Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

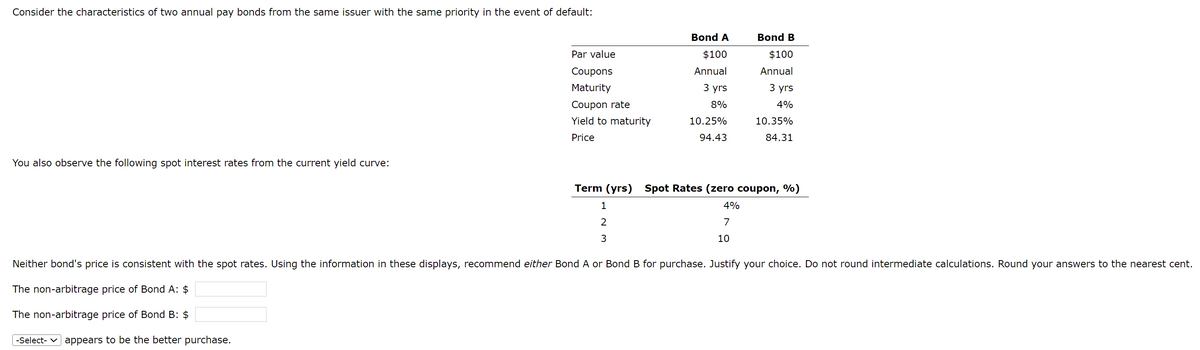

Transcribed Image Text:Consider the characteristics of two annual pay bonds from the same issuer with the same priority in the event of default:

You also observe the following spot interest rates from the current yield curve:

Par value

Coupons

Maturity

Coupon rate

Yield to maturity

Price

Bond A

$100

Annual

3 yrs

8%

10.25%

94.43

1

2

3

Bond B

$100

Annual

3 yrs

4%

10.35%

84.31

Term (yrs) Spot Rates (zero coupon, %)

4%

7

10

Neither bond's price is consistent with the spot rates. Using the information in these displays, recommend either Bond A or Bond B for purchase. Justify your choice. Do not round intermediate calculations. Round your answers to the nearest cent.

The non-arbitrage price of Bond A: $

The non-arbitrage price of Bond B: $

-Select- ✓ appears to be the better purchase.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 3 steps with 8 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- The following is a list of prices for zero-coupon bonds of various maturities. Maturity (years) Price of Bond 1 $ 953.40 2 903.47 3 852.62 4 787.66 Required: Calculate the yield to maturity for a bond with a maturity of (i) one year; (ii) two years; (iii) three years; (iv) four years. Assume annual coupon payments. Calculate the forward rate for (i) the second year; (ii) the third year; (iii) the fourth year. Assume annual coupon payments.arrow_forwardThis question has TWO parts. Please be sure to scroll down and make sure you answer both parts. Which of the following bonds will be most sensitive to a change in interest rates if all bonds have the same initial yield to maturity? O A. a 10-year bond with a $1,000 face value whose coupon rate is 4.7% APR paid semiannually OB. a 20-year bond with a $1,000 face value whose coupon rate is 8.1% APR paid semiannually OC. a 20-year bond with a $1,000 face value whose coupon rate is 4.7% APR paid semiannually OD. a 10-year bond with a $1,000 face value whose coupon rate is 8.1% APR paid semiannually ... A measurement of the sensitivity of a bond's price to changes in interest rates is known as: (choose the most appropriate answer below) OA. Duration OB. Yield to Maturity (YTM) OC. Repayment Risk OD. Credit Riskarrow_forwardAssuming that the bond with the coupon you computed in b.4 were issued today, show to what the market price of that bond in b.4 would change if the bond yield to maturity fell by 2% shortly after it was issued at par value (with the change in the yield to maturity after issue occurring due to a decline in yields on 30-year T-bonds and/or a reduction in the company’s default risk) semi-annual payments and sells for its par value/principal amount of $1000 per bond? Market Rate = 4.97%-2%arrow_forward

- Explain why are the bond prices for A and B different or the same? Explain your answer clearly.arrow_forwardThe yield on a zero-coupon bond of maturity Tis equal to: the return on the bond each period, if the bond is held until maturity the expected return on the zero-coupon bond the forward rate for time T-1 the forward rate for time T the spot rate of interestarrow_forwardPlease do not give image formatarrow_forward

- Compute yield-to-maturity for the following zero-coupon bonds: 1-year zero-coupon bond, traded currently at 980 dollars 2-years zero-coupon bond, traded currently at 920 dollars 3-years zero-coupon bond, traded currently at 840 dollars Assume that all 3 bonds have the same nominal: 1000 dollars. Using YTMs calculated plot the yield curve.arrow_forwardSuppose you observe the following zero - coupon bond prices per $1 of maturity payment: 0.96154 (1-year), 0.91573 (2-year), 0.87630(3-year), 0.82270 (4- year), 0.77611 (5-year). What is the par coupon rate for the 4-year bond? Question 3 options: 3.999834% 4.488965% 4.492350 % 4.957679 % 5.144082%arrow_forwardThe following is a list of prices for zero-coupon bonds of various maturities. Maturity (years) 1 2 3 4 Price of Bond $ 980.90 914.97 843.12 771.76 Required: a. Calculate the yield to maturity for a bond with a maturity of (i) one year; (ii) two years; (iii) three years; (iv) four years. Assume annual coupon payments. b. Calculate the forward rate for (i) the second year; (ii) the third year; (iii) the fourth year. Assume annual coupon payments. Complete this question by entering your answers in the tabs below. Required A Required B Calculate the yield to maturity for a bond with a maturity of (i) one year; (ii) two years; (iii) three years; (iv) four years. Assume annual coupon payments. Note: Do not round intermediate calculations. Round your answers to 2 decimal places. Maturity (Years) Price of Bond YTM 1 $ 980.90 % 2 $ 914.97 % 3 $ 843.12 %arrow_forward

- Please answer 6D.arrow_forwardConsider the following: Price Yield to maturity Periods to maturity Modified duration Fixed-rate Bond Fixed-rate Note 107.18 5.00% 18 6.9848 100.00 5.00% 8 3.5851 a. For an increase in interest rates of 100 basis points, determine the change in value for the fixed-rate note. Show your work. b. For an increase in interest rates of 100 basis points, determine the change in value for the fixed-rate bond. Show your work. c. Which of the two fixed-rate securities are more sensitive to increases interest rates? Why? d. What would be the most appropriate course of action to take given interest rates are expected to rise? Explain carefully.arrow_forwardPrepare a duration table for a zero-coupon bond using the following assumptions: a. $100,000 par value b. 10-year maturity c. Discount Rate of 12%arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education