Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

Transcribed Image Text:5.

6.

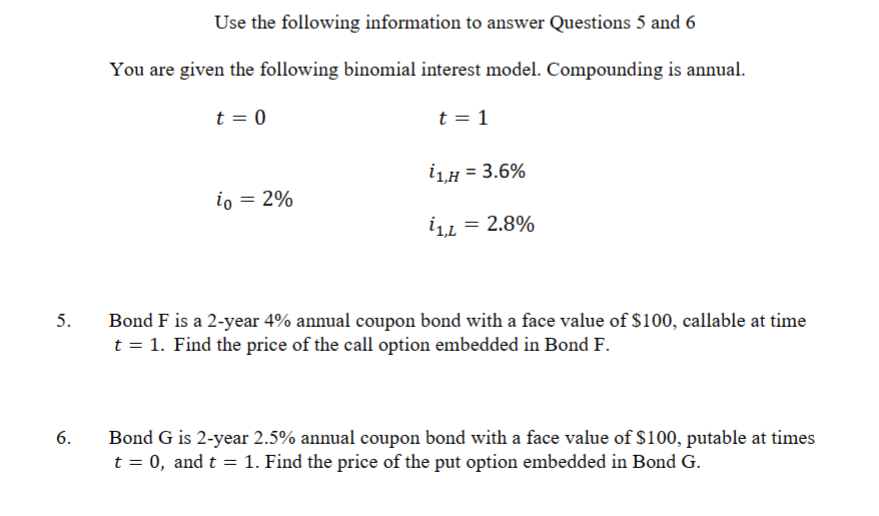

Use the following information to answer Questions 5 and 6

You are given the following binomial interest model. Compounding is annual.

t = 0

t = 1

i1,H = 3.6%

io = 2%

ίο

i1,L = 2.8%

Bond F is a 2-year 4% annual coupon bond with a face value of $100, callable at time

t = 1. Find the price of the call option embedded in Bond F.

Bond G is 2-year 2.5% annual coupon bond with a face value of $100, putable at times

t = 0, and t = 1. Find the price of the put option embedded in Bond G.

SAVE

AI-Generated Solution

info

AI-generated content may present inaccurate or offensive content that does not represent bartleby’s views.

Unlock instant AI solutions

Tap the button

to generate a solution

to generate a solution

Click the button to generate

a solution

a solution

Knowledge Booster

Similar questions

- Using the expectations hypothesis theory for the term structure of interest rates, determine the expected return for securities with maturities of two, three, and four years based on the following data. Note: Input your answers as a percent rounded to 2 decimal places. 1-year T-bill at beginning of year 1 1-year T-bill at beginning of year 21 1-year T-bill at beginning of year 3 1-year T-bill at beginning of year 4 2-year security 3-year security 4-year security Expected Return % % % Interest Rate 7% 9% 10% 12%arrow_forward1. How to calculate the value of a 6 year 2% coupon bond with semiannual payments, 1000 par. Expected return is the risk free rate of 3%. 2. Price a 5 year 4% semiannual coupon bond if the yield to maturity is 6% (write the price as if par is 100, use 5 decimal places)arrow_forwardPlease answer the question in the image attached below.arrow_forward

- 9. Interest Rate Risk. Suppose that you are a fixed income portfolio manager at Bourbon Street Capital. You have the following bonds issued by Royal, Inc. and Chartres, LLC in your portfolio and you want to understand the risk profile of your portfolio. Given that both bonds pay semiannual coupons, answer the following questions. (Remember to convert your answer to units of full years.) Coupon Yield to maturity Maturity (years) Royal, Inc. Chartres, LLC. Bond A Bond B 9% 8% 5 $100.00 $104.055 8% 8% 2 Par $100.00 Price $100.00 (a) What is the DV01 (at current prices) for bonds A and B? (b) What are the Macaulay Durations (at current prices) for the two bonds? (c) What are the modified durations for the two bonds? (d) What is the convexity of the two bonds?arrow_forwardIf possible, please calculate using excel and show formulas. The spot interest rates in the following downward-sloping term structure are: r1 = 4.6%, r2 = 4.4%, r3 = 4.2%, and r4 = 4.0%, r5=2%. Assume face value is $1,000. Calculate bond prices of a 5% coupon bond.arrow_forwardUsing the expectations hypothesis theory for the term structure of interest rates, determine the expected return for securities with maturities of two, three, and four years based on the following data. (Input your answers as a percent rounded to 2 decimal places.) 1-year T-bill at beginning of year 1 1-year T-bill at beginning of year 2 1-year T-bill at beginning of year 3 1-year T-bill at beginning of year 4 2-year security 3-year security 4-year security Expected Return % % % Interest Rate 61 98 7% 108arrow_forward

- Unlike the coupon interest rate, which is fixed, a bond's yield varies from day to day depending on market conditions. To be most useful, it should give us an estimate of the rate of return an investor would earn if that investor purchased the bond today and held it for its remaining life. There are three different yield calculations: Current yield, yield to maturity, and yield to call. A bond's current yield is calculated as the annual interest payment divided by the current price. Unlike the yield to maturity or the yield to call, it does not represent the actual return that investors should expect because it does not account for the capital gain or loss that will be realized if the bond is held until it matures or is called. This yield was popular before calculators and computers came along because it was easy to calculate; however, because it can be misleading, the yield to maturity and yield to call are more relevant. The yield to maturity (YTM) is the rate of return earned on a…arrow_forward2. You are holding a 3-year bond with coupon rate 10%. Coupon payments are annual and par values are 100. Spot rates are: r₁ = 5%, r₂ 6%, r3 = 6.5%. (a) Determine as many forward rates as you can based on the spot rates above. (b) You would like to get a guaranteed 3-year return on your coupon bond. Explain how this can be achieved using forward rates. Which forward rates should you use? What is your guaranteed 3-year return?arrow_forward13. Consider a coupon bond with coupon payment=4.25, M=100, and n=2. Suppose ?1 = 4% and ?2 = 4.24%. Consider a forward contract for the delivery of the coupon bond in one period from today. Calculate the forward price using the following two approaches: 1) use the forward rate to price the forward contract; 2) use the cost of carry approach: spot-forward parity adjusted for the coupons.arrow_forward

- In calculating the current price of a bond paying semiannual coupons, one needs to O use double the number of years for the number of payments made. O use the semiannual coupon. O use the semiannual rate as the discount rate. O All of the above needs to be done.arrow_forward3. Interest rate swap. Consider a portfolio of floating-rate bonds that all mature in three years. What is the fixed coupon rate for a fairly priced fixed-for-floating interest rate swap given the following discount factors? Years 2. 0.,95 06'0 0.86arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education