YTM 1 4.98% 2 5.48% 3 5.78% Print Done 4 5 5.96% 6.09% (Round to the nearest cent.) - Xarrow_forwardO ook int ences You find the following Treasury bond quotes. To calculate the number of years until maturity, assu of the bonds have a par value of $1,000 and pay semiannual coupons. Rate ?? 6.052 6.143 Maturity Month/Year May 33 May 36 May 42 Yield to maturity Asked Bid 103.4560 103.5288 104.4900 104.6357 ?? Change Ask Yield +.3248 5.00 % +.4245 +.5353 In the above table, find the Treasury bond that matures in May 2036. What is your yield to matur Note: Do not round intermediate calculations and enter your answer as a percent rounded to 5.919 ?? 3.951arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education