Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

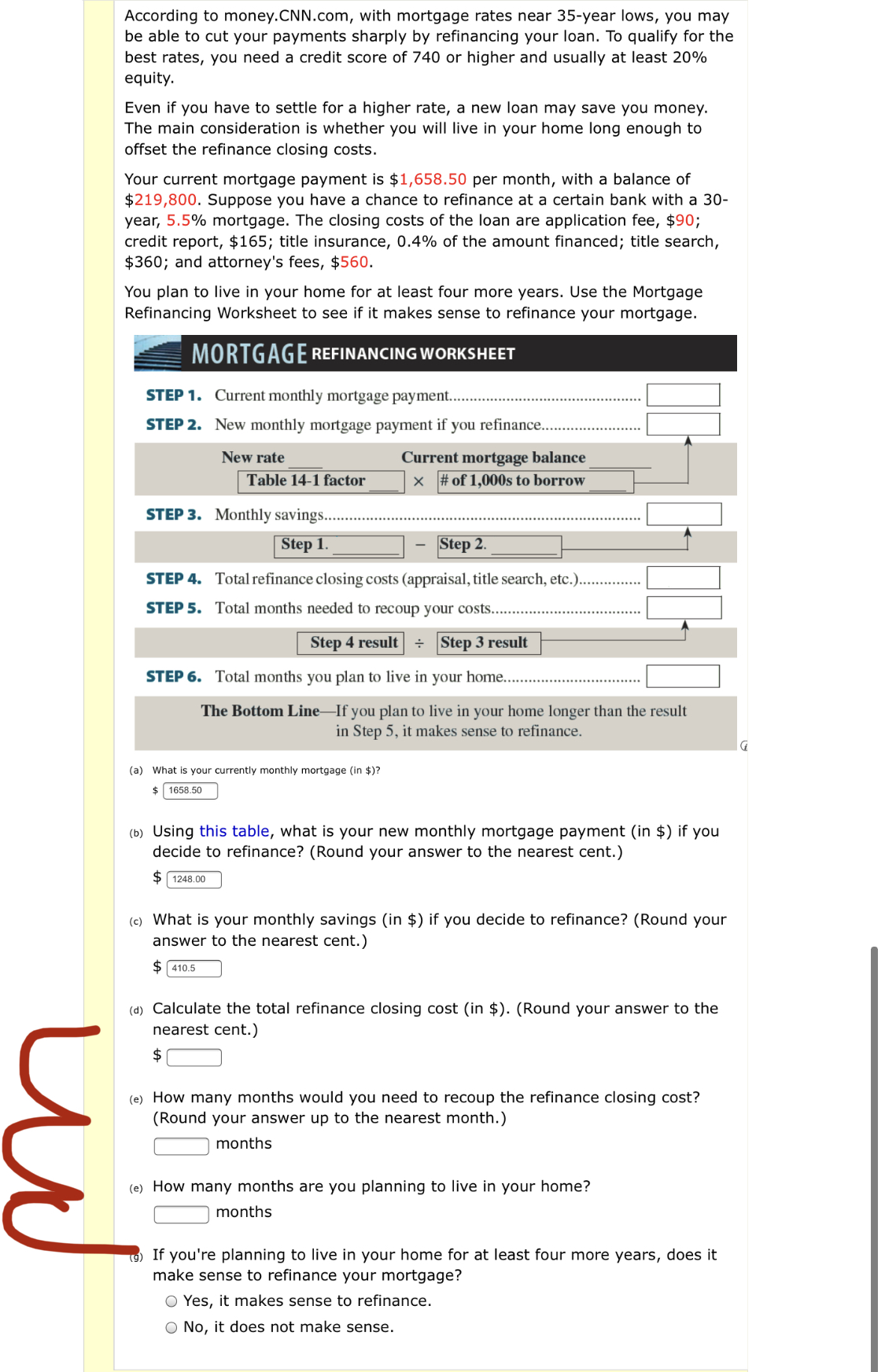

Transcribed Image Text:According to money.CNN.com, with mortgage rates near 35-year lows, you may

be able to cut your payments sharply by refinancing your loan. To qualify for the

best rates, you need a credit score of 740 or higher and usually at least 20%

equity.

Even if you have to settle for a higher rate, a new loan may save you money.

The main consideration is whether you will live in your home long enough to

offset the refinance closing costs.

Your current mortgage payment is $1,658.50 per month, with a balance of

$219,800. Suppose you have a chance to refinance at a certain bank with a 30-

year, 5.5% mortgage. The closing costs of the loan are application fee, $90;

credit report, $165; title insurance, 0.4% of the amount financed; title search,

$360; and attorney's fees, $560.

You plan to live in your home for at least four more years. Use the Mortgage

Refinancing Worksheet to see if it makes sense to refinance your mortgage.

MORTGAGE REFINANCING WORKSHEET

STEP 1. Current monthly mortgage payment..

STEP 2. New monthly mortgage payment if you refinance..

Current mortgage balance

x # of 1,000s to borrow

New rate

Table 14-1 factor

STEP 3. Monthly savings...

Step 1.

