ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

thumb_up100%

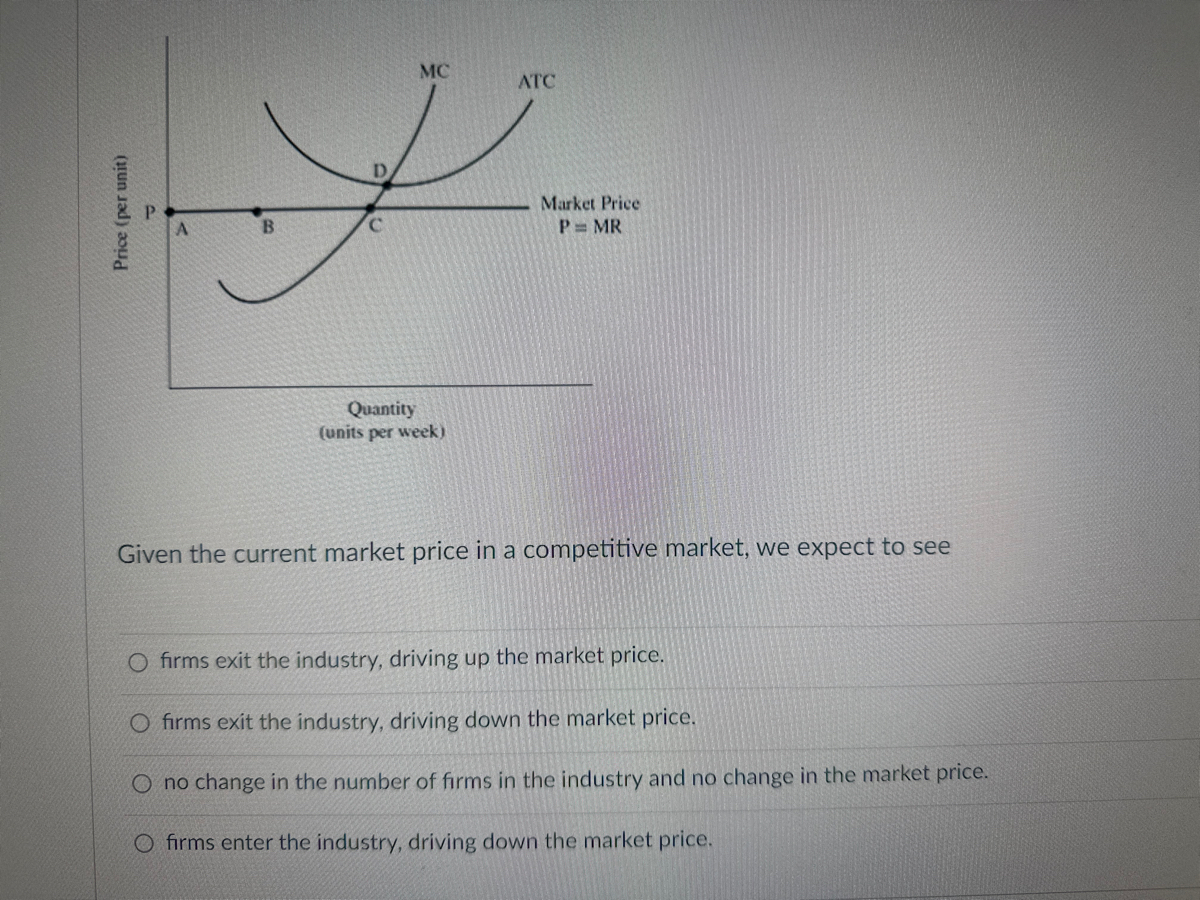

Transcribed Image Text:Price (per unit)

MC

D

P

B

Quantity

(units per week)

ATC

Market Price

P= MR

Given the current market price in a competitive market, we expect to see

O firms exit the industry, driving up the market price.

O firms exit the industry, driving down the market price.

O no change in the number of firms in the industry and no change in the market price.

O firms enter the industry, driving down the market price.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- A local pizzeria only servers two items: pizzas and sandwiches. An increase in the demand for sandwiches will result in which of the following for the firm? O an increase the opportunity cost of producing pizzas O an increase in the amount of resources the firm devotes to producing pizzas O a decrease in the price of bread a decrease in the price of sandwiches a decrease in the firm's overall revenuearrow_forwardA mattress company operates in a perfectly-competitive environment. If the firm can increase its profits by increasing output, O price is greater than marginal cost. O price is less than marginal cost. O price is equal to marginal cost. losses are minimized.arrow_forwards 1, 12 & 13 Assignment Saved Help Save & Exit Assume a purely competitive increasing-cost industry is in long-run equilibrium. If a decline in demand occurs, firms will Multiple Choice leave the industry, price will fall, and quantity produced will rise. enter the industry and price and quantity will both rise. leave the industry and price and quantity will both rise. leave the industry, price will fall, and quantity produced will fall.arrow_forward

- Price (dollars) 8 7 6 5 4 3 2 1 0 80 O increase; increase; increase O remain same; remain same; decrease O decrease; remain same; decrease O decrease; decrease; decrease Short-run Short-run MC AC 100 110 The graph above shows the cost curves for a firm selling in a perfectly competitive market. If the market demand falls due to a recession, the long run equilibrium price will output will ., the firm's and industry output will Output (per day) Long-run ACarrow_forwardPrice (dollars per soda) 2.50 2.00 1.50 1.00 0.50 Market Price 0 5 10 15 20 25 Quantity (thousands of sodas per month) The supply curve of Coca Cola is given above. The market price is $1.00 per soda. The marginal cost of the 20,000th soda is $0.50. $1.00. more than $1.00. $0.00. Sarrow_forward10. In a competitive market, the current equilibrium price is $200 per unit. A firm that produces Q units of output in this market has a short-run Total Cost (TC) given by TC = 8000 + 40Q + Q². What is the marginal cost for this firm? How many units should the firm produce?arrow_forward

- 13. Firms in Competitive Markets The market for fertilizer is perfectly competitive. Firms in the market are producing output but are currently making economic losses. Which of the following statements is true about the price of fertilizer? Check all that apply. The price of fertilizer must be less than average total cost. Price and Costs The price of fertilizer must be less than marginal cost. The price of fertilizer must be equal to average variable cost. The following graphs show the cost curves faced by a typical firm, the demand for fertilizer, and possible price and supply curves. MC Firm ATC LAVC II II Quantity (? P P₂ Demand 1 Market Quantity S₁ S₂ (?)arrow_forward20 12 10 0 MC ATC -MR 10 Quantity (units) Figure 11.4.1 Refer to Figure 11.4.1, which shows the cost curves and marginal revenue curve of a firm in a perfectly competitive market. In the long run, market O supply will decrease. demand will decrease. O supply and market demand will decrease. supply will increase. O demand will increase.arrow_forwardUrgently needarrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education