Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

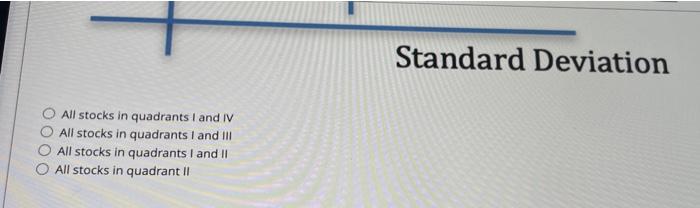

Transcribed Image Text:All stocks in quadrants I and IV

All stocks in quadrants I and III

All stocks in quadrants I and II

O All stocks in quadrant II

Standard Deviation

Transcribed Image Text:Suppose you have mean-variance utility function with a coefficient of risk Aversion-0, which stocks are preferred to P.

E(r)

III

IP

II

IV

Standard Deviation

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- Is the portfolio risk the weighted average of the variance or covariance?arrow_forwardThe variances of stocks A and B are 1 percentage square and 4 percentage square, respectively. If the covariance between the two stocks is 0.6 percentage square, what is the correlation? Dontarrow_forwardThe lower the standard deviation of returns on a security, the _____ the expected rate of return and the _____ the risk. Multiple Choice lower; lower lower; higher higher; lower higher; higherarrow_forward

- Question 1 Are the following statements true or false? Provide a short justification for your answer. (You are evaluated on your justification.) Remember that a statement is false if any part of the statement is false. A single correct counterexample is sufficient to show that a statement is false. a) assets A, B, C, with expected returns and standard deviations: Suppose you are a mean-variance optimizer. The risk-free rate is 3%. There are three risky E [řa] = 10%, SD [FA] = 5% E [řB] = 15%, SD [řB] = 7% E [řc] = 12%, SD [řc] = 9% You cannot invest in all three risky assets. Instead, you have to choose whether to invest in only assets (A, B), or only assets (A, C). Asset B mean-variance dominates asset C, since it has higher return and lower standard deviation than asset C. Thus, as long as you are risk-averse, you would always prefer the set of assets (A, B) to the set assets (A, C). b) the same market B's. The covariance matrix between A, B, C is: Suppose the CAPM holds. Consider…arrow_forwardH Consider the three stocks in the following table. Pe represents price at time t, and Qe represents shares outstanding at time t Stock C splits two-for-one in the last period. Pe 81 41 82 lo 100 200 200 Rate of return P₁ 86 36 92 li 100 200 200 % P₂ 86 36 46 Required: Calculate the first-period rates of return on the following indexes of the three stocks: (Do not round intermediate calculations. Round your answers to 2 decimal places.) a. A market value-weighted index 2₂ 100 200 400arrow_forwardT/F. The “Fear Index” is calculated using estimates of implied volatility. Group of answer choices True Falsearrow_forward

- According to modern portfolio theory, pair-wise covariance is more important to total portfolio risk than individual security variance. True or Falsearrow_forwardHow does standard deviation and variance affect portfolio risk, more so than expected return?arrow_forwardOver time beta coefficients tend to approach the beta value of the market portfolio. O True Falsearrow_forward

- Portfolios that offer the highest expected return for a given variance (or standard deviation) are known as efficient portfolios. O true falsearrow_forwardGiven the following probability distribution, what is the standard deviation of returns for Security J? (Expresss your answer in percentage, but do not include the percent sign, %, i.e., 4.65) State Pi rJ 1 0.2 8 % 2 0.6 12 3 0.2 17arrow_forwardExplain well all question with proper answer. And type the answer step by step.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education