Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

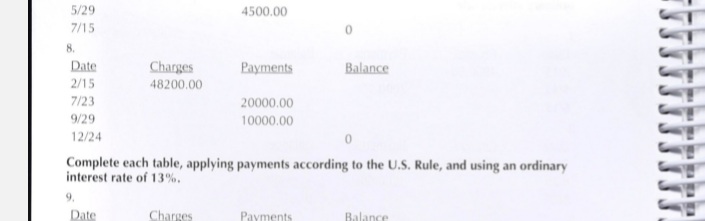

#8. Complete the table, applying payments according to the U.S. rule, and using an ordinary interest rate of 13%

Transcribed Image Text:5/29

4500.00

7/15

8.

Date

Charges

Payments

Balance

2/15

48200.00

7/23

20000.00

9/29

10000.00

12/24

Complete each table, applying payments according to the U.S. Rule, and using an ordinary

interest rate of 13%.

9.

Date

Charges

Payments

Balance

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- A bank in Mississauga has a buying rate of ¥1 = C$0.01275. If the exchange rate is ¥1 = C$0.01315, calculate the rate of commission that the bank charges to buy currencies. Round to two decimal placesarrow_forwardThe $/£ spot rate is $1.60/£1. The UK interest rate is 4% and the US interest rate is 9%. Calculate the one year forward rate using the covered interest parity formula. State if the pound is at a forward discount or at a forward premium, and why.arrow_forwardSuppose that the U.S. interest rate on one year Treasury notes was 4.5%. We will use this as the annual interest rate in the U.S. And suppose that the interest rate on the one-year German Treasury note was 4.1%. The spot rate is 1.0162 EUR/USD.. And the 3-month forward rate is 1.0188 Eur/USD. Is there an opportunity for covered interest arbitrage? If so, what would be the total profit if we borrowed $20 million for 3 months? A. YES- $27,395.21 would be the profit B. YES- $29,385.41 would be the profit C. YES- $31,695.53 would be the profit D. YES- $33,875.42 would be the profit E. NO- there is no opportunity for a profitarrow_forward

- Please use this information to answer the question below: A US firm's expected Accounts Receivables in Euro Zone due in 1 year Current Spot Rate (SR) for EUR Annual interest rate in US (Rh) Annual interest rate in Euro Zone (RF) EUR 15,000,000 USD 1.25 5% O USD 17,578,125 OEUR 13,392,857 EUR 18,750,000 USD 16,741,071 12% If the firm uses money market hedge, one year from now, their accounts receivables will fetch them:arrow_forwardSuppose the interest rate in Japan is 2% p. a. and the interest rate in the US is 3.6% p. a. What is the (approximate) forward premium for the yen?arrow_forwardLet the inflation rate in Belize be 3.3%. At the same time, the inflation rate in the U.S. is 2.9%. According to PPP, the Belize dollar (BBD) should ___________ by _________%. a . appreciate; 0.387% b . depreciate; 1.387% c . depreciate; 0.387% d . appreciate; 1.387%arrow_forward

- Assume the following information: Spot rate of U.S. dollar Quoted Price AUD1.2500/USD 180-day forward rate of U.S. dollar 180-day Australian interest rate (a periodic rate) 180-day U.S. interest rate (a periodic rate) AUD1.2800/USD 4.75% 3.10% A. What USD-denominated percent rate of return can a US investor earn if they attempt covered interest arbitrage? (to two decimal places like 6.54%) B. What AUD-denominated percent rate of return can an Australian investor earn if they attempt covered interest arbitrage? (to two decimal places like 6.54%) C. Given this information, who has a covered interest arbitrage opportunity? Answer either "Australian investors" or "U.S. investors". D. What changes in the 2 quoted prices above would likely occur to eliminate any further possibilities of covered interest arbitrage? (answer with just or 1) Spot rate of U.S. dollar 180-day forward rate of U.S. dollararrow_forwardFor the below questions use these rates that your bank has quoted you: EUR/USD: 1.0175 – 1.0180 GBP/USD: 1.2065 – 1.2070 USD/CAD: 1.2930 – 1.2935 USD/JPY: 134.85 – 134.90 AUD/USD: .6905 - .6910 Calculate the following crosses: EUR/GBP EUR/JPY AUD/JPY GBP/CAD GBP/JPY CAD/JPYarrow_forwardFrom the following data provided, ascertain what would be the exchange rates that the Bank would quote for an FDI transaction amounting to USD 2 Mn for value cash basis, assuming a margin of 3 paise where., Spot USD/INR = 75.0900/75.1000 ., Cash/Spot : 4/5 paise. Arrive at the exchange rate up to 4 decimal places. Adhere to the steps involved in calculation.arrow_forward

- Question II: The premium of a 100-strike yen-denominated put on the euro is 8.763. The current exchange rate is 95 /c. What is the strike of the corresponding curo-denominated yen call, and what is its premium?arrow_forward4) Suppose the Canadian dollar (CAD) is quoted at 1.3240 - 55 CAD/USD and the Euro is quoted at 0.8220 - 55 EUR/USD. What is the direct quote for the Canadian dollar in France?arrow_forward) In another case are these quotes: Spot rate €1.2562/£; 1 month forward €1.2662/£. Which of the two currencies is trading at forward premium?arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education