Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

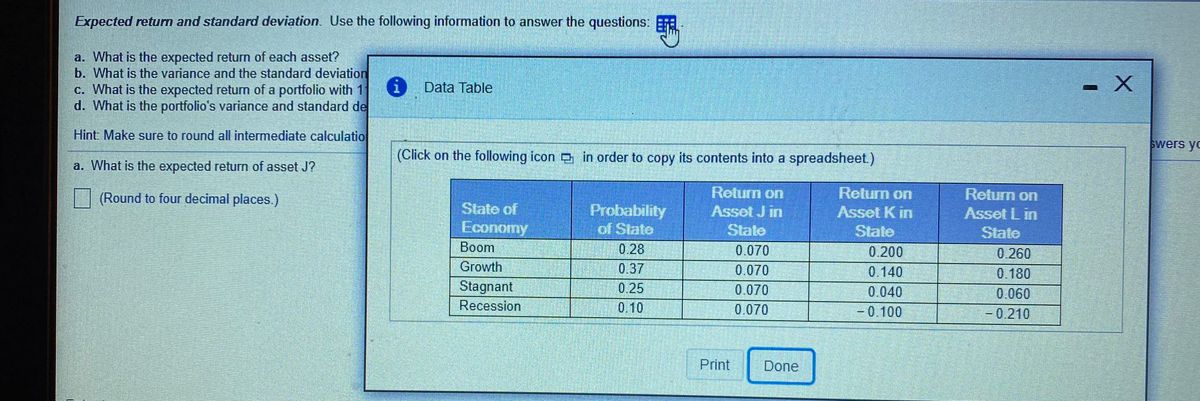

Transcribed Image Text:Expected retun and standard deviation. Use the following information to answer the questions:

a. What is the expected return of each asset?

b. What is the variance and the standard deviation

c. What is the expected return of a portfolio with 1 1 Data Table

d. What is the portfolio's variance and standard de

- X

Hint Make sure to round all intermediate calculatio

Swers yo

(Click on the following icon D in order to copy its contents into a spreadsheet.)

a. What is the expected return of asset J?

(Round to four decimal places.)

Return on

Return on

Return on

Probability

of State

State of

Asset J in

Asset Kin

State

0.200

0.140

0.040

Asset L in

Economy

State

State

Вoom

0.28

0.070

0.260

0.180

Growth

0.37

0.25

0.070

Stagnant

0.070

0.060

-0.210

Recession

0.10

0.070

-0.100

Print

Done

Transcribed Image Text:Expected return and standard deviation. Use the following information to answer the questions:

a. What is the expected retum of each asset?

b. What is the variance and the standard deviation of each asset?

c. What is the expected return of a portfolio with 11% in asset J, 49% in asset K, and 40% in asset L?

d. What is the portfolio's variance and standard deviation using the same asset weights from part (c)?

Hint Make sure to round all intermediate calculations to at least seven (7) decimal places. The input instructions, phrases in parenthesis after each answer box, only apply for the answers you will type.

a. What is the expected return of asset J?

(Round to four decimal places.)

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- Are the following statements true or false? Provide a short justification for vour answer. а) assets A, B, C, with expected returns and standard deviations: Suppose you are a mean-variance optimizer. The risk-free rate is 3%. There are three risky E [řA] = 10%, SD [řA] = 5% E [řB] = 15%, SD [řB] = 7% E [řc] = 12%, SD [ŕc] = 9% You cannot invest in all three risky assets. Instead, you have to choose whether to invest in only assets (A, B), or only assets (A, C). Asset B mean-variance dominates asset C, since it has higher return and lower standard deviation than asset C. Thus, as long as you are risk-averse, you would always prefer the set of assets (A, B) to the set assets (A, C). b) the same market B's. The covariance matrix between A, B, C is: Suppose the CAPM holds. Consider three stocks A, B, C. Suppose that assets A, B, C have 0.05 0.03 0.03 0.05 0.05 Assets A, B, C have the same variance. However, assets A and B are positively correlated with each other, so they have larger…arrow_forwardThe standard deviation of return on investment a is 0.10, while the standard deviation of return on investment b is 0.04. If the correlation coefficient between the returns on A and B is_____________. A. -0.0447 B. -0.0020 C. 0.0020 D. 0.0447arrow_forwardTime series forecasting maybe used to predict future values of a variable by: A. A simple moving average B. A weighted moving average C. Exponential smoothing D. All of the abovearrow_forward

