ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

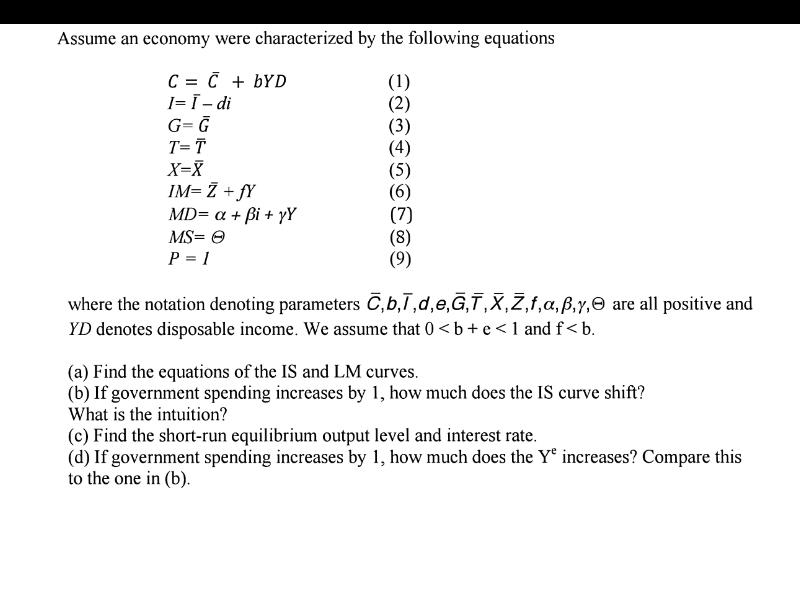

Transcribed Image Text:Assume an economy were characterized by the following equations

C = C + bYD

I=Ī - di

G=G

T=T

X=X

IM= Z +fY

MD= a + Bi+yY

MS=Ⓒ

P = 1

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

(9)

where the notation denoting parameters C,b,1,d,e,G,T,X,Z,f,a, ß,y, are all positive and

YD denotes disposable income. We assume that 0 <b+e<1 and f<b.

(a) Find the equations of the IS and LM curves.

(b) If government spending increases by 1, how much does the IS curve shift?

What is the intuition?

(c) Find the short-run equilibrium output level and interest rate.

(d) If government spending increases by 1, how much does the Ye increases? Compare this

to the one in (b).

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 6 steps with 6 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Please answer to 2 decimal placesarrow_forwardQuestion: Suppose that the marginal cost of extracting a non-renewable natural resource is MXC(Q) = 10 and the marginal beneÖt of using the resource are MB(Q) = 90Q. In the context of a static model, address the following question: Calculate the efficient value of Q if the total stock of the natural resource is Q = 50: Provide a graphical representation of the solution. My Note: This is my first time resubmitting, I was told to confirm that MXC(Q) =10 is the correct form of the Marginal cost of extraction to answer this question correctly. I'm not sure but this is the way my professor asked his question.arrow_forwardFor a income determination model Y = C +I + G, C = Co + bY d, I = Io + aYd, Yd = Y – T, T = To +tY, G = Go, 0 < a, b, t < 1, find the equilibrium level of income. Find the multipliers for each input.arrow_forward

- I want to check if I am going in the right direction with my math could I get feedback or guidance for the next partarrow_forwardAssume that the production function for a country is given by Y=√K and annual investment is given by the function I=γ×YI where γ=0.280, and that the yearly depreciation rate is 4.67%. Suppose that this year, the output in the country is 1, and a neighbor country's output is 50% higher. Calculate the time it would take for the country's output to catch up with its neighbor's output. Assume the neighbor country's economy is neither growing nor shrinking.arrow_forward51) In the absence of technological progress, we know with certainty that an decrease in the saving rate will cause which of the following? A) decrease steady state consumption B) increase steady state consumption C) have no effect on steady state consumption D) decrease steady state consumption only if the decrease in saving exceeds the increase in depreciation E) decrease steady state consumption only if the decrease in saving is less than the decrease in depreciation 52) As an economy adjusts to an decrease in the saving rate, we would expect output per worker A) to decrease at a constant rate and continue decreasing at that rate in the steady state. B) to decrease at a permanently higher rate. C) to increase at a permanently higher rate. D) to return to its original level. E) none of the above 53) Suppose the following situation exists for an economy: Kt+1/N t/N. Given this information, we know that A) saving per worker equals depreciation per worker…arrow_forward

- The formula for economic impact is I(r)=(A)/1-r The formula for impact change is ∆I= I'(r)*∆r The formula for percentage change is g(r)=(r)/1-rarrow_forwardWhy is consumption spending insufficient to explain economic growth and rising standards of living?arrow_forwardI need help with this question pleasearrow_forward

- a) A planner in a small, open economy has a utility function U = x1X2 and production takes place according to the production functions Y1 = 10L, – 0.5L Y2 = 10L2 – L The world prices of the goods are p1 10 and p2 5. The total amount of labour %| %3D available in the economy is 5 units. (i) Formulate the Lagrange equation. (ii) Write down the Karush-Khun-Tucker conditions. (iii) Determine a possible solution.arrow_forwardGiven a closed economy where there is no public sector. Production in the economy can be described with the following production function: Y = F (K, AL) = Kα(AL)1−α where Y is the productive capacity of the economy, K is the capital stock, L is the labor force, and A is knowledge. Think of AL as a single factor of production where knowledge and the amount of labor are multiplied together. Let's call the multiplier (ie AL) the efficiency of labor. Given that A = 1.5 and saving is a fixed rate of the production, or s = 33%. The capital stock shrinks by 3% per year, while the population grows is nobody Finally, α = 0.4. Answer the following questions based on the above criteria. (a) Show mathematically that the marginal productivity of labor and capital is positive but diminishing. Explain in words and with a picture what the term positive but diminishing marginal productivity means. (b) Show mathematically that saving and investment are equivalent in a closed economy (c) Show…arrow_forwardUse the attached graph .. which of the following can cause the relationship shown between MSC and MPC? a) an increase in cases of asthma due to pollution b) a decrease in financial instability from unlawful investing c) a increase in investment to support educational funding. d) a decrease in air pollution caused by a nuclear energy plant e)an increase in research and development funding of a productarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education