Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

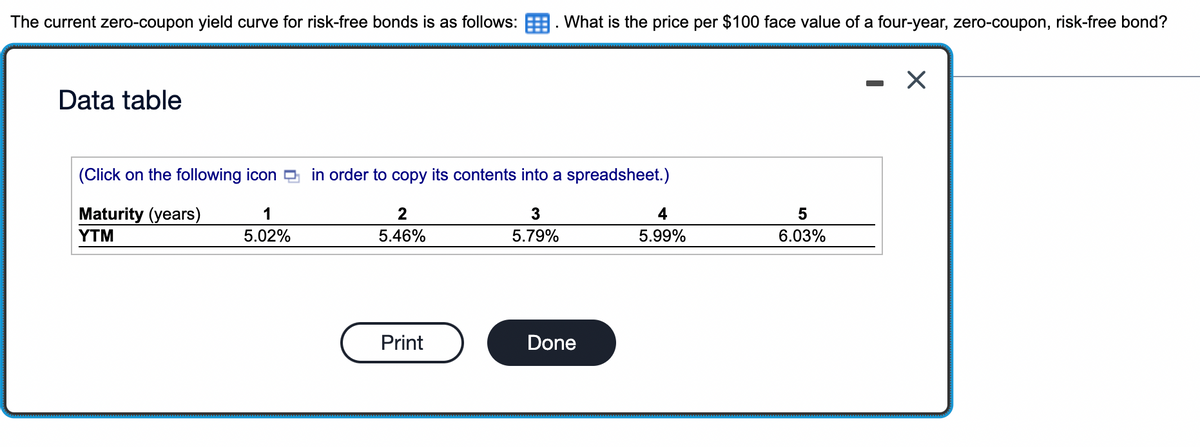

Transcribed Image Text:The current zero-coupon yield curve for risk-free bonds is as follows: . What is the price per $100 face value of a four-year, zero-coupon, risk-free bond?

Data table

(Click on the following icon D in order to copy its contents into a spreadsheet.)

Maturity (years)

1

2

4

YTM

5.02%

5.46%

5.79%

5.99%

6.03%

Print

Done

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- Problem • Suppose the following zero-coupon bonds are trading at the prices shown below per $100 face value. • Determine the corresponding yield to maturity (rate of return) for each bond. Maturity 1 year Price $96.62 2 years 3 years 4 years $92.45 $87.63 $83.06arrow_forward7. Bond Valuation: Semiannual Interest Calculate the value of each of the bonds shown in the following table, all of which pay interest semiannually. Bond Par Value Coupon Years to Maturity A $1000 10% B $800 12% C $1000 14% D $1000 8% 13 15 14 11 Required Annual Return 8% 11% 12% 10%arrow_forwardPlease show detailed steps and correct. Only by excelarrow_forward

- Maturity (years) Price 1 $97.25 $94 53 591 83 5 $87.53 $09 23 The above table shows the price per $100 face value of several risk-free, zero-coupon bonds. What is the yield to maturity of the four-year, zero-coupon, risk free bond shown? OA. 011% OB 2.00% OC. 144% OD 578 %arrow_forwardQUESTION 1 If the yield to maturity for a one year zero coupon bond is 5.2% and the yield to maturity for a 2 year zero coupon bond is 5.8%, what is the implied future short rate from year 1 to 2 (use 5 decimal places, write 3.333% as .03333)?arrow_forwardPlease answer all 4 price bonds with explanations thxarrow_forward

- solve MCQs question with proper reason and explanation I'll give you many upvotesarrow_forward4.arrow_forwardO ook int ences You find the following Treasury bond quotes. To calculate the number of years until maturity, assu of the bonds have a par value of $1,000 and pay semiannual coupons. Rate ?? 6.052 6.143 Maturity Month/Year May 33 May 36 May 42 Yield to maturity Asked Bid 103.4560 103.5288 104.4900 104.6357 ?? Change Ask Yield +.3248 5.00 % +.4245 +.5353 In the above table, find the Treasury bond that matures in May 2036. What is your yield to matur Note: Do not round intermediate calculations and enter your answer as a percent rounded to 5.919 ?? 3.951arrow_forward

- Please don’t reject question question is complete. Please answer all 4 sections. Thxarrow_forwardGive typing answer with explanation and conclusionarrow_forwardThere are two zero-coupon bonds below: Coupon Term to rate maturity 0% 1 year 10% 2 years Bond A B FV $100 $100 Price $95.24 $107.42 Consider a 2-year coupon bond C with FV = $100, coupon rate=25%, and price = $ 138. Is Bond C underpriced/overpriced relative to Bonds A and B? What is the potential arbitrage trading strategy? O a. Overpriced; Long 3/22 unit of A; Long 25/22 unit of B; Short 1 unit of C O b. Underpriced; Long 3/22 unit of A; Long 25/22 unit of B; Short 1 unit of C O c. Overpriced; Long 3 unit of A; Long 25 unit of B; Short 1 unit of C O d. Underpriced; Long 3 unit of A; Long 25 unit of B; Short 1 unit of Carrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education