Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

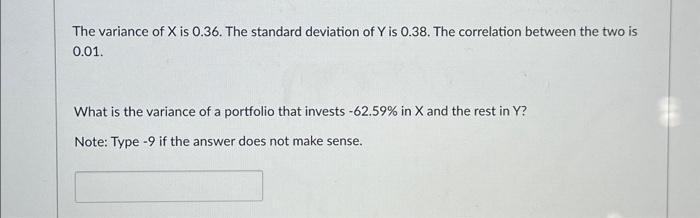

Transcribed Image Text:The variance of X is 0.36. The standard deviation of Y is 0.38. The correlation between the two is

0.01.

What is the variance of a portfolio that invests -62.59% in X and the rest in Y?

Note: Type -9 if the answer does not make sense.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 3 steps with 1 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- If standard deviation of security A is 27% and security B is 18%, the correlation coefficient between security A and B is -1, the weight of A for a minimum variance portfolio will be a. 0.4 b. 0.6 c. 0.2 d. 0.5arrow_forwardWhat is the expected return on a two asset portfolio and what are its variance and standard deviation. What is R squared? Please keep it short and simple but making lots of sense. thanksarrow_forwardStock A has a return variance (that is σ2) of 0.02. The market portfolio has a return variance of 0.03. The covariance between stock A’s return and market portfolio’s return is 0.01. Stock A has an expected return of 0.09, while the market has an expected return of 0.12. What is the expected return and standard deviation of a portfolio that is 65% invested in A and 35% invested in the market portfolio? a. ER = 10.1%, σ = 12.9% b. ER = 10.8%, σ = 16.7% c. ER = 10.1%, σ = 16.7% d. ER = 9.0%, σ = 12.9% e. ER = 8.5%, σ = 10.1%arrow_forward

- When calculating the beta of security by running a simple regression in Excel, which of the following is NOT true? O The alpha or intercept coefficient in the output table measures by how much the security outperformed the market index, adjusted for risk. O The beta can be found in the X Variable coefficient cell in the output table. O The market index should be used as the 'dependent' variable Y. The returns for the security should be the 'independent' variable X. O If the R-Square in the output table is .20, that means that 20% of the variation in the dependent variable can be explained by variations in the independent variable.arrow_forwardThe variance of expected returns is equal to the square root of the expected returns. a. True b. Falsearrow_forwardConsider a long-short portfolio. Beta of this portfolio is zero and its volatility is 20% . What is the portfolio-specific (unsystematic) variance of this portfolioarrow_forward

- Consider two risky assets that have returns variances of 0.0625 and 0.0324, respectively. The assets' standard deviations of returns are then 25% and 1 8%, respectively. Calculate the variances and standard deviations of portfolio returns for an equal-weighted portfolio of the two assets when their correlation of returns is 1.arrow_forwardneed answer fast hand written , <<<<<arrow_forwardUnder the stop-loss reinsurance model, suppose the total claim follows exponential distribution with mean 1/λ. For given premium P, (a) Derive the retention level M; (b) Calculate the sum of shared variances Var(X*) + Var.Xarrow_forward

- Assuming that the rates of return associated with a given asset investment are normally distributed; that the expected return, r, is 18.7%; and that the coefficient of variation, CV, is 1.88, answer the following questions: a. Find the standard deviation of returns, sigma Subscript rσr. b. Calculate the range of expected return outcomes associated with the following probabilities of occurrence: (1) 68%, (2) 95%, (3) 99%.arrow_forward1. Determine the expected return and the variance of the portfolio formed by the two assets S₁, S₂ with weights ₁ = 0.6, x2 = 0.4. The assets returns are described by the following scheme: scenario W1 2لا W3 probability 0.1 0.4 0.5 T1 -20% 0% 20% 12 -10% 20% 40%arrow_forwardConsider two stocks M and N with a standard deviation of 25% and 40% respectively. The returns of the two stocks are perfectly negatively correlated. Proportion of investment to be made in stock M for zero variance portfolio is____ a. 62% b. 38% c. 50% d. Cannot be determinedarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education