FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Question

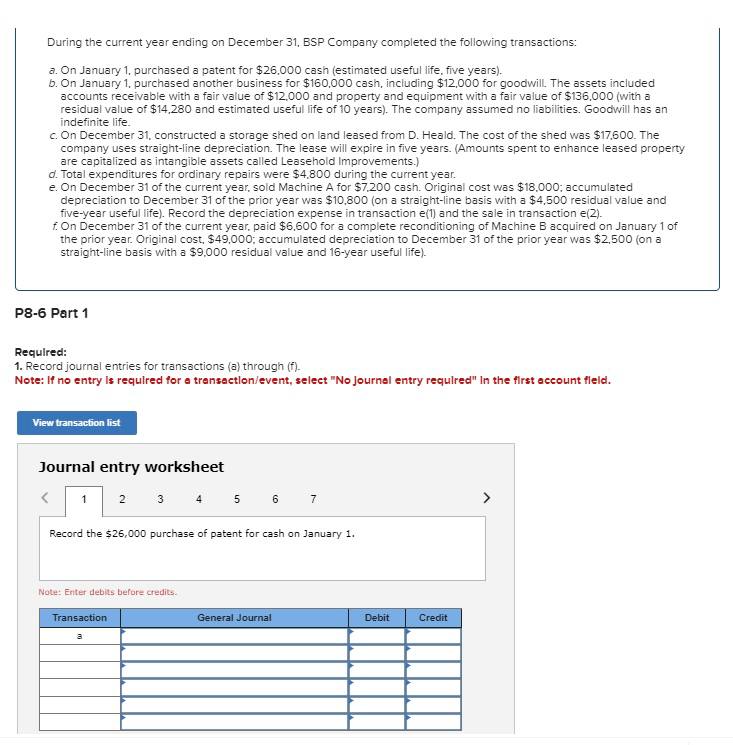

Transcribed Image Text:During the current year ending on December 31, BSP Company completed the following transactions:

a. On January 1, purchased a patent for $26,000 cash (estimated useful life, five years).

b. On January 1, purchased another business for $160,000 cash, including $12,000 for goodwill. The assets included

accounts receivable with a fair value of $12,000 and property and equipment with a fair value of $136,000 (with a

residual value of $14,280 and estimated useful life of 10 years). The company assumed no liabilities. Goodwill has an

indefinite life.

c. On December 31, constructed a storage shed on land leased from D. Heald. The cost of the shed was $17,600. The

company uses straight-line depreciation. The lease will expire in five years. (Amounts spent to enhance leased property

are capitalized as intangible assets called Leasehold Improvements.)

d. Total expenditures for ordinary repairs were $4,800 during the current year.

e. On December 31 of the current year, sold Machine A for $7,200 cash. Original cost was $18,000; accumulated

depreciation to December 31 of the prior year was $10,800 (on a straight-line basis with a $4,500 residual value and

five-year useful life). Record the depreciation expense in transaction e(1) and the sale in transaction e(2).

f. On December 31 of the current year, paid $6,600 for a complete reconditioning of Machine B acquired on January 1 of

the prior year. Original cost, $49,000; accumulated depreciation to December 31 of the prior year was $2,500 (on a

straight-line basis with a $9,000 residual value and 16-year useful life).

P8-6 Part 1

Required:

1. Record journal entries for transactions (a) through (f).

Note: If no entry is required for a transaction/event, select "No journal entry required" In the first account field.

View transaction list

Journal entry worksheet

<

1

234567

Record the $26,000 purchase of patent for cash on January 1.

Note: Enter debits before credits.

Transaction

General Journal

Debit

Credit

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- 1. A patent was purchased on January 2 of Year 1 for $104,000 when the remaining legal life was 16 years. On January 2 of Year 3, Denzel determined that the remaining useful life of the patent was only eight years from the date of its acquisition. 2. On January 1 of Year 3, Denzel Company purchased a second patent for $128,000 cash. At January 1 of Year 3, a total of 6 years of the patent's legal life of 20 years had expired. 3. On June 30 of Year 3, Denzel Company paid a firm $12,800 for a new trademark. Denzel considers the life of the trademark to be indefinite. 4. On November 1 of Year 3, Denzel Company acquired all noncash assets and assumed all liabilities of Lee Company at a cash purchase price of $192,000. Denzel determined that the fair value of the identifiable net assets acquired in the transaction is $187,200. Required a. What is the carrying value of each intangible asset on December 31 of Year 3? Assume no impairment losses were recognized in prior periods. b. What is…arrow_forwardSelect financial information for Logistical Corp. as at December 31, 20X6, follows: Please find the attached image Additional information is as follows: • During the year, Logistical sold equipment for proceeds of $50,000. The equipment had a cost of $80,000 and accumulated depreciation of $35,000.• During the year, a review of Logistical’s goodwill was completed, and it was determined that the asset was impaired and should be written down by $3,000.• Logistical did not purchase any additional investments in the year. Any changes in the fair value of investments have been adjusted through other comprehensive income. These securities are not cash equivalents.• During the year, a new lease was signed for equipment that had a fair market value of $45,000. Depreciation expense for the year totalled $1,000. The new lease was signed in the year, which required a $7,000 payment at the start of the lease.• Logistical elects to classify any interest paid and dividends paid as financing…arrow_forwardDuring the current year, Yost Company disposed of three different assets. On January 1 of the current year, prior to the disposal of the assets, the accounts reflected the following: Asset Machine A Machine B Machine C Estimated Life 8 years 10 years 15 years The machines were disposed of during the current year in the following ways: a. Machine A: Sold on January 1 for $5,000 cash. b. Machine B: Sold on December 31 for $30,500; received cash, $22,500, and an $8,000 interest-bearing (12 percent) note receivable due at the end of 12 months. c. Machine C: On January 1, this machine suffered irreparable damage from an accident. On January 10, a salvage company removed the machine at no cost. Original Cost Residual Value $21,000 120,000 85,000 Accumulated Depreciation (straight line) $15,750 (7 years) 84,800 (8 years) 64,000 (12 years) $3,000 14,000 5,000 equired: Give all journal entries related to the disposal of each machine in the current year. 2. Select the accounting rationale for…arrow_forward

