FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Topic Video

Question

Transcribed Image Text:CALCULATOR

FULL SCREEN

PRINTER VERSION

( BACK

NEXT

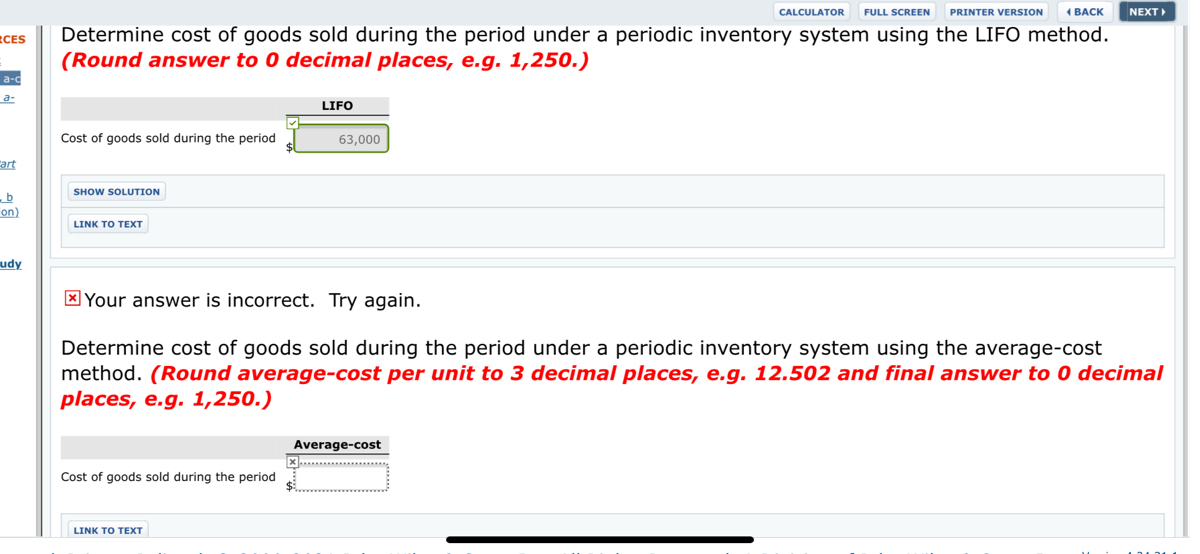

Determine cost of goods sold during the period under a periodic inventory system using the LIFO method.

(Round answer to 0 decimal places, e.g. 1,250.)

ECES

а-с

a-

LIFO

Cost of goods sold during the period

63,000

cart

SHOW SOLUTION

on)

LINK TO TEXT

udy

X Your answer is incorrect. Try again.

Determine cost of goods sold during the period under a periodic inventory system using the average-cost

method. (Round average-cost per unit to 3 decimal places, e.g. 12.502 and final answer to 0 decimal

places, e.g. 1,250.)

Average-cost

Cost of goods sold during the period

LINK TO TEXT

Transcribed Image Text:CALCULATOR

FULL SCREEN

PRINTER VERSION

( BACK

URCES

rk

Do It! Exercise 6-02 a-c

D2 a-c

04 a-

The accounting records of Americo Electronics show the following data.

Beginning inventory 3,000 units at $5

Purchases

8,000 units at $7

(Part

Sales

9,400 units at $10

a2, b

ssion)

M Your answer is correct.

Study

Determine cost of goods sold during the period under a periodic inventory system using the FIFO method.

(Round answer to 0 decimal places, e.g. 1,250.)

FIFO

Cost of goods sold during the period

59,800

SHOW SOLUTION

LINK TOΤΕXΤ

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- petermine the gross profit, cost of merchandise sold, and ending inventory on July 31 using the (a) first-in, first-out, (b) last-in, first-out, and (c) average cost flow methods.arrow_forwardSnow-Tech Inc. sells an Xpert ski that is popular with ski enthusiasts. The following information shows Snow-Tech's purchases and sales of Xpert skis during November: Date Nov. 1 Beginning inventory 5 12 19 22 Explanation 25 Purchases Sales Purchases Sales Purchases Unit Units Cost/Price $296 301 34 23 (40) 42 (48) 33 44 461 306 513 311arrow_forwardOn the basis of the following data, determine the value of the inventory at the lower of cost or market. Assemble the data in the form illustrated in Exhibit 10. Product InventoryQuantity Cost PerUnit Market Value per Unit(Net Realizable Value) Class 1: Model A 16 $162 $169 Model B 32 190 198 Model C 34 152 148 Class 2: Model D 31 298 309 Model E 42 72 78 Question Content Area a. Determine the value of the inventory at the lower of cost or market applied to each item in the inventory. Inventory at the Lower of Cost or Market Product InventoryQuantity Costper Unit Market Valueper Unit(Net Realizable Value) Cost Market Lower of Cost or Market Model A fill in the blank 1b67cb01c017023_1 $fill in the blank 1b67cb01c017023_2 $fill in the blank 1b67cb01c017023_3 $fill in the blank 1b67cb01c017023_4 $fill in the blank 1b67cb01c017023_5 $fill in…arrow_forward

