ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

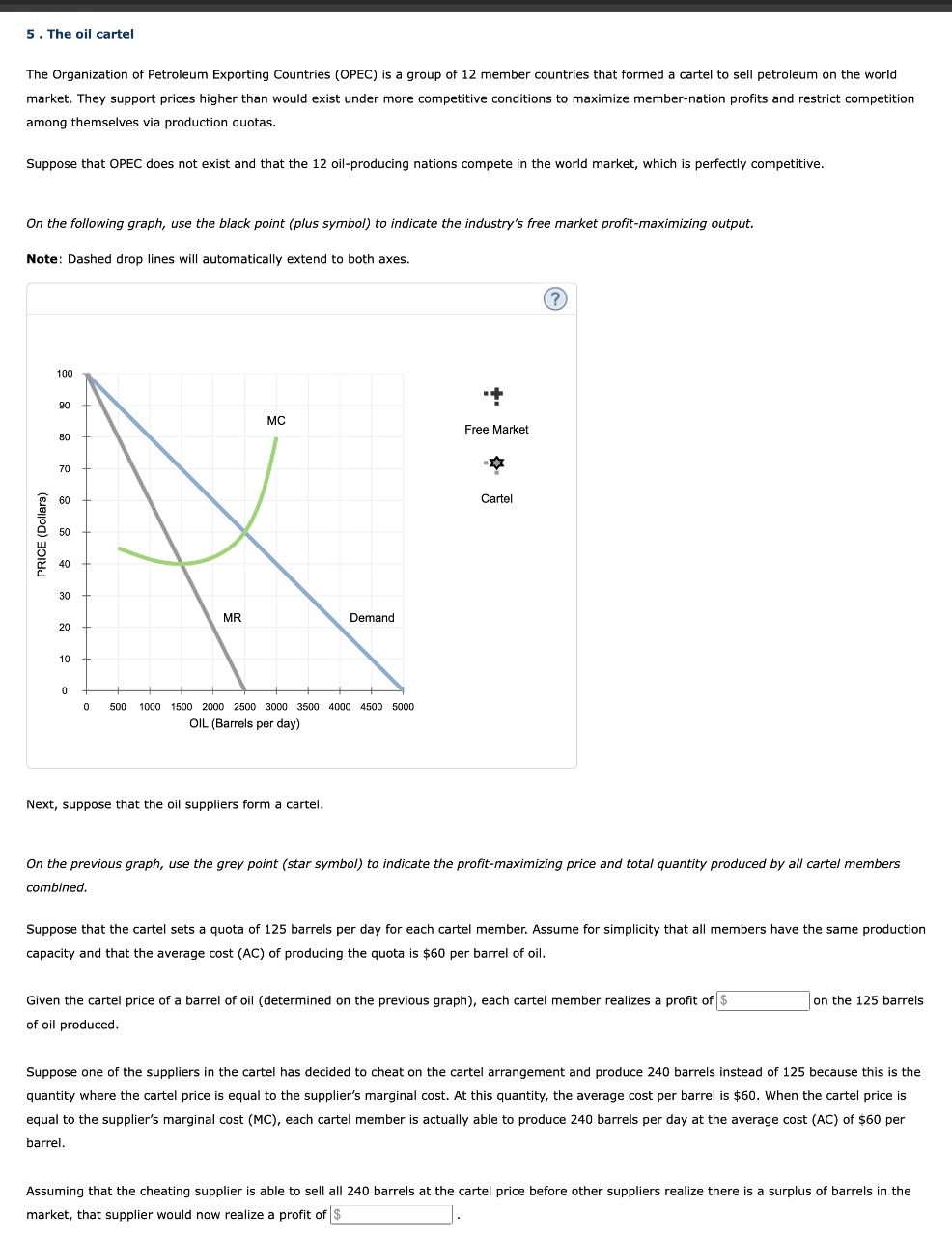

Transcribed Image Text:5. The oil cartel

The Organization of Petroleum Exporting Countries (OPEC) is a group of 12 member countries that formed a cartel to sell petroleum on the world

market. They support prices higher than would exist under more competitive conditions to maximize member-nation profits and restrict competition

among themselves via production quotas.

Suppose that OPEC does not exist and that the 12 oil-producing nations compete in the world market, which is perfectly competitive.

On the following graph, use the black point (plus symbol) to indicate the industry's free market profit-maximizing output.

Note: Dashed drop lines will automatically extend to both axes.

PRICE (Dollars)

100

90

80

70

60

50

40

30

20

10

0

MR

MC

Demand

0 500 1000 1500 2000 2500 3000 3500 4000 4500 5000

OIL (Barrels per day).

Next, suppose that the oil suppliers form a cartel.

܀ ܂

Free Market

Cartel

(?)

On the previous graph, use the grey point (star symbol) to indicate the profit-maximizing price and total quantity produced by all cartel members

combined.

Suppose that the cartel sets a quota of 125 barrels per day for each cartel member. Assume for simplicity that all members have the same production

capacity and that the average cost (AC) of producing the quota is $60 per barrel of oil.

