Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

make sure there is no eroor when giving me the answers please ASAP

A Index has currently a value of $10,000, and pays a dividend yield of 3%. What should be the price of a futures contract on the index for delivery in 1 year and what for delivery in 2 years? Assume that the interest rates for 2 years out are flat at 9%. If the one-year futures is trading in the market for $9,500 what will you do?

2) show in a diagram or graph or illustration of how the abritrage opprotunity happens.

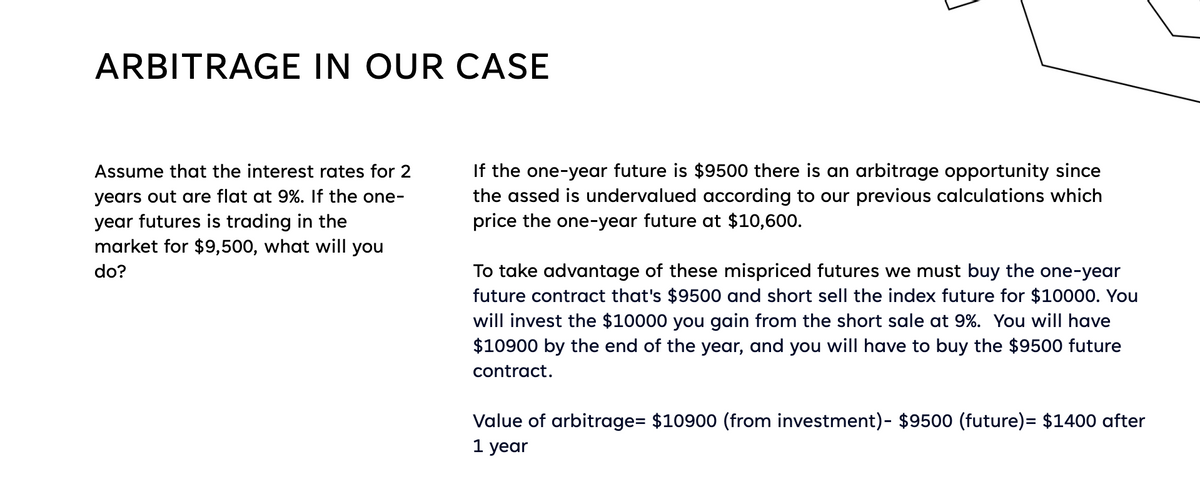

Transcribed Image Text:ARBITRAGE IN OUR CASE

Assume that the interest rates for 2

years out are flat at 9%. If the one-

year futures is trading in the

market for $9,500, what will you

do?

If the one-year future is $9500 there is an arbitrage opportunity since

the assed is undervalued according to our previous calculations which

price the one-year future at $10,600.

To take advantage of these mispriced futures we must buy the one-year

future contract that's $9500 and short sell the index future for $10000. You

will invest the $10000 you gain from the short sale at 9%. You will have

$10900 by the end of the year, and you will have to buy the $9500 future

contract.

Value of arbitrage= $10900 (from investment)- $9500 (future) = $1400 after

1 year

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps with 5 images

Knowledge Booster

Similar questions

- Please give me answer fast. I will rate for sure.arrow_forwardPlease no written by hand and no image 2. A forward contract for 4 months is entered into when a stock index is at 1000. If the risk free interest rate is 3% per year (with continuous compounding) and the dividend yield on the index is 2% per year, what is the futures price? After 1 month the index price is 980, what is the value of the futures agreement assuming the risk free rate with continuous compounding is now 5% (but the original dividend rate remains 2%) and the contract price is equal to $50 times the index value?arrow_forwardA non-dividend paying asset is current priced at $25 and the risk-free interest rate is 8% per annum. Today, you enter into a six-month futures contract to buy a unit of this asset. Three months from now the underlying price has fallen to $20 (but note that the interest rate has not moved). Which of the answers below is closest to the fall in the futures price? Use discrete discounting. a. $4.50 b. $6.50 c. $7.50 d. $5.50arrow_forward

- The futures price of an asset is currently 80 and the risk-free rate is 4%. A six-month put on the futures with a strike price of 85 is currently worth 6.5. What is the value of a six-month call on the futures with a strike price of 85 if both the put and call are European? What is the range of possible values of the six-month call with a strike price of 85 if both put and call are American? Show all work and briefly discuss.arrow_forwardThe spot price of oil is $40 per barrel and the cost of storing a barrel of oil for one year is $3.3, payable at the end of the year. The risk-free interest rate is 2.6% per annum, continuously compounded. What is an upper bound for the one-year futures price of oil? Your answer should be correct to one decimal place. Assume there are no transaction costs involved in arbitraging over-priced futures contracts.arrow_forward(mark-to-market) You enter a long position in a € future contract with the size of €125,000 today. The futures expire in 90 days. The interest rates are iS = 3.9% and i€ = 3.9%. The current spot rate is $1.38/€. Assume 360 days a year. If the spot rate is $1.43/€ the next day and interest rates remain the same, your profit or loss for this day is S _. (Keep the sign and two decimal places.)arrow_forward

- If you put on the futures position from 2 at a price of 0.043 $/peso, and if the peso appreciates from the spot rate of 0.045 $/peso by 15% in the next 6 months, what will be the total value of your position (the payable plus the future) in 6 months (again, this should be a negative number)?arrow_forwardA non-dividend paying asset is current priced at $25 and the risk-free interest rate is 8% per annum. Today, you enter into a six-month futures contract to buy a unit of this asset. Three months from now the underlying price has fallen to $18 (but note that the interest rate has not moved). Which of the answers below is closest to the fall in the futures price? Use discrete discounting. Question 7Answer a. $6.50 b. $5.50 c. $7.50 d. $4.50arrow_forwardSuppose that a stock is currently trading at £ 38, and that the current prices for European call and put options on this stock with maturity T 10 years and identical strike price K are equal to £30 and £35, respectively. Assuming that interest is compounded annually at rate 4%, determine the strike price to the nearest pence. Do not type in the pound sign. =arrow_forward

- (mark-to-market) You enter a long position in a € future contract with the size of €125,000 today. The futures expire in 90 days. The interest rates are i$=2.6% and iç-5.5%. The current spot rate is $1.38/€. Assume 360 days a year. If the spot rate is $1.36/€ the next day and interest rates remain the same, your profit or loss for this day is $_ ____.(Keep the sign and two decimal places.)arrow_forwardhelp please answer in text form with proper workings and explanation for each and every part and steps with concept and introduction no AI no copy paste remember answer must be in proper format with all workingarrow_forwardSuppose the 6-month Mini S&P 500 futures price is 1,168.44, while the cash price is 1,150.55. What is the implied dividend yield on the S&P 500 if the risk-free interest rate is 4.3 percent? (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.) Implied dividend yield %arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education