Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

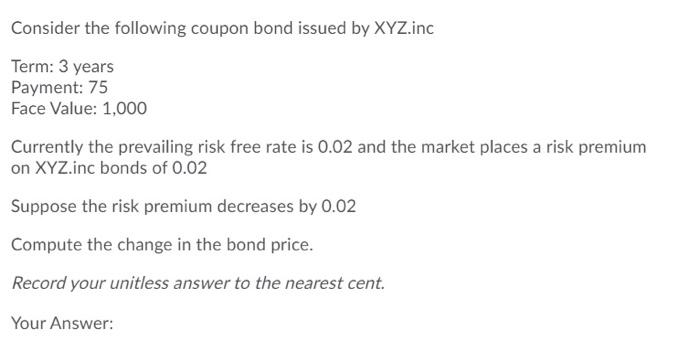

Transcribed Image Text:Consider the following coupon bond issued by XYZ.inc

Term: 3 years

Payment: 75

Face Value: 1,000

Currently the prevailing risk free rate is 0.02 and the market places a risk premium

on XYZ.inc bonds of 0.02

Suppose the risk premium decreases by 0.02

Compute the change in the bond price.

Record your unitless answer to the nearest cent.

Your Answer:

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- Assume the zero-coupon yields on default-free securities are as summarized in the following table: (Click on the following icon in order to copy its contents into a spreadsheet.) Maturity (years) Zero-coupon YTM 1 6.70% 2 7.10% 3 7.30% 4 7.70% 5 8.00% What is the price of a three-year, default-free security with a face value of $1,000 and an annual coupon rate of 5%? What is the yield to maturity for this bond? What is the price of a three-year, default-free security with a face value of $1,000 and an annual coupon rate of 5%? The price is $ (Round to the nearest cent.)arrow_forwardA. Calculate the yield spread of the following floating rate bond: • Annual coupon rate = reference rate + 200 basis points• initial reference rate (annual) = 4%• The bond has a 10-year of term to maturity• Assume the bond’s par value = USD1000• The price of the bond = USD1,032.84 B. Suppose the new reference rate is decreased to 3% two years after the bond is issued. What is the price of the bond then?arrow_forwardThe current zero-coupon yield curve for risk-free bonds is as follows What is the price per $100 face value of a four-year, zero-coupon, risk-free bond? The price per $100 face value of the four-year, zero-coupon, risk-free bond is $_______(Round to the nearest cent.)arrow_forward

- The one-year spot rate z1 = 5% and the forward price for a one-year zero-coupon bond beginning in one year is 0.9346. Find the spot price (zero price) of a two-year zero-coupon bond.arrow_forwardAssume that the real risk free rate is 2% and the average expected inflation rate is 3% for each future year. The default risk premium and the liquidity premium for bond x are each 1% and the applicable Maturity Risk premium is 2% what is bond x’s interest rate. Round to 2 decimal placesarrow_forwardSuppose the interest rate on a 1-year T-bond is 5.00% and that on a 2-year T-bond is 6.40%. Assume that the pure expectations theory is NOT valid, and the MRP is zero for a 1-year T-bond but 0.40% for a 2-year bond. What is the yield on a 1-year T-bond expected to be one year from now?arrow_forward

- Unlike the coupon interest rate, which is fixed, a bond's yield varies from day to day depending on market conditions. To be most useful, it should give us an estimate of the rate of return an investor would earn if that investor purchased the bond today and held it for its remaining life. There are three different yield calculations: Current yield, yield to maturity, and yield to call. A bond's current yield is calculated as the annual interest payment divided by the current price. Unlike the yield to maturity or the yield to call, it does not represent the actual return that investors should expect because it does not account for the capital gain or loss that will be realized if the bond is held until it matures or is called. This yield was popular before calculators and computers came along because it was easy to calculate; however, because it can be misleading, the yield to maturity and yield to call are more relevant. The yield to maturity (YTM) is the rate of return earned on a…arrow_forward13. Consider a coupon bond with coupon payment=4.25, M=100, and n=2. Suppose ?1 = 4% and ?2 = 4.24%. Consider a forward contract for the delivery of the coupon bond in one period from today. Calculate the forward price using the following two approaches: 1) use the forward rate to price the forward contract; 2) use the cost of carry approach: spot-forward parity adjusted for the coupons.arrow_forwardIn calculating the current price of a bond paying semiannual coupons, one needs to O use double the number of years for the number of payments made. O use the semiannual coupon. O use the semiannual rate as the discount rate. O All of the above needs to be done.arrow_forward

- Consider the zero coupon Treasury bond yield curve. Suppose a 1 year bond has a yield of 2.13%. The yield curve slopes downwards between maturities of 1 year and 3 years, and then slopes upwards. Which of the following must be true? Group of answer choices A) The yield of a zero coupon bond with maturity 5 years is higher than 2.13%. B) A 1 year positive coupon bond must have a lower price than the zero coupon bond with the same maturity. C) Bond purchasers believe the Fed will decrease rates in the short run, and then increase them in the long run. D) The economy will be in a recession within 2 years. E) C and D.arrow_forwardUse Macauly's Duration Price Approximation formula for this. Before a change in interest rates, your bond has the following characteristics: present value of $5,557.56, Duration of 3.69 years with market interest rates of 5%. Calculate the percentage change in the bond's price if market rates fall to 4.85%. Be sure to include the negative sign IF you think the price goes down. Iarrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education