Step 2.

STEP 4. Total refinance closing costs (appraisal, title search, etc.)..

STEP 5. Total months needed to recoup your costs....

Step 4 result ÷ Step 3 result

STEP 6. Total months you plan to live in your home...

The Bottom LineIf you plan to live in your home longer than the result

in Step 5, it makes sense to refinance.

(a) What is your currently monthly mortgage (in $)?

$ 1658.50

(b) Using this table, what is your new monthly mortgage payment (in $) if you

decide to refinance? (Round your answer to the nearest cent.)

$ 1248.00

(c) What is your monthly savings (in $) if you decide to refinance? (Round your

answer to the nearest cent.)

$ 410.5

(d) Calculate the total refinance closing cost (in $). (Round your answer to the

nearest cent.)

$

(e) How many months would you need to recoup the refinance closing cost?

(Round your answer up to the nearest month.)

months

(e) How many months are you planning to live in your home?

months

) If you're planning to live in your home for at least four more years, does it

make sense to refinance your mortgage?

O Yes, it makes sense to refinance.

O No, it does not make sense.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- The buyer of a piece of real estate is often given the option of buying down the loan. This option gives the buyer a choice of loan terms in which various combinations of interest rates and discount points are offered. The choice of how many points and what rate is optimal is often a matter of how long the buyer intends to keep the property. Darrell Frye is planning to buy an office building at a cost of $983,000. He must pay 10% down and has a choice of financing terms. He can select from a 9% 30-year loan and pay 4 discount points, a 9.25% 30-year loan and pay 3 discount points, or a 9.5% 30-year loan and pay 2 discount points. Darrell expects to hold the building for two years and then sell it. Except for the three rate and discount point combinations, all other costs of purchasing and selling are fixed and identical. (Round your answers to the nearest cent. Use this table, if necessary.) (a) What is the amount being financed? $ (b) If Darrell chooses the 4-point 9% loan,…arrow_forwardAccording to money.CNN.com, with mortgage rates near 35-year lows, you may be able to cut your payments sharply by refinancing your loan. To qualify for the best rates, you need a credit score of 740 or higher and usually at least 20% equity. Even if you have to settle for a higher rate, a new loan may save you money. The main consideration is whether you will live in your home long enough to offset the refinance closing costs. Your current mortgage payment is $1,578.50 per month, with a balance of $217,800. Suppose you have a chance to refinance at a certain bank with a 30-year, 5.75% mortgage. The closing costs of the loan are application fee, $80; credit report, $165; title insurance, 0.4% of the amount financed; title search, $360; and attorney's fees, $570. You plan to live in your home for at least four more years. Use the Mortgage Refinancing Worksheet to see if it makes sense to refinance your mortgage. MORTGAGE REFINANCING WORKSHEET STEP 1. Current monthly mortgage payment...…arrow_forwardThe figure below shows costs for a current home mortgage versus a refinanced home mortgage. Refinancing has initial costs, but results in a lower monthly payment. Which best describes the lines? ***SEE CHART**** The blue line is for refinancing, which starts cheaper but eventually is costlier The blue line is for refinancing, which starts costlier but eventually is cheaper The orange line is for refinancing, which starts cheaper but eventually is costlier The orange line is for refinancing, which starts costlier but eventually is cheaperarrow_forward

- The buyer of a piece of real estate is often given the option of buying down the loan. This option gives the buyer a choice of loan terms in which various combinations of interest rates and discount points are offered. The choice of how many points and what rate is optimal is often a matter of how long the buyer intends to keep the property. Darrell Frye is planning to buy an office building at a cost of $982,000. He must pay 10% down and has a choice of financing terms. He can select from a 9% 30-year loan and pay 4 discount points, a 9.25% 30-year loan and pay 3 discount points, or a 9.5% 30-year loan and pay 2 discount points. Darrell expects to hold the building for three years and then sell it. Except for the three rate and discount point combinations, all other costs of purchasing and selling are fixed and identical. (Round your answers to the nearest cent. Use this table, if necessary.) (a) What is the amount being financed? 2$ (b) If Darrell chooses the 4-point 9% loan, what…arrow_forward6) Over the past 40 years, interest rates have varied widely. The rate for a 30-year mortgage reached a high of 14.75% in July 1984, and it reached 3.31% in November 2012. A significant impact of lower interest rates on society is that they enable more people to afford the purchase of a home. In the following exercise, we consider the purchase of a home that sells for $125,000. Assume that we can make a down payment of $25,000, so we need to borrow $100,000. We assume that our annual income is $35,000 and that we have no other debt. If we can afford to pay a monthly amount of $566.67, determine how much we can borrow if the term is 30 years and the interest rate is at the historic high of 14.75%. (Round your answer to the nearest dollar.) $ Can we afford the home? Yes No If we can afford to pay a monthly amount of $566.67, determine how much we can borrow if the term is 30 years and the interest rate is 3.31%. (Round your answer to the nearest dollar.) $ Can we afford the home now? Yes…arrow_forwardYou get hired by a residential mortgage lender to help them revamp their mortgage pricing models. They ask you to start by exploring three common client scenarios. First, they give you the “Second Lien Scenario.” In this scenario, a borrower goes to one of your competitors with the intention to buy a $1.2 million house. Your competitor gives them two options: • A 30-year, fully amortizing FRM with 80% LTV and an interest rate of 6.1%; or • A 20-year, fully amortizing FRM with 90% LTV and an interest rate of 6.8%. Next, the borrower comes to you and asks for a quote on a second lien (i.e. a junior loan) worth 10% LTV for 30 years. They want to price a scenario where they get the 80% LTV loan from your competitor and the 10% LTV loan from you instead of the 90% LTV loan from your competitor (in other words, paying for the same amount with two loans instead of one). 1. In order to be competitive, (a) what monthly payment and (b) what interest rate should you charge on this second lien?…arrow_forward

