ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

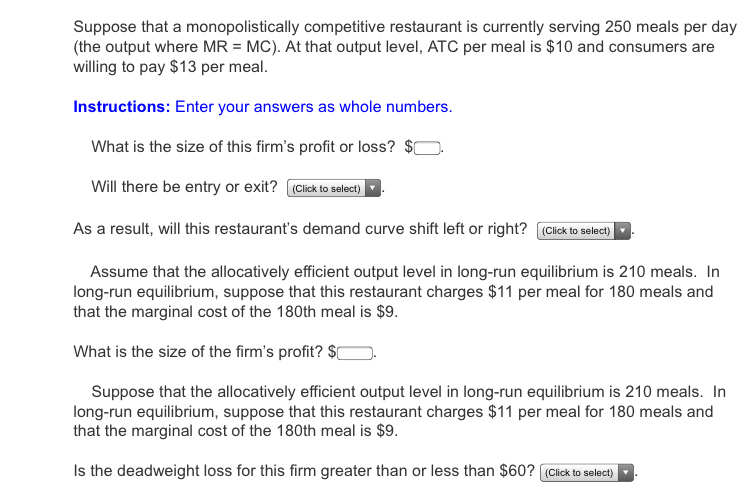

Transcribed Image Text:Suppose that a monopolistically competitive restaurant is currently serving 250 meals per day

(the output where MR = MC). At that output level, ATC per meal is $10 and consumers are

willing to pay $13 per meal.

Instructions: Enter your answers as whole numbers.

What is the size of this firm's profit or loss? $0

Will there be entry or exit? (Click to select)

As a result, will this restaurant's demand curve shift left or right? (Click to select)

Assume that the allocatively efficient output level in long-run equilibrium is 210 meals. In

long-run equilibrium, suppose that this restaurant charges $11 per meal for 180 meals and

that the marginal cost of the 180th meal is $9.

What is the size of the firm's profit? $[

Suppose that the allocatively efficient output level in long-run equilibrium is 210 meals. In

long-run equilibrium, suppose that this restaurant charges $11 per meal for 180 meals and

that the marginal cost of the 180th meal is $9.

Is the deadweight loss for this firm greater than or less than $60? (Click to select)

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Suppose that a monopolistically competitive restaurant is currently serving 230 meals per day (the output where MR = MC). At that output level, ATC per meal is $10, and consumers are willing to pay $12 per meal. What is this firm's profit or loss? Will there be entry or exit? Will this restaurant's demand curve shift left or right? In long-run equilibrium, suppose that this restaurant charges $11 per meal for 180 meals and that the marginal cost of the 180th meal is $8. What is the firm's profit? (LO3)arrow_forwardThe figure below shows the demand (D, MR) and cost (MC, ATC) curves for Gwen's Country Curtains, operating in a monopolistically competitive industry. Demand and cost conditions facing Gwen's Country Curtains MC Dollars 80 0 ATC 1,000 MR Number of curtains per month Suppose Gwen's Country Curtains is currently producing 1000 curtains per month at a price of $80. In the short run, this company is and in the long run, it should expect to a. earning zero profit; earn zero profit b. suffering a loss; earn zero profit c. suffering a loss; shut down d. making a profit; earn zero profitarrow_forwardc-State and explain briefly 2 differences between a perfectly competitive market and a monopolistic competitive market.arrow_forward

- please helparrow_forwardDE Quantity MC MR ATC Demand The graph above represents a firm in a monopolistically competitive market. Which of the following is true? The firm's profit-maximizing quantity is E. The firm is making a profit of (A - B) x D. The firm is making zero economic profits. The firm is making a loss of (A - B) x D.arrow_forwardAssume that in short-run equilibrium, a particular monopolistically competitive restaurant (Applebee's) charges $12 for each order of Chicken Parmesan and sells 52 orders per day. The average total cost (ATC) for those 52 orders is $10. How much revenue will the firm take in each day? $ What will be the firm's economic profit or loss on Chicken Parmesan? Next, suppose that other restaurants add/remove chicken parmesan from their menus (entry or exit occurs) and a long-run equilibrium is established. If the Applebees daily Chicken Parmesan orders remain at 52 units, what price will it be able to charge? $ What will be its economic profit or loss?arrow_forward

- 5- 3- 1- 20 40 60 80 100 Q MR Using the above graph, This profit-maximizing firm will produce Blank 1 units. -MC What price will this profit-maximizing firm charge? $Blank 2 (Do NOT enter the '$' in your response. Enter only the whole dollar amount; do NOT enter cents.) If the industry was perfectly competitive instead of monopolistic, then market output would be Blank 3 units and market price would be $Blank 4. (Do NOT enter the '$' in your response. Enter only the whole dollar amount; do NOT enter cents.) Blank 1 Blank 2 Blank 3 Blank 4 Add your answer Add your answer Add your answer Add your answerarrow_forwardExplain the difference in market power between perfectly competitive firms and monopolistically competitive firms. Which firms have more control over prices and/or output? Why? What are some industry examples of each type of market structure?arrow_forwardMail - Oliver, Ak X 13) Online Quiz i heducation.com/ext/map/index.html?_con=con&external_browser=0&launchUrl=https%253A%2525 1er. Excel Module 8 X 13 10 Refer to the graph for a monopolistically competitive firm in short-run equilibrium. This f 0 100 X M Question 16-LCX M Inbox (9,354) - Multiple Choice lass of $280 MC 160 180 210 Quantity ATC MR Darrow_forward

- Suppose that a monopolistically competitive restaurant is currently serving 250 meals per day (the output where MR = MC). At that output level, ATC per meal is $10 and consumers are willing to pay $12 per meal. Instructions: Enter your answers as a whole number. a. What is this firm's profit or loss? $ b. Will there be entry or exit? (Click to select) Will this restaurant's demand curve shift left or right? (Click to select) In long-run equilibrium, suppose that this restaurant charges $11 per meal for 180 meals and that the marginal cost of the 180th meal is $8. Suppose that the allocatively efficient output level in long-run equilibrium is 210 meals. c. What is the firm's profit? $ d. Is this firm's deadweight loss greater than or less than $90? (Click to select)arrow_forward3. Is monopolistic competition efficient? Suppose that a firm produces wooden train engines in a monopolistically competitive market. The following graph shows its demand curve, marginal- revenue (MR) curve, marginal-cost (MC) curve, and average-total-cost (ATC) curve. Place a black point (plus symbol) on the graph to indicate the long-run monopolistically competitive equilibrium price and quantity for this firm. Next, place a grey point (star symbol) to indicate the minimum average total cost the firm faces and the quantity associated with that cost. ? PRICE (Dollars per engine) 100 90 80 70 60 50 40 30 20 10 MC ATC MR 0 + Demand H 0 10 20 30 40 50 60 70 80 90 100 QUANTITY (Thousands of engines) Mon Comp Outcome Min Unit Cost Because this market is a monopolistically competitive market, you can tell that it is in long-run equilibrium by the fact that optimal quantity for each firm. Furthermore, the quantity the firm produces in long-run equilibrium is True or False: This indicates…arrow_forward33 and 60arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education