FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

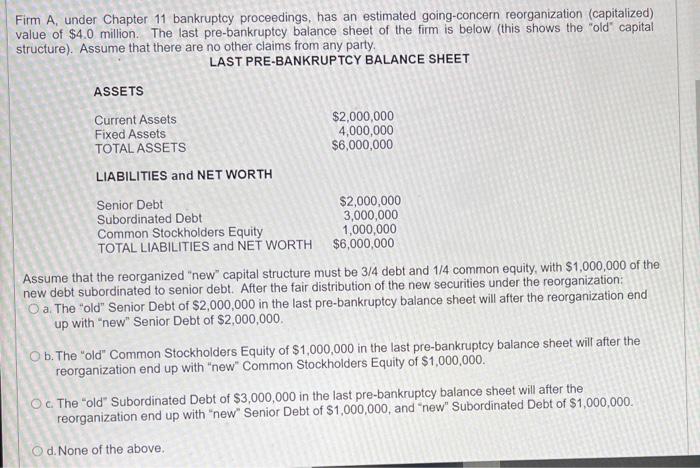

Transcribed Image Text:Firm A, under Chapter 11 bankruptcy proceedings, has an estimated going-concern reorganization (capitalized)

value of $4.0 million. The last pre-bankruptcy balance sheet of the firm is below (this shows the "old" capital

structure). Assume that there are no other claims from any party.

LAST PRE-BANKRUPTCY BALANCE SHEET

ASSETS

Current Assets

Fixed Assets

TOTAL ASSETS

$2,000,000

4,000,000

$6,000,000

LIABILITIES and NET WORTH

Senior Debt

Subordinated Debt

Common Stockholders Equity

TOTAL LIABILITIES and NET WORTH $6,000,000

$2,000,000

3,000,000

1,000,000

Assume that the reorganized "new" capital structure must be 3/4 debt and 1/4 common equity, with $1,000,000 of the

new debt subordinated to senior debt. After the fair distribution of the new securities under the reorganization:

O a. The "old" Senior Debt of $2,000,000 in the last pre-bankruptcy balance sheet will after the reorganization end

up with "new" Senior Debt of $2,000,000.

O b. The "old" Common Stockholders Equity of $1,000,000 in the last pre-bankruptcy balance sheet will after the

reorganization end up with "new" Common Stockholders Equity of $1,000,000.

OC The "old" Subordinated Debt of $3,000,000 in the last pre-bankruptcy balance sheet will after the

reorganization end up with "new" Senior Debt of $1,000,000, and "new" Subordinated Debt of S$1,000,000.

O d. None of the above.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- 1. Computational. On January 1, 20x1, ABC purchased bonds with face amount of P5,000,000. The entity paid P4,700,000 plus transaction cost of P42,130 for the bond investment. The business model of the entity in managing the financial asset is to collect contractual cash flows that are solely payment of principal and interest and also to sell the bonds the open market. The bonds mature on December 31, 20x3 and pays 6% interest annually on December 31 each year with 8% effective interest rate (after incorporating the transaction cost on initial recognition). The bonds are quoted at 106 and 108 on December 31, 20x1 and December 31, 20x2. The bonds are sold at 103 on July 1, 20x3, excluding accrued interest. Use 4-decimal present value factor. For the year ended December 31, 20x3, how much is the total impact to profit or loss as a result of the business model of ABC in holding this investment? (sample answer: 2,350,450.55)arrow_forwardPROBLEM: The creditors of the RR Corp. agreed to a liquidation based on the statement of affairs, suggested that unsecured creditors, without priority would receive approximately P.60 on the peso. The unsecured creditors are interested in determining whether the preliminary estimate still seems appropriate. The trustee was originally assigned noncash asset for P1,480,000 and creditor claims as follows: Fully secured P670,000 Partially secured P400,000 Unsecured with priority P200,000 Unsecured without priority P320,000 Assets with book value of P45,000 and unsecured liabilities, without priority, of P35,000 were subsequently discovered. Assets with a total book value of P740,000 were sold for P715,000 net. Fully secured liabilities of P410,000 and partially secured liabilities of P280,000 were paid. Remaining liquidation expenses were estimated to be P30,000. Assume the remaining noncash assets have an estimated net realizable value as follows: Assets traceable to…arrow_forwardIn business combination, the fair value of combinee bonds payable was $ 120,000 and the carrying amount of bonds payable was $ 100,000. The journal entry to allocate liquidated company to identifiable assets and liabilities with remainder to goodwill includes: а. Credit to premium on bonds payable $ 20,000. b. Debit to discount on bonds payable $ 20,000. C. Credit to bonds payable $ 120,000. d. Debit to premium on bonds payable $ 20,000arrow_forward

