Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

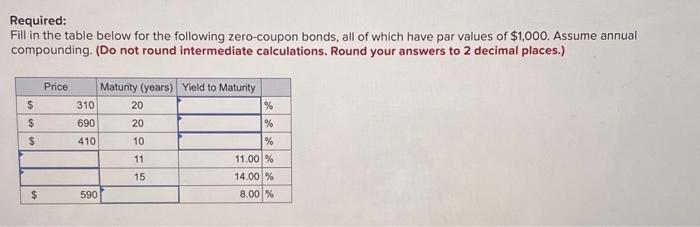

Transcribed Image Text:Required:

Fill in the table below for the following zero-coupon bonds, all of which have par values of $1,000. Assume annual

compounding. (Do not round intermediate calculations. Round your answers to 2 decimal places.)

$

$

$

$

Price

310

690

410

590

Maturity (years) Yield to Maturity

20

20

10

11

15

%

de de

%

%

11.00 %

14.00 %

8.00 %

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- Prices of zero-coupon bonds reveal the following pattern of forward rates: Year 1 2 3 Forward Rate 4% 5 6 In addition to the zero-coupon bond, investors also may purchase a 3-year bond making annual payments of $40 with par value $1,000. Required: a. What is the price of the coupon bond? Note: Do not round intermediate calculations. Round your answer to 2 decimal places. b. What is the yield to maturity of the coupon bond? Note: Do not round intermediate calculations. Round your answer to 2 decimal places. c. Under the expectations hypothesis, what is the expected realized compound yield of the coupon bond? Note: Do not round intermediate calculations. Round your answer to 2 decimal places. d. If you forecast that the yield curve in 1 year will be flat at 5.5%, what is your forecast for the expected rate of return on the coupon bond for the 1-year holding period? Note: Do not round intermediate calculations. Round your answer to 2 decimal places. a. Price b. Yield to maturity c.…arrow_forwardOnly D & E pleasearrow_forwardZero-Coupon Bonds (ZCBS) with maturity in 1 and 5 years are available on the market. Their redemption value is £100, and they sell for £90 (1-year ZCB) and £84 (5-year ZCB). Find the spot rates corresponding to the ZCBs' prices 数字 i1 = % i5 数字 Enter a percentage correct to 2 decimal places % Calculate the forward rate 1,5 i1,5 数字 Enter a percentage correct to 2 decimal places %arrow_forward

- Please answer all 4 prices with explanations thxarrow_forwardConsider the following $1,000 par value zero-coupon bonds: Bond Maturity A 1 BU C D Years until Yield to Interest rate 2 3 Maturity (years) 1 2 3 4 Maturity 8.00% 9.00 9.50 10.00 Required: a. According to the expectations hypothesis, what is the market's expectation of the one-year interest rate three years from now? (Do not round intermediate calculations. Round your answer to 2 decimal places.) b. What are the expected values of next year's yields on bonds with maturities of (a) 1 year; (b) 2 years; (c) 3 years? (Do not round intermediate calculations. Round your answer to 2 decimal places.) YTM Check my work % % % %arrow_forwardRolling Company bonds have a coupon rate of 6.20 percent, 25 years to maturity, and a current price of $1,196. What is the YTM? The current yield? (Do not round intermediate calculations. Enter your answers as a percent rounded to 2 decimal places.) YTM % Current yield %arrow_forward

- 4) A 10 year bond with $50, 000 face value has semiannual coupon rate 4% and semiannual yield rate 2%. Fill out the following amortization table. Principle Outstanding t Payment Interest герaid Balance 1 2 3 12arrow_forward6. The Mariposa Co. has two bonds outstanding. One was issued 25 years ago at a coupon rate of 9%. The other was issued 5 years ago at a coupon rate of 9%. Both bonds were originally issued with terms of 30 years and face values of $1,000. The going interest rate is 14% today. a. What are the prices of the two bonds at this time? b. Discuss the result of part (a) in terms of risk in investing in bonds.arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education