Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

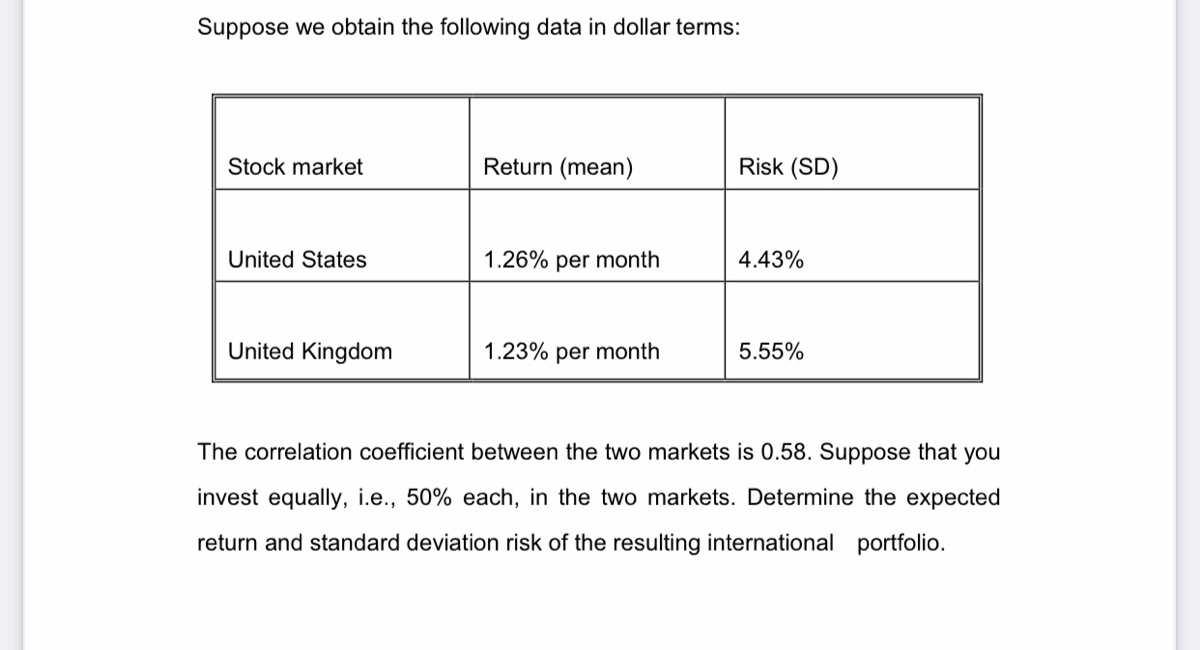

Transcribed Image Text:Suppose we obtain the following data in dollar terms:

Stock market

Return (mean)

Risk (SD)

United States

1.26% per month

4.43%

United Kingdom

1.23% per month

5.55%

The correlation coefficient between the two markets is 0.58. Suppose that you

invest equally, i.e., 50% each, in the two markets. Determine the expected

return and standard deviation risk of the resulting international portfolio.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- Consider two types of assets: market portfolio (M) and stock A. The expected return is 8% and standard deviation of the market portfolio is 15%. The risk-free rate is 2%. The standard deviation of market portfolio returns is 15%. The standard deviation of stock A is 30%, and the beta coefficient is 1. Draw the capital market line and show the position of stock A.arrow_forwardThis question assumes the standard mean-variance utility function. You are allocating your investments between a the NZX50 and a holding of (New Zealand) T-bills. The expected return on the NZX50 is 7.50%, with volatility 12.80%. In contrast, there is no risk investing in T-bills, and they will earn you a return of 4.70%. Your risk-aversion is 7. What percentage of your wealth should you allocate to Treasury bills? 34.61% 96.88% 96.51% 75.59%arrow_forwardYou have estimated the single index model (SIM) fund B and found that its alpha and beta are 0.035 and 1.1 respectively. The standard deviation of Fund B's excess returns is 30% and the market portfolio excess returns have a standard deviation of 20%. What's the information ratio of Fund B?arrow_forward

- the CAPM world, the average investor’s risk aversion parameter is 2 and the standard deviation of the market portfolio is 23%. The risk-free rate is 3.5%. What is the expected return on the market portfolio?arrow_forwardSuppose there are two independent economic factors, M1 and M2. The risk-free rate is 4%, and all stocks have independent firm-specific components with a standard deviation of 49%. Portfolios A and B are both well diversified. Portfolio Beta on M1 Beta on M2 Expected Return (%) A 1.6 2.4 39 B 2.3 -0.7 9 Required: What is the expected return–beta relationship in this economy?arrow_forwardSuppose there are two independent economic factors, M₁ and M₂. The risk-free rate is 6%, and all stocks have independent firm- specific components with a standard deviation of 46%. Portfolios A and B are both well diversified. Portfolio A Beta on M₁ 1.5 2.0 Beta on My 2.1 -0.6 Required: What is the expected return-beta relationship in this economy? (Do not round intermediate calculations. Round your answers to 2 decimal places.) Expected return-beta relationship E(rp) = Expected Return (%) 36 14 45 60 Answer is not complete. Bp1 Bp2arrow_forward

- The expected return for the investment is ??? The standard deviation is ??? While the expected return for the risk-free assets, Treasury Bills, is ??? The standard deviation is ???arrow_forwardYou are evaluating the expected performance of two stocks, Alibaba and Bank of China.You gathered the following informationRisk-free rate = 5%Expected return for a Hong Kong market = 11.5%Beta of Alibaba = 1.5Beta of Bank of China = 0.8 Based on your analysis, you forecast the return on these 2 stocks are 13.25% for Alibaba and11.25% for Bank of China.i) Calculate the required rate of return for Alibaba and Bank of Chinaii) Indicate whether each stock is undervalued, fairly valued or overvalued.arrow_forwardConsider the following information on a portfolio of three stocks: State of Economy Probability of State of Economy Stock A Rate of Return Stock B Rate of Return Stock C Rate of Return Boom.13.02.32.50 Normal.55.10.22.20 Bust .32.16.21.35 If your portfolio is invested 40 percent each in A and B and 20 percent in C, what is the portfolio's expected return, the variance, and the standard deviation? Note: Do not round intermediate calculations. Round your variance answer to 5 decimal places, e.g., 16161. Enter your other answers as a percent rounded to 2 decimal places, e. g., 32.16. If the expected T-bill rate is 4.25 percent, what is the expected risk premium on the portfolio? Note: Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e. g., 32.16.arrow_forward

- Assume that both portfolios A and B are well diversified, that E(rA) = 20% and E(rB) = 15%. If the economy has only one factor, and BetaA = 1.3, whereas BetaB = 0.8, what must be the risk-free rate (write as percentage, rounded to two decimal places)?arrow_forwardPlease help with this question with full working out.arrow_forwardNonearrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education