Given the cartel price of a barrel of oil (determined on the previous graph), each cartel member realizes a profit of $

of oil produced.

on the 125 barrels

Suppose one of the suppliers in the cartel has decided to cheat on the cartel arrangement and produce 240 barrels instead of 125 because this is the

quantity where the cartel price is equal to the supplier's marginal cost. At this quantity, the average cost per barrel is $60. When the cartel price is

equal to the supplier's marginal cost (MC), each cartel member is actually able to produce 240 barrels per day at the average cost (AC) of $60 per

barrel.

Assuming that the cheating supplier is able to sell all 240 barrels at the cartel price before other suppliers realize there is a surplus of barrels in the

market, that supplier would now realize a profit of $

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 4 steps with 6 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Coke and Pepsi dominate the cola market. Suppose that the marginal cost of making cola is $2. Assume also that the demand for cola is given by the following table: Price $8 7 6 5 4 3 2 1 Quantity 5 cans 6 7 8 9 10 11 12 Suppose Coke and Pepsi both supply cola. They form a cartel and agree to cooperate on how much soda to produce. In this cartel case, how many bottles of cola would be sold? Type your answer...arrow_forward14. Aside from advertising, how can monopolisticallycompetitive firms increase demand for their products? 17. Would you expect the kinked demand curve to bemore extreme (like a right angle) or less extreme (like anormal demand curve) if each firm in the cartel producesa near-identical product like OPEC and petroleum?What if each firm produces a somewhat differentproduct? Explain your reasoning.arrow_forward4. Imagine a market with demand P = 420 – Q in each period. Two firms are thinking about colluding. They each have cost C(Qi) = 60Qi. If they cooperate and behave as a monopoly, then they have a marginal revenue curve, MRm = 420 – 2Q, and a marginal cost curve, MCm = 60. If they are in a cartel, then the firms will split the monopoly production and profits. If they compete, then they face MRi = 420 – 2Qi – Q-I and MCi = 60. a. If the firms stick to their agreement (cooperate), how much per-period profit do they each make? b. If they are not able to maintain their agreement (compete), what is their per-period profit? c. If one firm cheats on their agreement (deviate), how much does each firm make? Be sure to specify both the profit for the cheater and the firm cheated-on. d. Suppose the firms assume that their interaction will last forever (r = 1) and they share the common discount value R. What is the lowest value of R such that both firms are willing to continue with the cartel…arrow_forward

- 1arrow_forwardQuestion 35 (Table: Three-Country Oil Production) Refer to the table. Suppose that three countries are engaged in oil production. For simplicity, assume zero costs so that revenue equals profit. Assume that country A cheats on the cartel agreement by producing 200 more barrels than the other two countries. What is the resultant profit earned by country A? Market Price 6,000 Total Market Output 600 800 1,000 1,200 1,400 1,600 1,800 O 24,000 O 30,000 O 70,000 90 80 70 60 50 40 30arrow_forward3. Antitrust laws Cooperation among oligopolies runs counter to the public interest because it leads to underproduction and high prices. In an effort to bring resource allocation closer to the social optimum, public officials attempt to force oligopolies to compete instead of cooperating. Consider the following scenario: Suppose that two American investment banks negotiate a merger agreement because a financial crisis threatens to bankrupt both firms. This merger could potentially be stopped by a lawsuit brought by which of the following American institutions? O The Commerce Department O The Interior Department O The Defense Department O The Justice Departmentarrow_forward

- 5. Interpreting concentration ratios The following table shows the four-firm concentration ratios of various industries. Industry Computer and electronic parts Greeting cards Photo equipment and supplies Plastics and rubber product manufacturing Coffee and tea manufacturing Four-Firm Concentration Ratio: 19 80 78 10.5 52.5 Based on the data presented in the table, in which of the following industries are sales most concentrated among the four largest firms? Plastics and rubber product manufacturing Greeting cards O Computer and electronic parts Photo equipment and supplies O Coffee and tea manufacturingarrow_forward9. Antitrust laws Cooperation among oligopolies runs counter to the public interest because it leads to underproduction and high prices. In an effort to bring resource allocation closer to the social optimum, public officials attempt to force oligopolies to compete instead of cooperating. Consider the following scenario: Suppose that two American investment banks negotiate a merger agreement because a financial crisis threatens to bankrupt both firms. This merger could potentially be stopped by a lawsuit brought by which of the following American institutions? O The Defense Department O The Commerce Department O The Justice Department O The Interior Departmentarrow_forwardThe Competition Bureau in Canada wants to increase competition and reduce monopoly power. Thus it it worries about industry concentration in Canada. Let's assume that the Canadian halibut processing industry there are only two firms(duopoly). Under such a market structure, if one of the halibut processing firm increases its price, then the other firm in the halibut processing industry can: keep the price of its processed halibut constant and thus increase its market share. keep its price of its processed halibut constant and thus decrease its market share. decrease its price of its processed halibut and thus decrease its market share. try to achieve economies of scale. increase its price of its processed halibut and thus increase its market share.arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education