ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

(a) Why does the labour demand curve slope downwards?

(b) A garment factory’s production function is provided in the table.The gross profit per unit (difference between selling price and material cost, but not including the cost of labour) is $100.

| # Workers | Output |

| 1 | 20 |

| 2 | 36 |

| 3 | 48 |

| 4 | 56 |

| 5 | 60 |

| 6 | 62 |

(i) If the wage rate is $1,000 a week, how many workers should the factory hire?

(ii) If a surge in popularity for the factory’s brand allows them to raise the product price such that the gross profit rises to $150, how many workers will the factory hire now?

(iii) Calculate the number of garments produced in each of the two cases above.

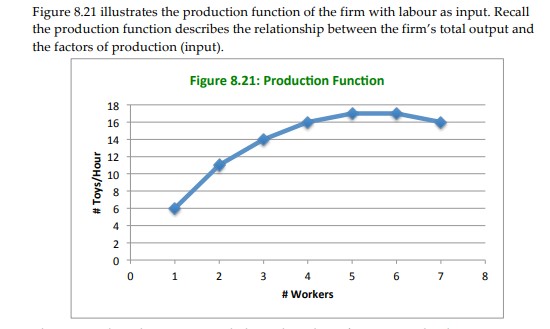

Transcribed Image Text:Figure 8.21 illustrates the production function of the firm with labour as input. Recall

the production function describes the relationship between the firm's total output and

the factors of production (input).

Figure 8.21: Production Function

18

16

14

12

10

8

6.

4

2

1

3

6.

8.

# Workers

# Toys/Hour

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps with 1 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Why does the marginal product of labor start to decrease after a certain number of workers are hired? What makes the difference? a) The variable input continues to increase while the fixed input is fixed. b) Both the variable and the fixed inputs are increasing at the same rate. is it a or b?arrow_forwardThe firm’s production data is given in the table below. What is the marginal product for the 4th worker? Number of workers Quantity of Computers Produced (Total Product) 0 0 1 15 2 28 3 38 4 46 5 52arrow_forwardThe market for drones is perfectly competitive. Labor is the only variable input. The fixed cost is $500. Based on the information in the table below, what is the Marginal Product of Labour when Q=300? Enter a number only, drop the $ sign. Wage rate =$100 per unit of Labour Quantity Quantity of of Labour Output 8 44 15 213 21 300 43 433arrow_forward

- 9. Assume the production function of a farmer who keeps a poultry is q = f(1) = 100L05, where Lis labor (i.e., the number of people working on the farm) and q is output (number of birds). If the wage rate is w = 2 and the price per bird is p = 3, how many people should he employ? Explain your answer.arrow_forward1. Suppose a short-run production function is described as Q40L 0.04L2 where L is the number of labors used each hour.arrow_forwardIf the marginal product of labor is 50 per day, and if the market is $4.50, calculate the marginal revenue product.arrow_forward

- An economic downturn has caused the labor demand to decrease from DO to D1. In the short-run what will be the new wage and level of employment? Wage Rate 40 35 30 ($) 25 20 20 15 10 DO 5 D1 0 5 10 15 20 25 30 35 40 Quantity of Labor (Q)arrow_forwardA firm in a competitive market should hire workers up to the point where the value of the marginal product of labor = a. the wage b. total revenue c. total cost d. total profitarrow_forwardHand written solutions are strictly prohibitedarrow_forward

- Describe the construction of the firm’s demand curve for labour in the short run.Describe the relationship between the firm's demand curve for labour in the short-run andthe market demand curve for labour in the short-run. In particular, is one curve likely to bemore or less elastic than the other? Explain your answer.arrow_forwardIn the short run, a tool manufacturer has a fixed amount of capital. Labor is a variable input. The cost and output structure that the firm faces is depicted in the table below. Assume the product price is $4. Calculate the marginal revenue product and the marginal resource cost, and then complete the table. Instructions: Enter your answers as whole numbers. Quantity of Labor Marginal Product Marginal Revenue Hourly Wage Rate ($) Marginal Resource Total Product Total Labor Product ($) Cost ($) (Labor) Cost ($) 10 400 5 50 es 11 420 20 8. 88 12 438 18 11 132 13 454 16 14 182 14 468 14 17 238 15 480 12 20 300 The equilibrium wage rate ($) = The equilibrium level of labor use = workersarrow_forwardI7arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education