ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

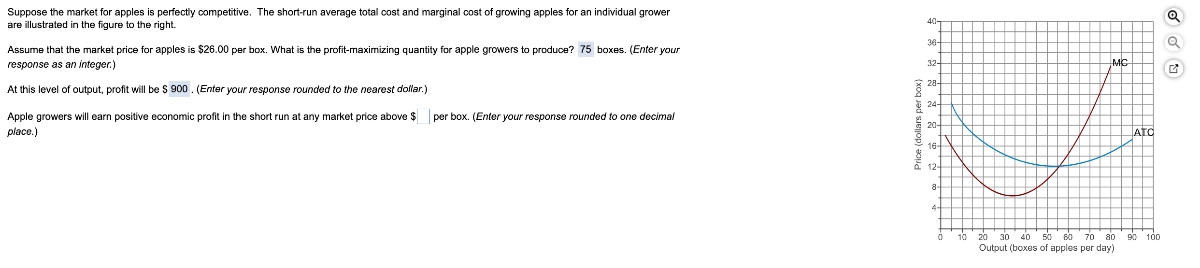

Transcribed Image Text:Suppose the market for apples is perfectly competitive. The short-run average total cost and marginal cost of growing apples for an individual grower

are illustrated in the figure to the right.

40-

36

Assume that the market price for apples is $26.00 per box. What is the profit-maximizing quantity for apple growers to produce? 75 boxes. (Enter your

response as an integer.)

32

MC

28

At this level of output, profit will be S 900. (Enter your response rounded to the nearest dollar.)

Apple growers will earn positive economic profit in the short run at any market price above $

per box. (Enter your response rounded to one decimal

20-

place.)

ATO

12-

20 30 40 so 80 70 ao 90 100

Output (boxes of apples per day)

(xoq jəd sejop) so

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps with 1 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- K A firm's profit function is (q) = R(q)-C(q)=100q- (190+40q+10q²). What is the positive output level that maximizes the firm's profit (or minimizes its loss)? What is the firm's revenue, variable cost, and profit? Should it operate or shut down in the short run? The output level at which the firm's profit is maximized is q = (Enter your response as a whole number.)arrow_forwardFirm Profit, Loss, and Shut Down Based upon the graph, answer the following questions: 1) What is the production level that will maximize the profit for the firm? 2) What is the profit-maximizing price the firm will charge? 3) Will the firm incur an economic gain or economic loss? 4) What will the dollar amount of economic gain or economic loss be? 5) What will be the price and quantity where the firm will shut down?arrow_forwardAmos McCoy is currently raising corn on his 100-acre farm and earning an accounting profit of $100 per acre. However, if he raised soybeans, he could earned an accounting profit of $200 per acre. Is he currently earning an economic profit?arrow_forward

- Consider the business whose Total Cost and Total Revenue for various quantities of a particular product are shown in the table below. Quantity Total Cost Total Revenue 0 100 0 1 250 500 2 350 950 3 500 1350 4 725 1700 5 1000 2000 6 1400 2250 Use the Profit-Maximizing Rule to explain the quantity that this business should produce to maximize its profits. Answer must both state the number to produce and an explanation of how you used the profit-maximizing rule to arrive at that number.arrow_forwardIn the short run, if a firm is having economic losses, but the profit is greater than the average variable cost, then the firm should ____________.arrow_forward50 MC ATC 40 30 MR 10 10 20 30 40 Quantity (per day) The figure above shows a perfectly competitive firm. The firm is operating; that is, the firm has not shut down. a) What is the output level should the firm produce to maximize the profit? b) What is the price does the firm charge at this output level? Price and costs (dollars) 20arrow_forward

- 100 90 90 00 80 COSTS (Dollars) 70 70 00 60 50 40 30 20 10 ATC AVC MC 0 0 5 10 15 20 25 30 QUANTITY (Thousands of snapbacks) 35 35 40 45 50 For every price level given in the following table, use the graph to determine the profit-maximizing quantity of snapbacks for the firm. Further, select whether the firm will choose to produce, shut down, or be indifferent between the two in the short run. (Assume that when price exactly equals average variable cost, the firm is indifferent between producing zero snapbacks and the profit-maximizing quantity of snapbacks.) Lastly, determine whether the firm will earn a profit, incur a loss, or break even at each price. Price (Dollars per snapback) 10 20 32 40 50 60 Quantity (Snapbacks) Produce or Shut Down? Profit or Loss?arrow_forwardAt what output rate does the firm maximize profit or minimize loss?arrow_forwardInfo in imagesarrow_forward

- Suppose the market for beans is perfectly competitive. The average total cost and marginal cost of growing beans in the long run for an individual farmer are illustrated in the graph to the right. According to the graph, the long run equilibrium price for beans is $ per box. (Enter a numeric response using a real number rounded to two decimal places.) C Price and cost (dollars per box) 10- 9- 00 N 1 0 10 MC 20 30 40 50 60 70 80 Quantity of beans (boxes per week) ATC 90 100 Narrow_forwardConsider the competitive market for steel. Assume that, regardless of how many firms are in the industry, every firm in the industry is identical and faces the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves shown on the following graph. V AVC COSTS (Dollars per ton) 100 882 889 80 20 0 MC 5 25 30 35 QUANTITY (Thousands of tons) 15 20 10 45 40 50 The following diagram shows the market demand for steel.arrow_forwardPierce Manufacturing determines that the daily revenue, in dollars, from the sale of x lawn chairs is R(x)=0.005x³ +0.02x² +0.5x Currently, Pierce sells 90 lawn chairs daily a) What is the current daily revenue? b) How much would revenue increase if 95 lawn chairs were sold each day? c) What is the marginal revenue when 90 lawn chairs are sold daily? d) Use the answer from part (c) to estimate R(91), R(92), and R(93) a) The current revenue is $ b) The revenue would increase by $ (Round to the nearest cent.) c) The marginal revenue is $ when 90 lawn chairs are sold daily. d) R(91) $ R(92) $ R(93) $arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education