Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

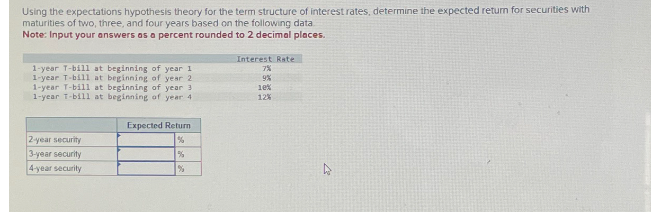

Transcribed Image Text:Using the expectations hypothesis theory for the term structure of interest rates, determine the expected return for securities with

maturities of two, three, and four years based on the following data.

Note: Input your answers as a percent rounded to 2 decimal places.

1-year T-bill at beginning of year 1

1-year T-bill at beginning of year 21

1-year T-bill at beginning of year 3

1-year T-bill at beginning of year 4

2-year security

3-year security

4-year security

Expected Return

%

%

%

Interest Rate

7%

9%

10%

12%

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 3 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- Following bond if interest (coupon) is paid annually? (Round to two decimal places.) - X Years to Data Table pon Rate Maturity 5% 15 following bond if interest (coupon) is (Click on the following icon in order to copy its contents into a spreadsheet) Yiold to Maturity Years to Years to Par Value $1,000.00 $1,000,00 $5,000.00 $5,000,00 Coupon Rate 5% 9% 8% 11% Maturity 15 25 20 20 Price $900 00 $1,000.00 $4,140.00 $7,110.00 pon Rate Maturity 9% 25 Print Donearrow_forwardYield to maturity The bond shown in the following table pays interest annually. (Click on the icon here in order to copy the contents of the data table below into a spreadsheet.) Par value $100 Coupon interest rate 14% Years to maturity 4 Current value $100 a. Calculate the yield to maturity (YTM) for the bond. b. What relationship exists between the coupon interest rate and yield to maturity and the par value and market value of a bond? Explain. a. The yield to maturity (YTM) for the bond is%. (Round to two decimal places.)arrow_forwardplease show hoe to complete using excel formulasarrow_forward

- Give typing answer with explanation and conclusionarrow_forwardData table 不 The following table summarizes prices of various default-free zero-coupon bonds (expressed as a percentage of face value): a. Compute the yield to maturity for each bond. b. Plot the zero-coupon yield curve (for the first five years). c. Is the yield curve upward sloping, downward sloping, or flat? a. Compute the yield to maturity for each bond. The yield on the 1-year bond is ☐ %. (Round to two decimal places.) (Click on the following icon in order to copy its contents into a spreadsheet.) Maturity (years) Price (per $100 face value) 1 $95.42 2 3 4 5 $90.99 $86.47 $81.58 $76.46 Print Donearrow_forwardQuantitative Problem: An analyst evaluating securities has obtained the following information. The real rate of interest is 2.9% and is expected to remain constant for the next 5 years. Inflation is expected to be 2.2% next year, 3.2% the following year, 4.2% the third year, and 5.2% every year thereafter. The maturity risk premium is estimated to be 0.1 x (t-1)%, where t = number of years to maturity. The liquidity premium on relevant 5-year securities is 0.5% and the default risk premium on relevant 5-year securities is 1%. a. What is the yield on a 1-year T-bill? Do not round intermediate calculations. Round your answer to one decimal place. % b. What is the yield on a 5-year T-bond? Do not round intermediate calculations. Round your answer to one decimal place. % c. What is the yield on a 5-year corporate bond? Do not round intermediate calculations. Round your answer to one decimal place. %arrow_forward

- Suppose we observe the following rates: 1R1 = 6.7, 1R2 = 7.4, and E(2r1) = 6.7. If the liquidity premium theory of the term structure of interest rates holds, what is the liquidity premium for year 2? Please step by step.arrow_forward1. Pricing a bond in the secondary market: For each question, use the three methods we learned in class: plug in the values in the formula, handwrite the keys you enter in the Financial Calculator, and use Excel (formula and arguments). Use the Table below for each answer. a. Find the price of a 10-year 10% coupon (paid semiannually). The current yield to maturity is 5%. b. Find the price of a 10-year 5 % coupon (paid semiannually). The current yield to maturity is 10%. c. Based on your answers, discuss the relationship between coupon rate, yield to maturity, and bond price. FORMULA (Plug in the corresponding values in the formula below) 2 Financial Calculator (Indicate the keys you enter and write the answer) 3 Excel (Write the function and arguments in Excel)arrow_forwardTreasury securities that matures in 8 years currently have a rate of 11.9 %. Inflation is expected to be 5 percent each of the next 3 years and 6 percent each year after the 3rd year. The maturity risk premium is estimated to be 0.2 (t-1). Where t is the zero. The real risk rate is assumened to be tconsint over time what is the risk free rate of interest. a. 6. 28 b. 4.88 C. 2.51 D. 4.68arrow_forward

- An investor considers the purchase of a 2-year bond with a 5% coupon rate, with interest paid annually. Assuming the sequence of spot rates shown below, the price of the bond is closest to: Time-to-Maturity Spot Rates 1 year 3% 2 years 4% A. $101.93 B. $102.85 C. $105.81 D. $103.85arrow_forwardThe pure rate of return is 1.5%. Inflation is expected to be 2% this year and 3% during the next two years. Assume that the maturity risk premium for 2 and 3 years security are 1.2% and 1.3% respectively. What is the yield on 2 year Treasury Securities? Group of answer choices 5.47% 5.20% 5.37% 5.30% Please show the steps.arrow_forwardDiscuss the overarching idea of Asset Liability Management and its key objectives. How does the process of Gap Analysis support Asset Liability Management?arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education