ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

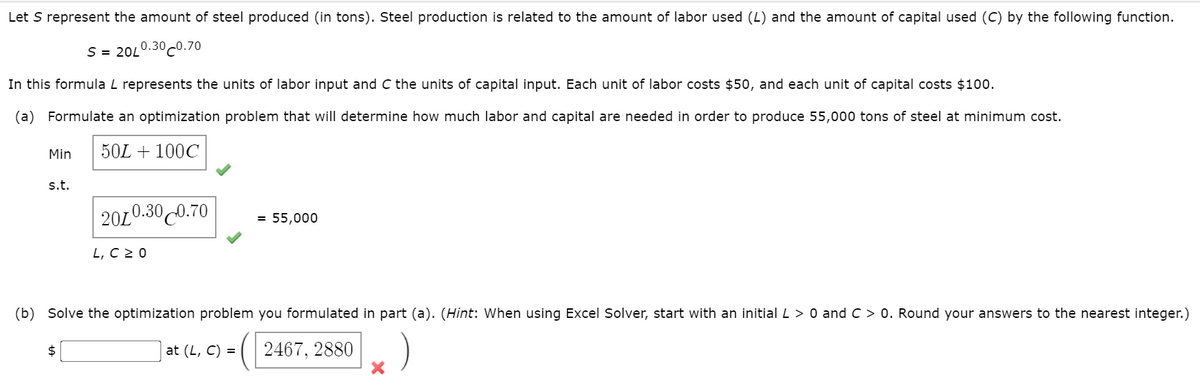

Transcribed Image Text:Let S represent the amount of steel produced (in tons). Steel production is related to the amount of labor used (L) and the amount of capital used (C) by the following function.

S = 20L

0.30c0.70

In this formula L represents the units of labor input and C the units of capital input. Each unit of labor costs $50, and each unit of capital costs $100.

(a) Formulate an optimization problem that will determine how much labor and capital are needed in order to produce 55,000 tons of steel at minimum cost.

Min

50L + 100C

s.t.

,0.300.70

20L

= 55,000

L, C 2 0

(b) Solve the optimization problem you formulated in part (a). (Hint: When using Excel Solver, start with an initial L > 0 and C > 0. Round your answers to the nearest integer.)

at (L, C) =

( 2467, 2880

2$

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 4 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- a) What are the determinants of production? Explain.b) Suppose that an economy’s production function is in the Cobb–Douglas form with parameter α = 0.3. What is the production function equation? What does each component stand for?arrow_forwardProduction function Q=100K^0.5L^0.5 .During the last production of Tyres the following inputs of 100 and 25 for capital and labor were used.What is the marginal product of capital and marginal product of labor based on the stated inputs.arrow_forwardBased on the table you created in image, Choose one isoquant and compute two MRTS at least! (for an example from point A to B and from B to C)arrow_forward

- Solve the exercise with a production function with diminishing returns: In this case, production increases as workers are added, but it increases less and less. a) Calculate the amount of production for each worker and add it to the table, taking into account the production function K 10 1 9. 2 8 3 7 4 6. 4 7 3 8 2 9 10 b) Explain why the production function exhibits diminishing returns to scale.arrow_forwardFor the Cobb-Douglas production function P and isocost line (budget constraint, in dollars), find the amounts of labor L and capital K that maximize production, and also find the maximum production. Then evaluate and give an interpretation for |å| and use it to answer the question. (a) Maximize P = 2000L3/5K2/5 with budget constraint 15L + 32OK = 8000. L = K = P = (b) Evaluate and give an interpretation for |21. Each additional dollar of budget increases production by this amount. (c) Approximate the increase in production if the budget is increased by $80. unitsarrow_forwardSuppose a pizza parlor has the following production costs: $5.00 in labor per pizza, $4.00 in ingredients per pizza, $0.10 in electricity per pizza, $2,000 in restaurant rent per month, and $250 in insurance per month. Assume the pizza parlor produces 3,000 pizzas per month. What is the variable cost of production (per month)? The variable cost of production is $ 27,300. (Enter your response as an integer.) What is the fixed cost of production (per month)? The fixed cost of production is $. (Enter your response as an integer.) Clear all Finaarrow_forward

- Which of the following production functions exhibits constant returns to scale (refer to activities and slides ): Group of answer choices q = AL0.5K0.6 q = AL0.3K0.4 q = AL0.5K0.7 Q = 10 L0.3 K0.7arrow_forwardA company produces commercials. A 2-minute commercial, for example, needs exactly 5 minutes of filming and 8 minutes of editing. Let x1 denote the minutes of filming and x2 denote the minutes of editing. a) Write down the production function and state whether it has increasing, constant, or decreasing returns to scale b) Suppose that filming costs $45 per minute and editing costs $10 per minute. To produce a 5-minute commercial, how many minutes of filming and how many minutes of editing is needed to minimize cost? c) Suppose that filming costs w1 per minute and editing costs w2 per minute. Let y denote the length (in minutes) of commericals produced. derive the conditional factor demand functions x1(w1,w2,y) and x2(w1,w2,y) and its cost function c(w1,w2,y)arrow_forwardcomplete the tablearrow_forward

- I am having trouble understanding how to answer the last part of this question. I am providing the work I did on the remainder of the problem to provide context, but the multiple choice question is what I'm stuck on. If you see an error in my previous work that would cause me to have trouble with this last question, please let me know and I will fix it. Thank you!arrow_forwardGiven the following data on input and output levels. Suppose the output price is $5 and input price is $10. Find the values of APP and MPP when X = 6: X 0 2 4 6 8 10 12 Y 0 100 250 450 600 700 750 50 and 150 6 and 200 100 and 75 75 and 100arrow_forwardThe Cobb-Douglas production function for a particular product is N(x,y) = 40x0.6.0.4, where x is the number of units of labor and y is the number of units of capital required to produce N(x, y) units of the product. Each unit of labor costs $40 and each unit of capital costs $120. Answer the questions (A) and (B) below. (A) If $300,000 is budgeted for production of the product, determine how that amount should be allocated to maximize production, and find the maximum production. (B) Find the marginal productivity of money in this case, and estimate the increase in production if an additional $50,000 is budgeted for the production of the product. (A) If $300,000 is budgeted for production of the product, determine how that amount should be allocated to maximize production, and find the maximum production. Production will be maximized when using units of labor and units of capital.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education