ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

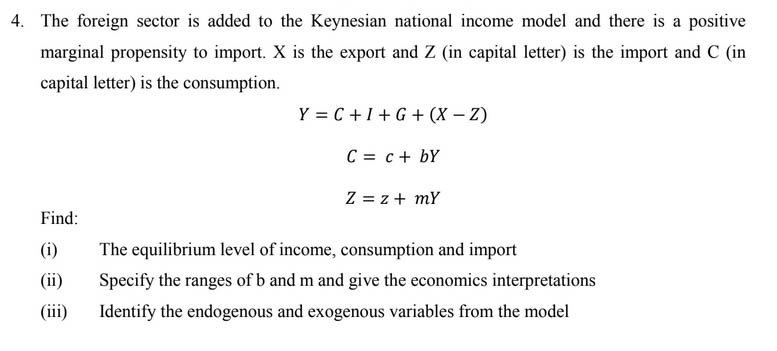

Transcribed Image Text:4. The foreign sector is added to the Keynesian national income model and there is a positive

marginal propensity to import. X is the export and Z (in capital letter) is the import and C (in

capital letter) is the consumption.

Y = C+1+G+ (X – Z)

C = c+ bY

Z = z + mY

Find:

(i)

The equilibrium level of income, consumption and import

(ii)

Specify the ranges of b and m and give the economics interpretations

(iii)

Identify the endogenous and exogenous variables from the model

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- In the Keynesian cross model, assume that the consumption function is given by C = 20 + 0.8(Y- T). Planned investment is 200; government purchases and taxes are both 400. There is no foreign trade. An economist has claimed that the full employment level of output is 2,400. How much should the government expenditure or taxes rise or fall to achieve full employment?arrow_forward• Assuming that there is no government spending or trade, an economy's GDP is the sum of domestic consumption C and investment I, ie. Y = C+ 1 of • Assume that I is unaffected by GDP • Assume the consumption function is C = co + cY • In any equilibrium aggregate demand, AD must be equal to Y, GDP. Given this model, which of the following statements is correct? Select one or more: O a. The aggregate demand equation is given by AD = Co + CY + I %3D O b. C is equal to autonomous consumption. O c. if c is a number between 0 and 1, and I+Co >0 then the aggregate demand equation is a straight line that must intersect the 45 degree line at some point. O d. In a demand-driven economy the AD curve is a vertical line Oe. In a demand-driven economy demand is equal to supply in equilibrium Of. In a supply-driven economy demand is equal to supply in equilibrium g. In a demand-driven economy, supply creates its own demand Oh. If the economy above is a demand-driven economy, then the equilibrium…arrow_forwardConsider the basic Macroeconomic model involving: Private sector consumption: C = co+c1(Y-T); Y = GDP, T = Taxes Tax function: T = to+t1Y Business sector investment: I = io+i2r, r=interest rate Government spending: G = Go Exports: X = xo+x1x; x = Exchange rate of the dollar Imports: M = mo+m1Y+m2x; x = Exchange rate (a) Identify and explain the parameters: co, t1, i2, and m2. (b) Solve this model for the equilibrium GDP (Y*).arrow_forward

- Suppose country A has the following system of taxes/transfers: ANAL (a) Income 200: Taxed at 40%. In this country, we assume that everyone receives 5 per hour as wages. A worker chooses how many hours she wants to work. Her preferences over aggregate consumption, c, and 41 abor, I, are represented by the following utility function U(c, 1) =c+0ln(31-1) where 0 is a parameter reflecting drudgery of work (i.e. how painful the work is). Assuming 0 = 60 for the worker and given the system of axes/transfers, what is her optimal choice of labor? A 1=21 B 1 20 C 1* = 19 D 1*=22 48 55arrow_forwardQuestion 2 Refer to the information provided in Figure 23.9 below to answer the question(s) that follow. Aggregate expenditures ($ millions) 225 200 175 150 45° AE 100 200 300 Aggregate output ($ millions) Figure 23.9 a) Refer to Figure 23.9. Write the equation for the aggregate expenditure function (AE). Show your work. b) Refer to Figure 23.9. What is the equilibrium level of output in this economy? State the equilibrium condition used to determine this. c) Explain the forces that maintain/drive the economy to this equilibrium by considering what will happen at the following two levels of output, $300 million and $100 million. You will need to discuss changes in investment through unplanned inventories and the response of output. d) Refer to Figure 23.9. How will equilibrium aggregate expenditure and equilibrium aggregate output change as a result of a decrease in investment by $20 million? e)The interest rate is an exogenous factor that effects the level of investment in an economy.…arrow_forward(1)The following macroeconomic model describes the economy of Sunderland. 1. Y= C +I + G + NX 2. C = 220 + 0.63 Y 3. 1 = 1000- 2000R 4. G = Go 5. NX = 525-0.10Y-50OR 6. M (0.1583Y-1000R)P (a)ls it a fair characterization to refer to equation #2 as a "simple" consumption function? Explain. (b)Derive the expression for equilibrium real output, Y, for this economy. Note: In your final expression for Y, restrict coefficient values to three decimal points. (c) Suppose government spending is 1200 , money supply by the Central Bank is 900 and the price level is 1, find the value of GDP (Y) and equilibrium interest rate (R) for Sunderland. Income Identity Consumption function Investment function Government Expenditure Net export function Money market equilibrium (2)The questions in this section are related to the macroeconomic model of Sunderland. (a)The expression you are asked to derive in question #1b can be considered an aggregate demand curve. Do you agree? Explain your answer. (b)Sketch…arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education