- The variance of expected returns is equal to the square root of the expected returns. a. True b. Falsearrow_forwardneed answer fast hand written , <<<<<arrow_forwardAssuming that the rates of return associated with a given asset investment are normally distributed; that the expected return, r, is 18.7%; and that the coefficient of variation, CV, is 1.88, answer the following questions: a. Find the standard deviation of returns, sigma Subscript rσr. b. Calculate the range of expected return outcomes associated with the following probabilities of occurrence: (1) 68%, (2) 95%, (3) 99%.arrow_forward

- 1. Determine the expected return and the variance of the portfolio formed by the two assets S₁, S₂ with weights ₁ = 0.6, x2 = 0.4. The assets returns are described by the following scheme: scenario W1 2لا W3 probability 0.1 0.4 0.5 T1 -20% 0% 20% 12 -10% 20% 40%arrow_forwardSuppose two asset returns are described by a two factor model, n = 0% + 11 + 1.82 + e1 2 = -1% + 2/1 + 0.52 + e2 where the volatility of first factor is 30%, the volatility of the second factor is 10%, and the correlation between the two factors is 0.5. Suppose also that the volatilities of the error terms ej and ez are both 10%. What is the covariance of n and r2 ? (Nearest 0.0001).arrow_forwardGiven the following probability distribution, what are the expected return and the standard deviation of returns for Security J? State Pi ri 1 0.5 11% 2 0.3 8% 3 0.2 5% O 9.40%; 2.04% O 8.90%; 2.34% O 7.40%; 2.94% O 8.40%; 2.64% O 7.90%; 1.74%arrow_forward

- Suppose that there are four risky assets whose expected returns E(r) and variance- covariance matrix (S) are shown in the spreadsheet below. We also consider the portfolio weights of two portfolios x and y of risky assets (see Cells B8:E9): 1 8 Portfolio x 9 Portfolio y A FOUR-ASSET PORTFOLIO PROBLEM Variance-covariance, S 20 Portfolio variance, 21 Portfollo standard deviation o 0.10 0.01 0.03 0.05 11 Portfolio x and y statistics: Mean, variance, covariance, correlation 12 Mean, Ejr, 13 Variance, 14 Covariance() 15 Correlation P 16 17 Calculating returns of combinations of Portfolio x and Portfolio y 18 Proportion of x 19 Mean portfolio return, r 0.01 0.30 0.06 -0.04 0.20 0.20 10.50% 0.1216 0.0714 0.4540 ? ? ? 0.3 0.03 0.06 0.40 0.02 0.30 0.10 ? 0.05 0.02 0.50 0.40 0.10 0.10 0.60 Mean, Er Variance, 0.2014 Question il Question ili Mean returns E(r) ? 7% 9% 11% 20% Question i i. Write the Excel formula used to estimate the mean and variance of portfolio y in cells E12 and E13,…arrow_forwardPLEASE DO THIS IN EXCELarrow_forwardQuestion 1 Are the following statements true or false? Provide a short justification for your answer. (You are evaluated on your justification.) Remember that a statement is false if any part of the statement is false. A single correct counterexample is sufficient to show that a statement is false. a) assets A, B, C, with expected returns and standard deviations: Suppose you are a mean-variance optimizer. The risk-free rate is 3%. There are three risky E [řa] = 10%, SD [FA] = 5% E [řB] = 15%, SD [řB] = 7% E [řc] = 12%, SD [řc] = 9% You cannot invest in all three risky assets. Instead, you have to choose whether to invest in only assets (A, B), or only assets (A, C). Asset B mean-variance dominates asset C, since it has higher return and lower standard deviation than asset C. Thus, as long as you are risk-averse, you would always prefer the set of assets (A, B) to the set assets (A, C). b) the same market B's. The covariance matrix between A, B, C is: Suppose the CAPM holds. Consider…arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education