ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

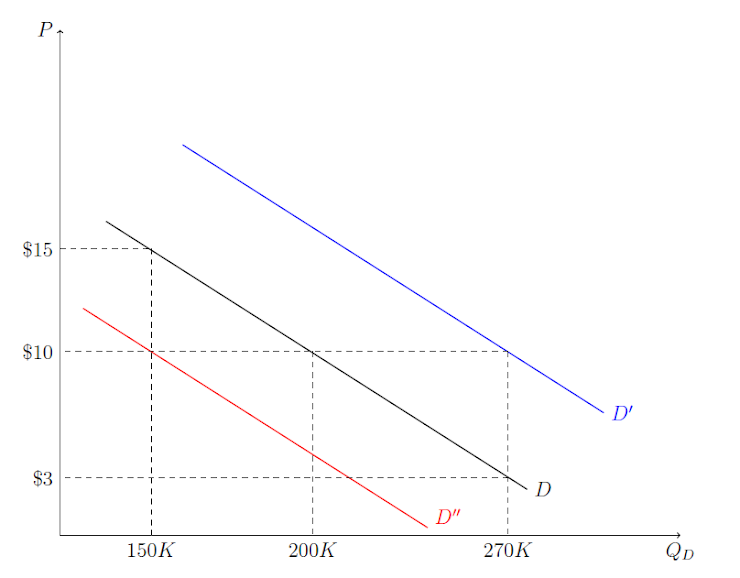

Consider the demand for shrimp shown in Figure 2. Suppose the current demand for shrimp is D (in black), the current price of a pound of shrimp is $10, and the current quantity demand for shrimp is 200K. Which of the following correctly describes a decrease in the demand for shrimp, assuming the price of a pound of shrimp remains at $10?

A) The demand curve for shrimp shifts right from D (black) to D' (blue), and the quantity demand for shrimp decreases from 200K pounds to 150K pounds.

B) The demand curve for shrimp shifts left from D (black) to D'' (red), and the quantity demand for shrimp decreases from 200K pounds to 150K pounds.

C) The demand curve for shrimp shifts right from D (black) to D' (blue), and the quantity demand for shrimp increases from 200K pounds to 270K pounds.

D) The demand curve for shrimp shifts left from D (black) to D'' (red), and the quantity demand for shrimp increases from 200K pounds to 270K pounds.

Transcribed Image Text:$15

$10

D'

$3

D

D"

150K

200K

270K

QD

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Find the equilibrium price and quantity for a product that has the following supply and demand curves, where p is the price in 100's of dollars and q is quantities in 1,000's of units demand: 1/3q + 1/3p - 4=0 Supply: q-p-2=0 If the product is currently priced at $400, what is the quantity supplied and the quantity demanded? Is there a surplus (More supplied than demanded) or a shortage (More demanded than supplied)arrow_forwardQuestion 1 Consider a rice farmer planting two (2) types of rice, white and brown rice, concurrently in his rice field using the same resources and technology and harvesting them at the same time. Given that consumers like to mix both white and brown rice in their daily consumption, explain the effect on the white rice market when the price of brown rice increases. Support your answers with suitable white rice market diagrams. Consider a farmer that produces both white and brown rice. It is discovered that the demand for brown rice is relatively more inelastic compared to the demand for white rice. Initially the price of both white and brown rice is the same and the farmer produces the same quantity of white and brown rice. Now there is an improvement in agricultural technologies that affect both white and brown rice equally. Employ the demand and supply model to compare and contrast the effects on the equilibrium price and quantity of both white and brown rice…arrow_forwardSuppose the demand for organic bananas is given by the following equation: Qd = 10 - 1P where Qd is the quantity demanded per week of organic bananas, and P is the price of organic bananas. Suppose further that the supply of organic bananas is: Qs = 3 + 2P where Qs is the quantity supplied per week of organic bananas. What is the equilibrium market quantity of organic bananas? (Round your answer to 2 decimal places.)arrow_forward

- Consider two markets: the market for waffles and the market for pancakes. The initial equilibrium for both markets is the same, the equilibrium price is $6.50, and the equilibrium quantity is 35.0. When the price is $9.75, the quantity supplied of waffles is 57.0 and the quantity supplied of pancakes is 101.0. For simplicity of analysis, the demand for both goods is the same. Using the midpoint formula, calculate the elasticity of supply for pancakes. Please round to two decimal places. Supply in the market for waffles isarrow_forwardBelow are the supply and demand schedules for a video game. Price $200 $180 $160 $140 $120 $110 $100 $90 $80 $60 Quantity Demanded 10 15 20 25 30 35 40 45 50 55 Quantity Supplied 100 90 80 70 60 50 40 30 20 10 a) What is the equilibrium price? $ b) What is the equilibrium quantity? Assume that this video game receives a poor rating and consumers decide to purchase 45 less at each price. c) What is the new equilibrium price? $ d) What is the new equilibrium quantity? 100 40 units unitsarrow_forwardConsider the demand for soap shown in Figure 1 above. What is quantity demand for soap if the price of a pound of soap is $10? A) 210 pounds B) 248 pounds C) 286 pounds D) 305 poundsarrow_forward

- Solve the attachmentarrow_forwardUsing the supply and demand functions below, derive the demand and supply curves if Y=$55,000 and pc=$9. What is the equilibrium price and quantity of coffee? Part 2 The demand function for coffee is Q=8.5−p+0.01Y, where Q is the quantity of coffee in millions of pounds per year, p is the price of coffee in dollars per pound, and Y is the average annual household income in high-income countries in thousands of dollars. The coffee supply function is Q=9.6+0.5p−0.2pc, where pc is the price of cocoa in dollars per pound.arrow_forwardThe weekly demand for wine in the United States is described by the following equation: Qd = 45,000,000 - 1,500,000P where Qd is the weekly quatity demanded in bottles and P is the price per bottle in dollars. The weekly supply of wine in the United States is described by the following equation: Qs = -5,000,000 + 1,000,000P where Qs is the weekly quantity supplied in bottles and P is the price per bottle in dollars. a. What is the equilibrium price and quantity for wine in the US? Intense lobbying efforts result in the United States government establishing a $5 per bottle excise tax by wine producers. b. What would be the new equilibirum price and quantity after the imposition of the per bottle excise tax? c. Determine the total amount of the consumer surplus assuming the market for wine is in equilibrium after the imposition of the excise tax.arrow_forward

- By providing an example, explain three factors that might shift the demand curve for a product inward (to left).arrow_forward6. Individual and market demand Suppose that Dmitri and Frances are the only consumers of pizza slices in a particular market. The following table shows their weekly demand schedules: Price Dmitri's Quantity Demanded Frances's Quantity Demanded (Dollars per slice) (Slices) (Slices) 1 8. 12 5 8 3 3 6. 4 1 4 5arrow_forwardConsider the supply and demand for electric cars. If the materials used to make specifically electric car batteries become significantly more expensive at the same time that consumer income drastically increases, what will happen to the price and quantity demanded of electric cars?arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education