ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

thumb_up100%

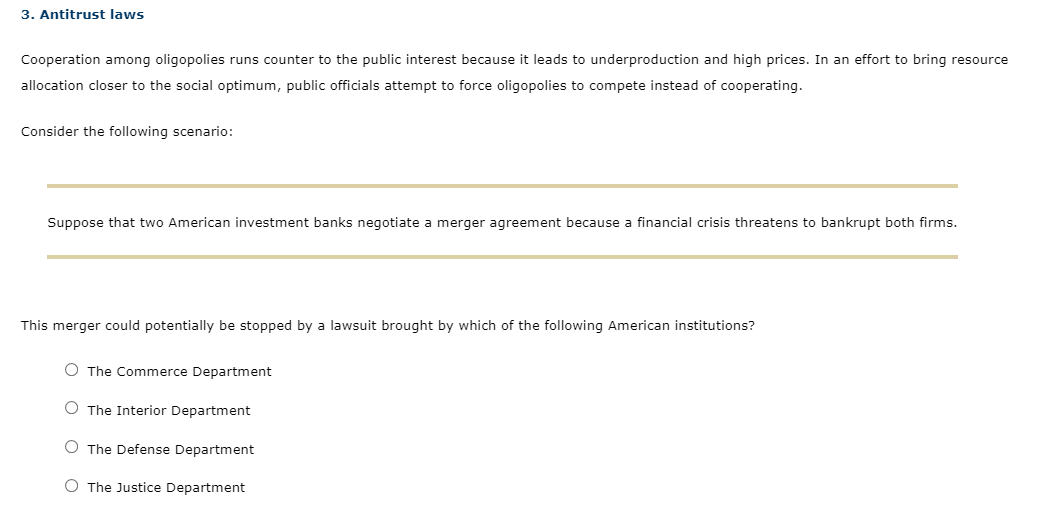

Transcribed Image Text:3. Antitrust laws

Cooperation among oligopolies runs counter to the public interest because it leads to underproduction and high prices. In an effort to bring resource

allocation closer to the social optimum, public officials attempt to force oligopolies to compete instead of cooperating.

Consider the following scenario:

Suppose that two American investment banks negotiate a merger agreement because a financial crisis threatens to bankrupt both firms.

This merger could potentially be stopped by a lawsuit brought by which of the following American institutions?

O The Commerce Department

O The Interior Department

O The Defense Department

O The Justice Department

Expert Solution

arrow_forward

Step 1

Antitrust laws are created by the government for the protection of the consumer from predatory practices of business and for ensuring fair competition.

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- 4) Which of the following companies is least likely to operate in an oligopoly? Burger King, which sells fast food Frontier, which provides Internet services AHF pharmacy Verizon, which provides cell phone coveragearrow_forwardSuppose that a small town has seven burger shops whose respective shares of the local hamburger market are (as percentages of all hamburgers sold): 18 percent, 24 percent, 20 percent, 11 percent, 10 percent, 9 percent, and 8 percent. The four-firm concentration ratio for the hamburger industry in this town is percent. (Enter your response as a whole number.) The Herfindahl index for the hamburger industry in this town is (Enter your response as a whole number.) Suppose the top three sellers combined to form a single firm. The four-firm concentration ratio would be percent. (Enter your response as a whole number.) Suppose the top three sellers combined to form a single firm. The Herfindahl index would be (Enter your response as a whole number.)arrow_forward8. Two firms, the only firms in the market, sell the same product and have the same marginal cost. They realise they would be better off if they didn't compete with each other. They enter an alternating offers bargaining game to decide how they will divide the monopoly profit, n. They have three periods to come to an agreement. If no agreement is reached after three periods, the firms will compete simultaneously in prices. The firms toss a coin to decide who makes the first offer in the bargaining game. Firm 1 wins and decides to go first. Each firm has a discount factor o. a) Draw the game tree. b) What is the subgame perfect equilibrium when 8 = 0.5? c) What is the equilibrium payoff for each firm? d) Was Firm 1 wise to opt to make the first offer? Explain your answer. %3Darrow_forward

