MATLAB: An Introduction with Applications

6th Edition

ISBN: 9781119256830

Author: Amos Gilat

Publisher: John Wiley & Sons Inc

expand_more

expand_more

format_list_bulleted

Related questions

Question

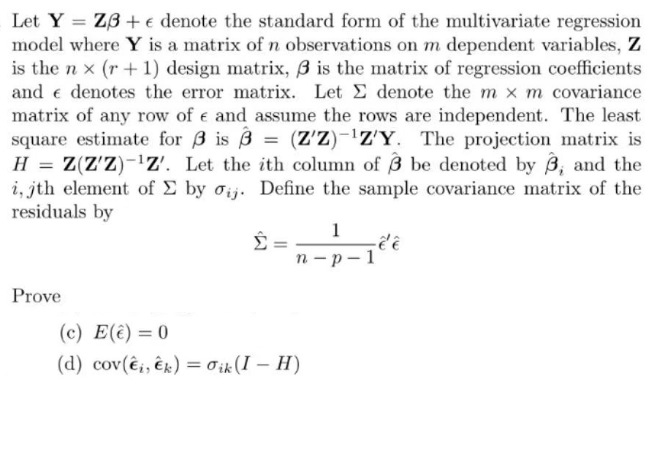

Transcribed Image Text:Let Y Z3+ e denote the standard form of the multivariate regression

model where Y is a matrix of n observations on m dependent variables, Z

is the nx (r + 1) design matrix, 3 is the matrix of regression coefficients

and denotes the error matrix. Let Σ denote the m x m covariance

matrix of any row of € and assume the rows are independent. The least

square estimate for 3 is 3 (Z'Z)-¹Z'Y. The projection matrix is

H = Z(Z'Z)-¹Z'. Let the ith column of 3 be denoted by 3, and the

i, jth element of Σ by oij. Define the sample covariance matrix of the

residuals by

Prove

Σ

=

1

n-p-1

(c) E(ê) = 0

(d) cov(ei, k) = Oik (I-H)

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 4 steps

Knowledge Booster

Similar questions

- The following table gives the experience (in years) and the number of computers sold during the previous three months by seven salespersons.Experience ( years)4129610167Computer sold {unit)194228313935211) Determine both dependent and independent variables, and explain the expected relationship between them.2) Calculate the correlation coefficient and the determinant coefficient. Explain what they mean.3) Estimates the simple regression model and comment on the estimated coefficients.4) Predict the number of computers sold during the past three months by salespersons with eleven years of experience.arrow_forwardThe regression linear model between two variables X and Y, in pairs, defined as X=[4,2,3,5,2,4] and Y=[6,4,6,8,5,10] is equal to" 1.364x+1.955 1.364x+3.125 1.955x+1.364 1.25x+2 2x+1.25 correct option?arrow_forwardConsider the one-variable regression model Yi = β0 + β1Xi + ui and suppose that it satisfies the least squares assumptions .The regressor Xi is missing, but data on a related variable, Zi, are available, and the value of Xi is estimated usingX ̃i = E(Xi | Zi). Let wi = X ̃ i - Xi.a. Show that X ̃i is the minimum mean square error estimator of Xi using Zi. That is, let X^i = g(Zi) be some other guess of Xi based on Zi, and show that E[(X^i - Xi)2] ≥ E[(X ̃i - Xi)2].b. Show that E(wi | X ̃i) = 0.c. Suppose that E(ui | Zi) = 0 and that X ̃i is used as the regressor in place of Xi. Show that β^1 is consistent. Is β^0 consistent?arrow_forward

- Suppose you want to test whether X2 and X3 can jointly explain Y in the following regression model: Y = Bo + B1X1 + B,X2 + B3X3 + u You obtain data for 85 observations and conduct a joint test of significance at 1% level. Your restricted model is given by, OY = Bo + B3X3 +u OY = Bo + B1X1 + B3 X3 + u OY = Bo + B1X1 + u OY = Bo + uarrow_forwardEach of 25 teenage girls with one brother was asked to provide her own height (y), in inches, and the height (x), in inches, of her brother. The scatterplot below displays the results. Only 22 of the 25 pairs are distinguishable because some of the (x,y) pairs were the same. The equation of the least-squares regression line is ŷ = 35.1 + 0.427x.*Girls are on the y-axis and brothers are on the x-axis* a.) Draw the least-squares regression line on the scatterplot above. b.) One brother’s height was x = 67 inches and his sister’s height was y = 61 inches. Circle the point on the scatterplot above that represents this pair and draw the segment on the scatterplot that corresponds to the residual for it. Give a numerical for the residual. c.) Suppose the point x = 84 , y = 71 is added to the data set. Would the slope of the least squares regression line increase, decrease, or remain about the same?Explain. Would the correlation increase, decrease, or remain about the same? Explain.arrow_forward(Yi, X1i, X2i) satisfy the assumptions. You are interested in β1, the causal effect of X1 on Y . Suppose that X1 and X2 are uncorrelated. You estimate β1 by regressing Y onto X1 (so that X2 is not included in the regression). Does this estimator suffer from omitted variable bias? Explain.arrow_forward