- Loban Company purchased, on January 1 for cash, four cars for $9,000 each and expects that they will be sold in 3 years for $1,500 each. The company uses group depreciation on a straight-line basis. Required: 1. Prepare journal entries to record the acquisition and the first year’s depreciation expense. 2. If one of the cars is sold at the beginning of the second year for $7,000, what journal entry is required?arrow_forwardBensen Company started business by acquiring $26,900 cash from the issue of common stock on January 1, Year 1. The cash acquired was immediately used to purchase equipment for $26,900 that had a $4,500 salvage value and an expected useful life of four years. The equipment was used to produce the following revenue stream (assume that all revenue transactions are for cash). At the beginning of the fifth year, the equipment was sold for $4,950 cash. Bensen uses straight-line depreciation. Revenue Year 1 $ 7,820 Year 2 $ 8,320 Year 3 $ 8,520 Year 4 $ 7,320 Year 5 $ 0 Required Prepare income statements, statements of changes in stockholders' equity, balance sheets, and statements of cash flows for each of the five years. Complete this question by entering your answers in the tabs below. Statement of Income Statement Statement of Changes in Balance Sheet Stockholders Cash Flows Prepare the statements of cash flows for each of the five years. Note: Amounts to be deducted and cash outflows…arrow_forwardDuring the current year, Fortini Company disposed of three different assets. The company's accounts reflected the following on January 1 of the current years, prior to the disposal of the assets: Accumulated Depreciation (straight line) $15,750 (7 years) Original Residual Asset Machine A Machine B Machine C Cost $21,000 50,000 Value $3,000 4,000 75,000 3,000 Estimated Life 8 years 10 years 12 years 36,800 (8 years) 60,000 (10 years) The machines were disposed of in the following ways: a. Machine A: Sold on January 1 of the current year for $5,000 cash. b. Machine B. Sold on April 1 for $10,500; received cash, $2,500, and a note receivable for $8,000, due on March 31 of the following year, plus 6 percent interest. c. Machine C: Suffered irreparable damage from an accident on July 2. On July 10, a salvage company removed the machine at no cost. The machine was insured, and $18,000 cash was collected from the insurance company. Required: 1. Prepare all journal entries related to the…arrow_forward

- Rahularrow_forwardThe draft financial statements of Enjoy Ltd for the year ended 31 December 20X6 are given below. The following additional information is also provided: (i) Plant with an original cost of $800 and accumulated depreciation of $600 was sold for $200. (ii) Interest expense was $350 of which $140 was paid during the period. $130 relating to interest expense of the prior period was also paid during the period. (iii) Investment income included $250 of interest that was received during the period and $250 of interest still to be received. The $250 of interest still to be received is included within other receivables. (iv) Investment income also included $300 of dividend that was received. Statement of Profit and Loss for the year ended 31 December 20X6: Sales 44,870 Cost of sales 31,000 Gross Profit…arrow_forwardTimberly Construction makes a lump-sum purchase of several assets on January 1 at a total cash price of $830,000. The estimated market values of the purchased assets are building, $514,100; land, $329,800; land improvements, $48,500; and four vehicles, $77,600. Compute the first-year depreciation expense on the building using the straight-line method, assuming a 15-year life and a $30,000 salvage value.arrow_forward

- Rakko, Inc. acquired a patent on January 1 for $70,000 cash. The patent was estimated to have a useful life of 14 years with no residual value. Required: Part a. Prepare the journal entry to record the acquisition of the patent on January 1. Part b. Prepare the journal entry to record the annual amortization as of Dec 31.arrow_forwardBluestone Company had three intangible assets at the end of the current year: a. A patent purchased this year from Miller Company on January 1 for a cash cost of $4,000. When purchased, the patent had an estimated life of 10 years. b. A trademark was registered with the federal government for $11,000. Management estimated that the trademark could be worth as much as $260,000 because it has an indefinite life. c. Computer licensing rights were purchased this year on January 1 for $36,000. The rights are expected to have a four-year useful life to the company. Required: 1. Compute the acquisition cost of each intangible asset. 2. Compute the amortization of each intangible for the current year ended December 31. 3. Show how these assets and any related expenses should be reported on the balance sheet and income statement for the current year.arrow_forwardMorey, Inc., has the following plant asset accounts: Land, Buildings, and Equipment, with a separate accumulated depreciation account for each of these except Land. Morey completed the following transactions: Jan 4 Traded in equipment with accumlated depreciation of $64,000 (cost of $134,000) for similar new equipment with a cash cost of $175,000. Recieved a trade-in allowance of $72,000 on the old equipment and paid $103,000 in cash. Jan 29 Sold a building that had a cost of $650,000 and had accumulated depreciationof $140,000 through December 31 of the preceding year. Depreciation is computed on a straight-line basis. The building has a 40-year useful life and a residual value of $220,000. Morey received $125,000 cash and a $379,625 note receivable. Oct 30 Purchased land and a building for a single price of $360,000 cash. An independent appraisal valued the land at $160,800 and the building at $241,200. Dec 31 Recorded depreciation as follows: Equipment has an expected…arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education