- The buyer of a piece of real estate is often given the option of buying down the loan. This option gives the buyer a choice of loan terms in which various combinations of interest rates and discount points are offered. The choice of how many points and what rate is optimal is often a matter of how long the buyer intends to keep the property. Darrell Frye is planning to buy an office building at a cost of $982,000. He must pay 10% down and has a choice of financing terms. He can select from a 9% 30-year loan and pay 4 discount points, a 9.25% 30-year loan and pay 3 discount points, or a 9.5% 30-year loan and pay 2 discount points. Darrell expects to hold the building for three years and then sell it. Except for the three rate and discount point combinations, all other costs of purchasing and selling are fixed and identical. (Round your answers to the nearest cent. Use this table, if necessary.)arrow_forwardAccording to money.CNN.com, with mortgage rates near 35-year lows, you may be able to cut your payments sharply by refinancing your loan. To qualify for the best rates, you need a credit score of 740 or higher and usually at least 20% equity. Even if you have to settle for a higher rate, a new loan may save you money. The main consideration is whether you will live in your home long enough to offset the refinance closing costs. Your current mortgage payment is $1,578.50 per month, with a balance of $219,800. Suppose you have a chance to refinance at a certain bank with a 30-year, 5.75% mortgage. The closing costs of the loan are application fee, $90; credit report, $165; title insurance, 0.4% of the amount financed; title search, $360; and attorney's fees, $570. You plan to live in your home for at least four more years. Use the Mortgage Refinancing Worksheet to see if it makes sense to refinance your mortgage. (a) What is your currently monthly mortgage (in $)? $ (b) Using…arrow_forwardThe buyer of a piece of real estate is often given the option of buying down the loan. This option gives the buyer a choice of loan terms in which various combinations of interest rates and discount points are offered. The choice of how many points and what rate is optimal is often a matter of how long the buyer intends to keep the property. Darrell Frye is planning to buy an office building at a cost of $983,000. He must pay 10% down and has a choice of financing terms. He can select from a 9% 30-year loan and pay 4 discount points, a 9.25% 30-year loan and pay 3 discount points, or a 9.5% 30-year loan and pay 2 discount points. Darrell expects to hold the building for four years and then sell it. Except for the three rate and discount point combinations, all other costs of purchasing and selling are fixed and identical. (Round your answers to the nearest cent. Use this table, if necessary.) (d): If Darrell chooses the 2-point 9.5% loan, what will be his total outlay in points…arrow_forward

- According to money.CNN.com, with mortgage rates near 35-year lows, you may be able to cut your payments sharply by refinancing your loan. To qualify for the best rates, you need a credit score of 740 or higher and usually at least 20% equity. Even if you have to settle for a higher rate, a new loan may save you money. The main consideration is whether you will live in your home long enough to offset the refinance closing costs. Your current mortgage payment is $1,658.50 per month, with a balance of $219,800. Suppose you have a chance to refinance at a certain bank with a 30-year, 5.5% mortgage. The closing costs of the loan are application fee, $80; credit report, $165; title insurance, 0.4% of the amount financed; title search, $360; and attorney's fees, $570. You plan to live in your home for at least four more years. Use the Mortgage Refinancing Worksheet to see if it makes sense to refinance your mortgage. (attached is chart) (a): What is your currently monthly mortgage (in…arrow_forwardNote:- Do not provide handwritten solution. Maintain accuracy and quality in your answer. Take care of plagiarism. Answer completely.arrow_forwardThe buyer of a piece of real estate is often given the option of buying down the loan. This option gives the buyer a choice of loan terms in which various combinations of interest rates and discount points are offered. The choice of how many points and what rate is optimal is often a matter of how long the buyer intends to keep the property. Darrell Frye is planning to buy an office building at a cost of $986,000. He must pay 10% down and has a choice of financing terms. He can select from a 9% 30-year loan and pay 4 discount points, a 9.25% 30-year loan and pay 3 discount points, or a 9.5% 30-year loan and pay 2 discount points. Darrell expects to hold the building for three years and then sell it. Except for the three rate and discount point combinations, all other costs of purchasing and selling are fixed and identical. (Round your answers to the nearest cent. Use this table, if necessary.) I want to know how to find this out: If Darrell chooses the 4-point 9% loan, what will be his…arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education