Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

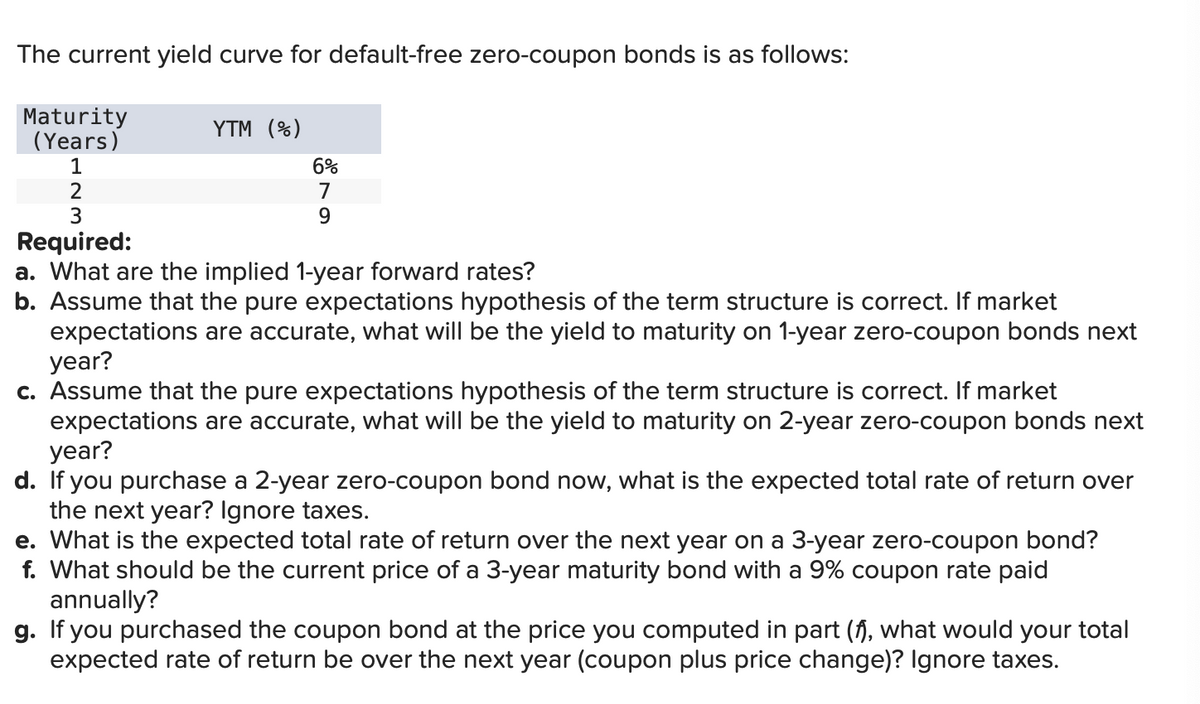

Transcribed Image Text:The current yield curve for default-free zero-coupon bonds is as follows:

Maturity

(Years)

1

YTM (%)

6%

7

9

2

3

Required:

a. What are the implied 1-year forward rates?

b. Assume that the pure expectations hypothesis of the term structure is correct. If market

expectations are accurate, what will be the yield to maturity on 1-year zero-coupon bonds next

year?

c. Assume that the pure expectations hypothesis of the term structure is correct. If market

expectations are accurate, what will be the yield to maturity on 2-year zero-coupon bonds next

year?

d. If you purchase a 2-year zero-coupon bond now, what is the expected total rate of return over

the next year? Ignore taxes.

e. What is the expected total rate of return over the next year on a 3-year zero-coupon bond?

f. What should be the current price of a 3-year maturity bond with a 9% coupon rate paid

annually?

g. If you purchased the coupon bond at the price you computed in part (f), what would your total

expected rate of return be over the next year (coupon plus price change)? Ignore taxes.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps

Knowledge Booster

Similar questions

- (a) You hold a consol that pays a coupon C in perpetuity. The current interest rate is i, and the average expectation in the market is that this will remainunchanged. What will be the price of the consol today? (b) In the next period however, the interest rate changes unexpectedly to i'. What is the new price of the bond? If the bond is sold at the beginning of that next period, what is the yield from the consol? Does the yield increase or decrease if i'> i? (c) Suppose alternatively that the market expects that the interest rate will change to i' after the initial period. What is the initial value of the consol, and whatis the yield from selling it after one period?arrow_forwardAssume the real risk-free is 1% and the average annual expected inflation rate is 4%. The DRP and LP for bond A are each 3%, and the applicable MRP is 3%. What is Bond A's interest rate?arrow_forwardSuppose you are considering two possible investment opportunities: a 12-year Treasury bond and a 7-year, A-rated corporate bond. The current real risk-free rate is 3%, and inflation is expected to be 2% for the next 2 years, 3% for the following 4 years, and 4% thereafter. The maturity risk premium is estimated by this formula: MRP = 0.02(t - 1)%. The liquidity premium (LP) for the corporate bond is estimated to be 0.3%. You may determine the default risk premium (DRP), given the company's bond rating, from the following table. Remember to subtract the bond's LP from the corporate spread given in the table to arrive at the bond's DRP. Corporate Bond Yield Rate Spread = DRP + LP U.S. Treasury 0.83 % — AAA corporate 1.03 0.20 % AA corporate 1.39 0.56 A corporate 1.79 0.96 What yield would you predict for each of these two investments? Round your answers to three decimal places. 12-year Treasury yield: fill in the blank _ % 7-year Corporate yield: fill…arrow_forward