- Heteroscedasticity Stigler and Friedland (1983) conducted a study to determine whether the separation of company control from company ownership affects company profits. Using data from 69 companies in the United States, the authors estimate the following model: profiti = α + β1asseti + β2management_controli + ei Where i is company and: profiti = annual profit (in million dollar) asseti = company asset (in million dollar) management_controli = dummy variable that is worth one if the control of the company is held by the manager The regression results are presented in the table in the picture a. Explain whether the statements below are TRUE, FALSE, or CANNOT BE DETERMINED. "If there is a heteroscedasticity problem, the confidence interval of the OLS estimator is not valid." b. Determine the 95% confidence interval for the parameter 2, what can you conclude?arrow_forwardThe null hypothesis being tested in the least-squares regression output for B is B1 = B1,0=1. True Falsearrow_forwardThe y-interept bo of a least-squares regression line has a useful interpretation only if the x-values are either all positive or all negative. Determine if the statement is true or false. Why? If the statement is false, rewrite as a true statement.arrow_forward

- Suppose we have a multiple regression model with 2 predictors and an intercept. (Without any interaction or higher order terms, we have only the 2 predictors in the model and the intercept.) We have only n= 6 observations (so it would be rather silly to fit this model to this data, but let's pretend it is reasonable). We find the values of the first 5 residuals are: 2.6, 2.3, 2.5, -1.5, -1.4 What is the value of MSRes for this multiple regression model?arrow_forwardStudents who complete their exams early certainly can intimidate the other students, but do the early finishers perform significantly differently than the other students? A random sample of 37 students was chosen before the most recent exam in Prof. J class, and for each student, both the score on the exam and the time it took the student to complete the exam were recorded. a. Find the least-squares regression equation relating time to complete (explanatory variable, denoted by x, in minutes) and exam score (response variable, denoted by y) by considering Sx = 15, sy = 17,r = 39.706, x = 90, ỹ = 78 b. The standard error of the slope of this least-squares regression line was approximately (Sp) is 20.13. Test for a significant positive linear relationship between the two variables exam score and exam completion time for students in Prof. J's class by doing a hypothesis test regarding the population slope B1. Write the null and Alternate hypothesis and conclude the results. (Assume that…arrow_forwardA manufacturer of phone batteries determines that the average length of talk time for one of its batteries is 470 minutes. Suppose that the standard deviation is known to be 32 minutes and that the data are approximately bell-shaped. Estimate the percentage of batteries whose talk time is between 406 minutes and 534 minutes. Estimate the percentage of batteries whose talk time is less than 438 minutes. Estimate the percentage of batteries whose talk time is more than 534 minutes. answer in excelarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- MATLAB: An Introduction with ApplicationsStatisticsISBN:9781119256830Author:Amos GilatPublisher:John Wiley & Sons Inc

Probability and Statistics for Engineering and th...StatisticsISBN:9781305251809Author:Jay L. DevorePublisher:Cengage Learning

Probability and Statistics for Engineering and th...StatisticsISBN:9781305251809Author:Jay L. DevorePublisher:Cengage Learning Statistics for The Behavioral Sciences (MindTap C...StatisticsISBN:9781305504912Author:Frederick J Gravetter, Larry B. WallnauPublisher:Cengage Learning

Statistics for The Behavioral Sciences (MindTap C...StatisticsISBN:9781305504912Author:Frederick J Gravetter, Larry B. WallnauPublisher:Cengage Learning  Elementary Statistics: Picturing the World (7th E...StatisticsISBN:9780134683416Author:Ron Larson, Betsy FarberPublisher:PEARSON

Elementary Statistics: Picturing the World (7th E...StatisticsISBN:9780134683416Author:Ron Larson, Betsy FarberPublisher:PEARSON The Basic Practice of StatisticsStatisticsISBN:9781319042578Author:David S. Moore, William I. Notz, Michael A. FlignerPublisher:W. H. Freeman

The Basic Practice of StatisticsStatisticsISBN:9781319042578Author:David S. Moore, William I. Notz, Michael A. FlignerPublisher:W. H. Freeman Introduction to the Practice of StatisticsStatisticsISBN:9781319013387Author:David S. Moore, George P. McCabe, Bruce A. CraigPublisher:W. H. Freeman

Introduction to the Practice of StatisticsStatisticsISBN:9781319013387Author:David S. Moore, George P. McCabe, Bruce A. CraigPublisher:W. H. Freeman

MATLAB: An Introduction with Applications

Statistics

ISBN:9781119256830

Author:Amos Gilat

Publisher:John Wiley & Sons Inc

Probability and Statistics for Engineering and th...

Statistics

ISBN:9781305251809

Author:Jay L. Devore

Publisher:Cengage Learning

Statistics for The Behavioral Sciences (MindTap C...

Statistics

ISBN:9781305504912

Author:Frederick J Gravetter, Larry B. Wallnau

Publisher:Cengage Learning

Elementary Statistics: Picturing the World (7th E...

Statistics

ISBN:9780134683416

Author:Ron Larson, Betsy Farber

Publisher:PEARSON

The Basic Practice of Statistics

Statistics

ISBN:9781319042578

Author:David S. Moore, William I. Notz, Michael A. Fligner

Publisher:W. H. Freeman

Introduction to the Practice of Statistics

Statistics

ISBN:9781319013387

Author:David S. Moore, George P. McCabe, Bruce A. Craig

Publisher:W. H. Freeman