ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

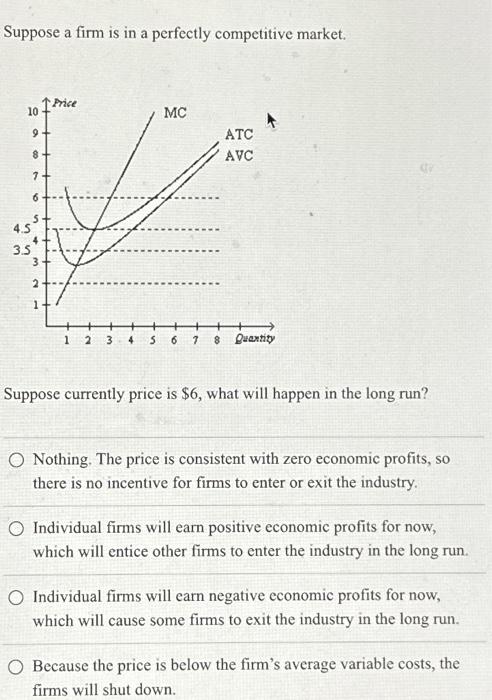

Transcribed Image Text:Suppose a firm is in a perfectly competitive market.

10 Price

9-

8

4.5³

3.5

MC

ATC

AVC

123 4 5 6 7 8 Quantity

Suppose currently price is $6, what will happen in the long run?

O Nothing. The price is consistent with zero economic profits, so

there is no incentive for firms to enter or exit the industry.

O Individual firms will earn positive economic profits for now,

which will entice other firms to enter the industry in the long run.

O Individual firms will earn negative economic profits for now,

which will cause some firms to exit the industry in the long run.

O Because the price is below the firm's average variable costs, the

firms will shut down.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 4 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Resources Submit All Question 9 of 30 The accompanying graph depicts the cost curves of an individual firm in a perfectly (or purely) competitive industry. a. Use the line labeled 'Supply' to trace out the firm's Short-Run supply curve. 20 Supply Marginal cost 19 18 17 16 Average total cost 15 14 13 Average variable cost 12 11 10 8. 7. 4 3. 2 15 21 24 27 30 33 36 39 12 46°F A 18 a 1Oarrow_forwardQuantity Price 0 20 1 18 2 16 3 14 4 12 5 10 Are the price and quantity combinations above for a perfectly competitive industry? Select one: O a. No, they are not because the demand curve should be perfectly elastic. O b. No, because the quantities are too low. O c. Yes, they are because the demand curve is downward sloping. O d. Yes, they are because the price falls the same amount for each increase in quantity. Note:- Do not provide handwritten solution. Maintain accuracy and quality in your answer. Take care of plagiarism. Answer completely. You will get up vote for sure.arrow_forwardNeed now please .arrow_forward

- On the preceding graph, use the blue rectangle (circle symbols) to fill in the area that represents profit or loss of the firm given the market price of $20 and the quantity of production from your previous answer. Note: In the following question, enter a positive number regardless of whether the firm earns a profit or incurs a loss. The rectangular area represents a short-run thousand per day for the firm. ofarrow_forwardSuppose that firm is currently producing 15 units of a good at a market price of $12. The firm has a MC of $12 and an average total cost of $8. What is the firm's economic profit and is it maximizing profits? O $0, yes O $60, no $60, yes O $0, no Note:- Do not provide handwritten solution. Maintain accuracy and quality in your answer. Take care of plagiarism. Answer completely. You will get up vote for sure.arrow_forwardEconomics A firm's total cost function is given by: TC = 2000 + 16400Q - 32Q2 + 0.016Q What is the minimum price the firm can accept so it does not have to shut down in the short-run? Select one: O a. 100 O b. 250 O c. 400 O d. None of the abovearrow_forward

- 2. Suppose that the market for wind chimes is a competitive market. The following graph shows the daily cost curves of a particular firm operating in this PRICE (Dollars per wind chime) 40 36 32 28 24 20 16 2 8 4 0 0 MC 2 ATC AVC 6 4 8 QUANTITY (Thousands of wind chimes per day) + 10 12 14 16 18 20 market: a) In short run, at a market price of $26 per wind chime, how much will firm choose to produce per day? How do you know? b) If the market price is $26 in the short run, and the firm chooses to produce the quantity you obtained in question (a), indicate the area that represents firm's profit or loss in short run on the graph. c) What is this firm's shutdown price, that is the price below which it is optimal for the firm to shut down in short run? d) long run, all firms can enter and exit the market, and all entram the same costs as above. As this markarrow_forwardA firm facing a demand curve will have zero quantity demanded if it raises its price above the market price. a. perfectly elastic O b. relatively elastic O c. relatively inelastic O d. perfectly inelastic A perfectly competitive firm is breaking even. In the short run it should In the long run it should a. produce where MC = MR; keep the same production level O b. produce where MC = MR; leave the industry O c. shut down; exit the industry O d. shut down; expandarrow_forwarddo fast i will 5 upvotes.arrow_forward

- In a competitive market with free entry and exit from the market a permanent rise in demand will lead to Select one or more: O a. excess profits being made in the short run (before new firms can enter) O b. entry by new firms O c. a permanent rise in prices O d. normal profits being made in the long-runarrow_forwardSolve it correctlyarrow_forward1arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education