- Suppose we observe the following rates: 1R1 = 6.7, 1R2 = 7.4, and E(2r1) = 6.7. If the liquidity premium theory of the term structure of interest rates holds, what is the liquidity premium for year 2? Please step by step.arrow_forward1) If a speculator expects interest rates to increase, should they go long or short on a futures contract for a 10-year US treasury bond? 2) True or False: The yield curve provides a forecast of economic growth.arrow_forward1. If the term structure is upward sloping and the risk premium is negative, we know with certainty which of the following? i) Investors expect interest rates to rise ii) The two year rate is above the one year rate iii) The forward rate will be above the spot or current rate iv) The expected return from a two year bond is above the expected return from rolling over in two one-year bonds a) I and II only b) I, II, and III only c) II and III only d) I, III, and IV onlyarrow_forward

- Conceptually good plsarrow_forwardCoupon payments are fixed, but the percentage return that investors receive varies based on market conditions. This percentage return is referred to as the bond’s yield. Q1. Yield to maturity (YTM) is the rate of return expected from a bond held until its maturity date. However, the YTM equals the expected rate of return under certain assumptions. Which of the following is one of those assumptions? a. The bond is callable. b. The probability of default is zero. Consider the case of RTE Inc: Q2. RTE Inc. has 9% annual coupon bonds that are callable and have 18 years left until maturity. The bonds have a par value of $1,000, and their current market price is $1,130.35. However, RTE Inc. may call the bonds in eight years at a call price of $1,060. What are the YTM and the yield to call (YTC) on RTE Inc.’s bonds? Value YTM ? YTC ? Q3. If interest rates are expected to remain constant, what is the best estimate of the remaining life left for RTE Inc.’s bonds? a. 8 years b. 10…arrow_forwardYou observe the following yield curve for Treasury securities: Maturity 1 Year 2 Years 3 Years 4 Years 5 Years Assume that the pure expectations hypothesis holds. What does the market expect will be the yield on 4-year securities, 1 year from today? O 6.45% O 6.30% O 6.15% O 6.00% Yield 2.40% 3.40% 4.00% 4.10% 5.40% 5.85%arrow_forward

- Suppose the interest rate on a 1-year T-bond is 2.60% and that on a 2-year T-bond is 4.50%. Assume that the pure expectations theory is NOT valid, and the MRP is zero for a 1-year T-bond but 0.30% for a 2-year bond. What is the equilibrium market forecast for 1-year rates 1 year from now? a. 4.7333% b. 5.1110% c. 5.2676% d. 5.5463% e. 5.8250%. Only typing answer Please explain step by steparrow_forward. Bond yields Coupon payments are fixed, but the percentage return that investors receive varies based on market conditions. This percentage return is referred to as the bond’s yield. Yield to maturity (YTM) is the rate of return expected from a bond held until its maturity date. However, the YTM equals the expected rate of return under certain assumptions. Which of the following is one of those assumptions? The bond is callable. The probability of default is zero. Consider the case of Demed Inc.: Demed Inc. has 9% annual coupon bonds that are callable and have 18 years left until maturity. The bonds have a par value of $1,000, and their current market price is $1,160.35. However, Demed Inc. may call the bonds in eight years at a call price of $1,060. What are the YTM and the yield to call (YTC) on Demed Inc.’s bonds?arrow_forwardb. Suppose you are considering two possible investment opportunities: a 12-year Treasury bond and a 7-year, AA-rated corporate band. The current real risk-free rate is 5%, and inflation is expected to be 2% for the next 2 years, 3% for the following 4 years, and 4% thereafter. The maturity risk premium is estimated by this formula: MRP = 0.03 (t-1) %. The liquidity premium (LP) for the corporate bond is estimated to be 0.2%. You may determine the default risk premium (DRP), given the company's bond rating, from the following table. Remember to subtract the bond's LP from the corporate spread given in the table to arrive at the bond's DRP. Rate 0.83% 1.03 1.35 1.73 Corporate Bond Yield Spread = DRP + LP U.S. Treasury AAA corporate 0.20% AA corporate 0.52 A corporate 0.90 What yield would you predict for each of these two investments? Round your answers to three decimal places, 12-year Treasury yield: 7-year Corporate yield: % %arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education