- On 1/1/2019, Allie Company issued bonds payable of $500,000 at 8%. It was sold at $464,000 with effective interest rate of 9%. On 1/1/2020, Choco purchased all of Allie's bond for $532,000 cash with effective interest at 7% and Allie's bonds payable has been effectively retired. 3) Compute the consolidated gain or loss on a consolidated income statement for at the end of 2020arrow_forwardAt December 31, 2020, the available-for-sale debt portfolio for Windsor, Inc. is as follows. Security Cost Fair Value UnrealizedGain (Loss) A $27,125 $23,250 $(3,875 ) B 19,375 21,700 2,325 C 35,650 39,525 3,875 Total $82,150 $84,475 2,325 Previous fair value adjustment balance—Dr. 620 Fair value adjustment—Dr. $1,705 On January 20, 2021, Windsor, Inc. sold security A for $23,405. The sale proceeds are net of brokerage fees. 1). Prepare the adjusting entry at December 31, 2020, to report the portfolio at fair value. 2). Show the balance sheet presentation of the investment-related accounts at December 31, 2020arrow_forwardYear 2 and 3 for Fair Value at the end of the year are still incorrect and I do not understand why?arrow_forward

- Assuming that the quasi reorganization shall be accomplished as follows: Property, plant and equipment are to be reduced to their fair market value of P800,000. Inventories are to be written down by P50,000. • Unaccrued obligation shall be recognized at P150,000. • The par value of ordinary Shares will be reduced to P5. 1. What is the balance of the retained earnings account as of 31 December 2019? Assuming that the quasi reorganization shall be accomplished as follows: Property, plant and equipment are to be reduced to their fair market value of P800,000. Inventories are to be written down by P50,000. • Unaccrued obligation shall be recognized at P150,000. • The par value of ordinary Shares will be reduced to P5. 2. What is the balance of the retained earnings account as of 31 December 2019?arrow_forwardAt December 31, 2020, the available-for-sale debt portfolio for Ivanhoe, Inc. is as follows. Security Cost Fair Value UnrealizedGain (Loss) A $17,100 $14,200 $(2,900) B 11,800 15,300 3,500 C 22,000 25,600 3,600 Total $50,900 $55,100 4,200 Previous fair value adjustment balance—Dr. 300 Fair value adjustment—Dr. $3,900 On January 20, 2021, Ivanhoe, Inc. sold security A for $14,300. The sale proceeds are net of brokerage fees.Ivanhoe, Inc. reports net income in 2020 of $117,000 and in 2021 of $141,000. Total holding gains (including any realized holding gain or loss) equal $42,000 in 2021. 1. Prepare a statement of comprehensive income for 2020, starting with net income. 2. Prepare a statement of comprehensive income for 2021, starting with net income.arrow_forwardpresentation. EH.6 (LO 3), AP At December 31, 2022, the trading debt securities for Gwynn, Inc. are as follows. Fair Value Instructions Security A B C Total Cost $18,100 12,500 23,000 $53,600 $16,000 14,800 18,000 $48,800 a. Prepare the adjusting entry at December 31, 2022, to report the securities at fair value. b. Show the balance sheet and income statement presentation at December 31, 2022, after adjustment to fair value. Prepare adjusting entry to record fair value, and indicate statement presentation.arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education