ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

Economic

Q7 onlys

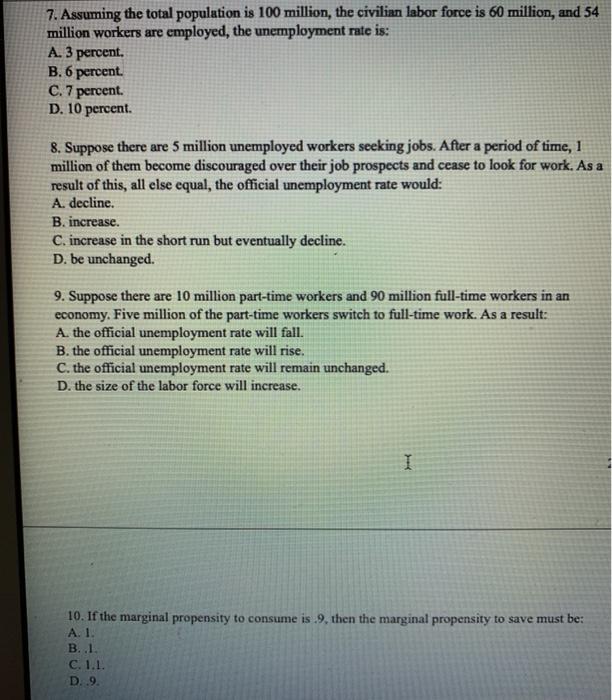

Transcribed Image Text:7. Assuming the total population is 100 million, the civilian labor force is 60 million, and 54

million workers are employed, the unemployment rate is:

A. 3 percent.

B. 6 percent.

C. 7 percent.

D. 10 percent.

8. Suppose there are 5 million unemployed workers seeking jobs. After a period of time, 1

million of them become discouraged over their job prospects and cease to look for work. As a

result of this, all else equal, the official unemployment rate would:

A. decline.

B. increase.

C. increase in the short run but eventually decline.

D. be unchanged.

9. Suppose there are 10 million part-time workers and 90 million full-time workers in an

Five million of the part-time workers switch to full-time work. As a result:

economy.

A. the official unemployment rate will fall.

B. the official unemployment rate will rise.

C. the official unemployment rate will remain unchanged.

D. the size of the labor force will increase.

10. If the marginal propensity to consume is .9, then the marginal propensity to save must be:

A. 1.

B. .1.

C. 1.1.

D..9.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- The research department at a manufacturing company has developed a new process that it believes will result in an improved product Management must decide whether to go ahead and market the new product. The new product may or may not be better than the old one. If the new product is better and the company decides to market it, sales should increase by $50,000. If it is not better and they replace the old product with the new product on the market, they will lose $24,000 to competitors. If they decide not to market the new product, they will lose a total of $30,000 if it is better and just research costs of $10,000 if it is not. Answer parts a through c below. (a) Prepare a payoff matrix. (Type an integer or decimal for each matrix element. Do not include the $ symbol in your answer.) (b) If management believes there is a probability of 0.4 that the new product is better, find the expected profits under each strategy and determine the best action. Select the correct answer below and fill…arrow_forwardYour company has a customer list that includes 3000 people. Your market research indicates that 90 of them responded to the coupon. If you send a coupon to ONE customer at random, what’s the probability that he or she will use the coupon? Group of answer choices 3%. 9%. 30%. 90%. None of the above.arrow_forwardTwo identically able agents are competing for a promotion. The promotion is awarded on the basis of output (whomever has the highest output, gets the promotion). Because there are only two workers competing for one prize, the losing prize=0 and the winning prize =P. The output for each agent is equal to his or her effort level times a productivity parameter (d). (i.e. Q2=dE1 , Q2=dE2). If the distribution of “relative luck” is uniform, the probability of winning the promotion for agent 1 will be a function of his effort (E1) and the effort level of Agent 2 (E2). The formula is given by...Prob(win)=0.5 + α(E1-E2), where α is a parameter that reflects uncertainty and errors in measurement. High measurement errors are associated with small values of α (think about this: if there are high measurement errors, then the level of an agent’s effort will have a smaller effect on his/her chances of winning). Using this information, please answer the following questions. Both workers have a…arrow_forward

- BN10.2 Case: Jennifer is willing to Pay $300 to Insure against the Theft of a $8,000 Necklace. The Probability of Theft is 4%. Question: What is Jennifer's Risk Tolerance?arrow_forwardThe probability that it will rain on any given day is 0.20, and the probability is independent from day to day. You are trying to decide whether or not to make a tee time tomorrow to play golf. This requires a commitment on your part of turning down, say, movie tickets in favor of playing golf. If you accept the tickets, you also make the commitment not to go golfing. There is a weather forecast that signals whether it will rain tomorrow or not. There is a 0.80 probability that it rains when there is a "rainy" forecast and a 0.125 probability of rain when there is a "sunny" forecast. The overall probability of getting a "rainy" forecast is 0.111. Assume you are risk neutral. You place the following monetary values on the potential outcomes: a sunny day at $95 the golf course a rainy day at the movies a rainy day at home a sunny day at the movies $20 -$18 $1arrow_forwardIn the late 1990s, car leasing was very popular In the United States. A customer would lease a car from the manufacturer for a set term, usually two years, and then have the option of keeping the car. If the customer decided to keep the car, the customer would pay a price to the manufacturer, the "residual value," computed as 60% Df the new car price. The manufacturer would then sell the retumed cars at auction. In 1999, manufacturers lost an average of $480 on each returned car (the auction price was, on average, $480 less than the residual value). Suppose two customers have leased cars from a manufacturer. Their lease agreements are up, and they are considering whether keep (and purchase at 60% of the new car price) their cars or return thelr cars. Two years ago, Becky leased a car valued new at $18,500. If she returns the car, the manufacturer could likely get $12,950 at auction for the car. Eleen also leased a car, valued new at $19,000, two years ago. If she returns the car, the…arrow_forward

- Calculate absolute and relative risk aversion for U(x)=ln(x) and U(x)=-e-x where wealth is (w)arrow_forwardYou work at a mechanic shop. 40% of cars that come in have a flat tire. If there are 50 cars in the shop, what is the probability that more than 30 have a flat tire? Round to three decimal points.arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education