- James's Televisions produces television sets in three categories: portable, midsize, and flat-screen. On January 1, 2025, James adopted dollar-value LIFO and decided to use a single inventory pool. The company's January 1 inventory consists of: Category Portable Midsize Flat-screen Category Portable Midsize Quantity Cost per Unit $100 Flat-screen 3,000 4,000 1,500 8,500 Quantity Purchased 7,500 During 2025, the company had the following purchases and sales. 10,000 5,000 250 22,500 400 Cost per Unit $110 300 Total Cost 500 $300,000 1,000,000 600,000 $1,900,000 Quantity Sold 7,000 12,000 3,000 22,000 Selling Price per Unit $150 400 600arrow_forwardThe cost of goods sold (Using the FIFO method) $.__________________________ The of cost of the ending Inventory (using the LIFO method) $____________________ The cost of Goods sold (Using the LIFO method) $_______________________________arrow_forwardSubject: accountingarrow_forward

- The following information is taken from a company’s records. Costper Unit Market valueper Unit Inventory Item 1 (10 units) $39 $38 Inventory Item 2 (22 units) 19 19 Inventory Item 3 (12 units) 9 11 Applying the lower-of-cost-or-market approach, what is the correct value that should be reported on the balance sheet for the inventory? $fill in the blank 1arrow_forwardGlasgow Corporation has the following inventory transactions during the year. Unit Number of Units 53 133 Cost $ 45 47 Total Cost $ 2,385 6,251 10,150 5,763 Date Transaction Jan. 1 Beginning inventory Purchase Purchase Purchase Apr. 7 Jul.16 203 50 Oct. 6 113 51 502 $24,549 For the entire year, the company sells 433 units of inventory for $63 each.arrow_forwardWildhorse Co. is a retailer operating in Calgary, Alberta. Wildhorse uses the perpetual inventory method. Assume that there are no credit transactions; all amounts are settled in cash. You are provided with the following information for Wildhorse for the month of January 2022. Date Description Quantity Unit Cost or Selling Price Dec. 31 Ending inventory 150 $ 20 Jan. 2 Purchase 100 21 Jan. 6 Sale 180 42 Jan. 9 Purchase 70 25 Jan. 10 Sale 60 42 Jan. 23 Purchase 112 26 Jan. 30 Sale 128 49arrow_forward

- Assuming that all net sales figures are at retail and all cost of goods sold figures are at cost, calculate the average inventory (in $) and inventory turnover for the following. If the actual turnover is less than the published rate, calculate the target average inventory (in $) necessary to come up to industry standards. If the actual turnover is greater than the published rate, enter "above" for target average inventory. Round inventories to the nearest dollar and inventory turnovers to the nearest tenth. Net Sales $4,560,000 Cost of Goods Sold Beginning Ending Inventory Inventory $858,000 $654,300 Average Inventory $ Inventory Published Turnover Rate 8.2 Target Average Inventoryarrow_forward3. Calculate the cost of goods sold dollar value for A74 Company for the sale on March 11, considering the following transactions under three different cost allocation methods and using perpetual inventory updating. Provide calculations for (a) first-in, first-out (FIFO); (b) last-in, first-out (LIFO); and (c) weighted average (AVG). Number of Units Unit Cost Beginning inventory Mar. 1 Purchased Mar. 8 Sold Mar. 11 for $120 per unit 110 $87 140 89 95arrow_forwardLower-of-cost-or-market method On the basis of the following data, determine the value of the inventory at the lower-of-cost-or-market by applying lower-of-cost-or-market to each inventory item, as shown in Exhibit 10. Commodity InventoryQuantity Cost perUnit Market Value per Unit(Net Realizable Value) JFW1 78 $58 $55 SAW9 148 28 33arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education