Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

help please answer in text form with proper workings and explanation for each and every part and steps with concept and introduction no AI no copy paste remember answer must be in proper format with all working

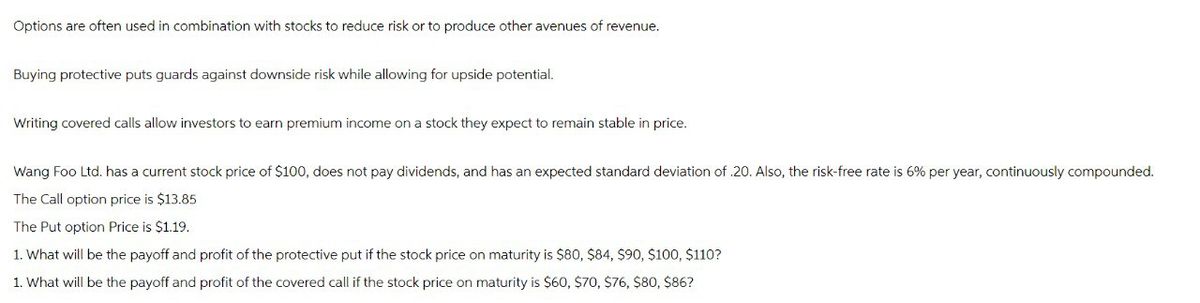

Transcribed Image Text:Options are often used in combination with stocks to reduce risk or to produce other avenues of revenue.

Buying protective puts guards against downside risk while allowing for upside potential.

Writing covered calls allow investors to earn premium income on a stock they expect to remain stable in price.

Wang Foo Ltd. has a current stock price of $100, does not pay dividends, and has an expected standard deviation of .20. Also, the risk-free rate is 6% per year, continuously compounded.

The Call option price is $13.85

The Put option Price is $1.19.

1. What will be the payoff and profit of the protective put if the stock price on maturity is $80, $84, $90, $100, $110?

1. What will be the payoff and profit of the covered call if the stock price on maturity is $60, $70, $76, $80, $86?

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps

Knowledge Booster

Similar questions

- g. BABA is a volatile stock and its stock price is expected to fluctuate within ±+50% from its current price level ($20). To avoid getting a marginal call, Jeremy can put more cash into his brokerage account when he first establishes the long position, i.e., his initial margin is larger than the IMR which is at 50%. What is the initial margin such that he will never get a margin call? Assume the price drop happens immediately after he purchases the stock.arrow_forwardPlease don't use Ai solutionarrow_forwardA stock has not been fluctuating much in price. Its average price is $20/share. You expect that the stock price behaves the same way in the next year. A one-year put option is selling for $5, which has an exercise price of $20. Suppose the risk-free rate is 0.05. To make use of your expectation in the future price movement, you establish a straddle strategy to maximize your profits. If the stock price actually ends up at $20 in a year, your profit is $ . Give your answer to 2 decimal places.arrow_forward

- A stock can either return -10% in recession or a +20% when the economy is doing well. If both possibilities are equally likely what is the expected return and standard deviation. If the T.Bill rate is 5% and investors conlude that that the stock is neither overpriced or underpriced )priced right), what must be the market risk of the stock. Explain.arrow_forwardIf a firm cannot invest retained earnings to earn a rate of return______________ (Pick either A- greater than or equal to or B- Less than) the required rate of return on retained earnings, it should return those funds to its stockholders. The current risk-free rate of return is 4.60% and the current market risk premium is 6.10%. Green Caterpillar Garden Supplies Inc. has a beta of 1.56. Using the Capital Asset Pricing Model (CAPM) approach, Green Caterpillar’s cost of equity is_____________% Cute Camel Woodcraft Company is closely held and, as a result, cannot generate reliable inputs for the CAPM approach. Cute Camel’s bonds yield 10.20%, and the firm’s analysts estimate that the firm’s risk premium on its stock relative to its bonds is 3.50%. Using the bond-yield-plus-risk-premium approach, the firm’s cost of equity is___________% The stock of Cold Goose Metal Works Inc. is currently selling for $25.67, and the firm expects its dividend to be $2.35…arrow_forwardThe stock of BP, a flood insurance provider, has a marketed beta of .8. The risk free rate is 3%. You estimate that the market risk premium is 5%. Compute the expected return for BP stock. Assume that BP’s true expected return is 8%. What is BP’s stock’s alpha assuming that CAPM is the correct asset pricing model? Is BP stock fairly priced, underpriced, or overpriced? Please explain your answerarrow_forward

- Although investing all at once works best when stock prices are rising, dollar-cost averaging can be a good way to take advantage of a fluctuating market. Dollar-cost averaging is an investment strategy designed to reduce volatility in which securities are purchased in fixed dollar amounts at regular intervals regardless of what direction the market is moving. This strategy is also called the constant dollar plan. You are considering a hypothetical $1,200 investment in a media company's stock. Your choice is to invest the money all at once or dollar-cost average at the rate of $100 per month for one year. Assume that the company allows you to purchase "fractional" shares of its stock. (a) If you invested all of the money in January and bought the shares for $12 each, how many shares could you buy? shares (b) From the following chart of share prices, calculate the number of shares that would be purchased each month using dollar-cost averaging and the total shares for the year. Round to…arrow_forwardAlthough investing all at once works best when stock prices are rising, dollar-cost averaging can be a good way to take advantage of a fluctuating market. Dollar-cost averaging is an investment strategy designed to reduce volatility in which securities are purchased in fixed dollar amounts at regular intervals regardless of what direction the market is moving. This strategy is also called the constant dollar plan. You are considering a hypothetical $1,200 investment in a media company's stock. Your choice is to invest the money all at once or dollar-cost average at the rate of $100 per month for one year. Assume that the company allows you to purchase "fractional" shares of its stock. (a) If you invested all of the money in January and bought the shares for $12 each, how many shares could you buy? shares (b)From the following chart of share prices, calculate the number of shares that would be purchased each month using dollar-cost averaging and the total shares for the year.…arrow_forwardPlease help with this question with full working out.arrow_forward

- Use the following forecasted financials: (Certain cells were left intentionally blank by asker) You may need to use the CAPM model. Assume beta equals 1.09, the risk-free rate is 1.62%, and the market risk premium is 4.72%. d) Calculate the terminal value and the present value of the terminal value. Assume a long-term growth rate of 3%. e) Calculate Sherwin Williams value per share. The company has 263.3 million shares outstanding.arrow_forwardJJM has a beta coefficient of 1.2. currently the risk free rate is 2 percent and the anticipated return on the market is 8 percent. JJM pays a $4.50 dividend that is growing at 4 percent annually. A. what is the required return for JJM? B. GIVEN THE REQUIRED RETURN, WHAT IS THE VALUE OF THE STOCK? C. IF THE STOCK IS SELLING FOR $100, WHAT SHOULD YOU DO? D. IF THE BETA COEFFICIENT DECLINES TO 1.0, E=WHAT IS THE NEW VALUE OF THE STOCK? E. IF THE PRICE REAMINS $100, WHAT COURSE OF ACTION SHOULD YOU TAKE GIVEN THE VALUATION IN D?arrow_forwardDon't provide handwritten solution. Suppose Company A's stock return has a volatility of 50% and its correlation with the Market Portfolio is 80%. The expected return on the Market Portfolio is 7%, the volatility of the Market Portfolio is 20%, and the riskfree interest rate is 1%. Calculate the expected rate of return on the stock of Company A. Type your answer below, in percentage terms rounded to the nearest whole percent (e.g., 8.05% would be written as 8)arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education