- 4. Imagine a market with demand P = 420 – Q in each period. Two firms are thinking about colluding. They each have cost C(Qi) = 60Qi. If they cooperate and behave as a monopoly, then they have a marginal revenue curve, MRm = 420 – 2Q, and a marginal cost curve, MCm = 60. If they are in a cartel, then the firms will split the monopoly production and profits. If they compete, then they face MRi = 420 – 2Qi – Q-I and MCi = 60. a. If the firms stick to their agreement (cooperate), how much per-period profit do they each make? b. If they are not able to maintain their agreement (compete), what is their per-period profit? c. If one firm cheats on their agreement (deviate), how much does each firm make? Be sure to specify both the profit for the cheater and the firm cheated-on. d. Suppose the firms assume that their interaction will last forever (r = 1) and they share the common discount value R. What is the lowest value of R such that both firms are willing to continue with the cartel…arrow_forward1. What do we mean by market power in economics? What are some ways firms can attain market power? How can we, as economists, know when a firm has "too much" market power? Give an example of a firm you think has a lot of market power.2. Chapter 3 is all about game theory. Imagine you are in charge of pricing at a firm that has 20% market share in an industry where the leading firm has 50% market share. Imagine that the leader increases prices on their products. How do you think you would react? Why?arrow_forwardDiscuss how oligopoly market structure can help explain some of the decision-making processes by firms?arrow_forward

- 3. Breakdown of a cartel agreement Consider a town in which only two residents, Gregor and Haidy, own wells that produce water safe for drinking. Gregor and Haidy can pump and sell as much water as they want at no cost. For them, total revenue equals profit. The following table shows the town's demand schedule for water. Price (Dollars per gallon) 4.80 4.40 4.00 3.60 3.20 2.80 2.40 2.00 1.60 1.20 0.80 0.40 0 Quantity Demanded (Gallons of water) 0 35 70 105 140 175 210 245 280 315 350 385 420 Total Revenue (Dollars) 0 $154.00 $280.00 $378.00 $448.00 $490.00 $504.00 $490.00 $448.00 $378.00 $280.00 $154.00 0 Suppose Gregor and Haidy form a cartel and behave as a monopolist. The profit-maximizing price is $ output is S per gallon, and the total gallons. As part of their cartel agreement, Gregor and Haidy agree to split production equally. Therefore, Gregor's profit is , and Haidy's profit is $ Suppose that Gregor and Haidy have been successfully operating as a cartel. They each charge the…arrow_forward1. In a homogenous good Bertrand duopoly model with complete and symmetric information the Bertrand paradox arises because the firms compete using _________ as their choice variable. 2. Suppose there is an industry with nine firms where two of them have a market share of 0.2, three of them have a market share of 0.1 and the remaining firms have a market share of 0.075. The 4 firm concentration ratio is______. (two decimal accuracy)arrow_forward2. Consider the following game: Soapy Inc. and Suddies Inc. are the only producers of soap powder. They collude and agree to share the market equally. If neither firm cheats on the agreement, each makes $1 million profit. If either firm cheats, the cheat makes a profit of $1.5 million, while the complier incurs a loss of $0.5 million. If both cheat, they break even. Neither firm can monitor the other's actions. a) Construct the payoff matrix. b) What is the dominant strategy? c) What is the nash equilibrium for this game?arrow_forward

- 8. Two firms, the only firms in the market, sell the same product and have the same marginal cost. They realise they would be better off if they didn't compete with each other. They enter an alternating offers bargaining game to decide how they will divide the monopoly profit, n. They have three periods to come to an agreement. If no agreement is reached after three periods, the firms will compete simultaneously in prices. The firms toss a coin to decide who makes the first offer in the bargaining game. Firm 1 wins and decides to go first. Each firm has a discount factor o. a) Draw the game tree. b) What is the subgame perfect equilibrium when o = 0.5? c) What is the equilibrium payoff for each firm? d) Was Firm 1 wise to opt to make the first offer? Explain your answer.arrow_forward11. Suppose there is a duopoly of two identical firms, A and B, facing a market inverse demand of P = 140 – 0.5Q, and cost functions of CA = 20QA and Cg = 20QB respectively. a. Find the Cournot-Nash equilibrium and profit for each firm. b. Suppose that A acts as the leader in a Stackelberg model and B responds. What are the respective quantities and profits of each firm now? Is it advantageous to move first? c. If the firms were able to collude, how much additional profit could they earn if they switch from simple single pricing to perfect price discrimination? d. Graph and label equilibria on the inverse demand.arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education