ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

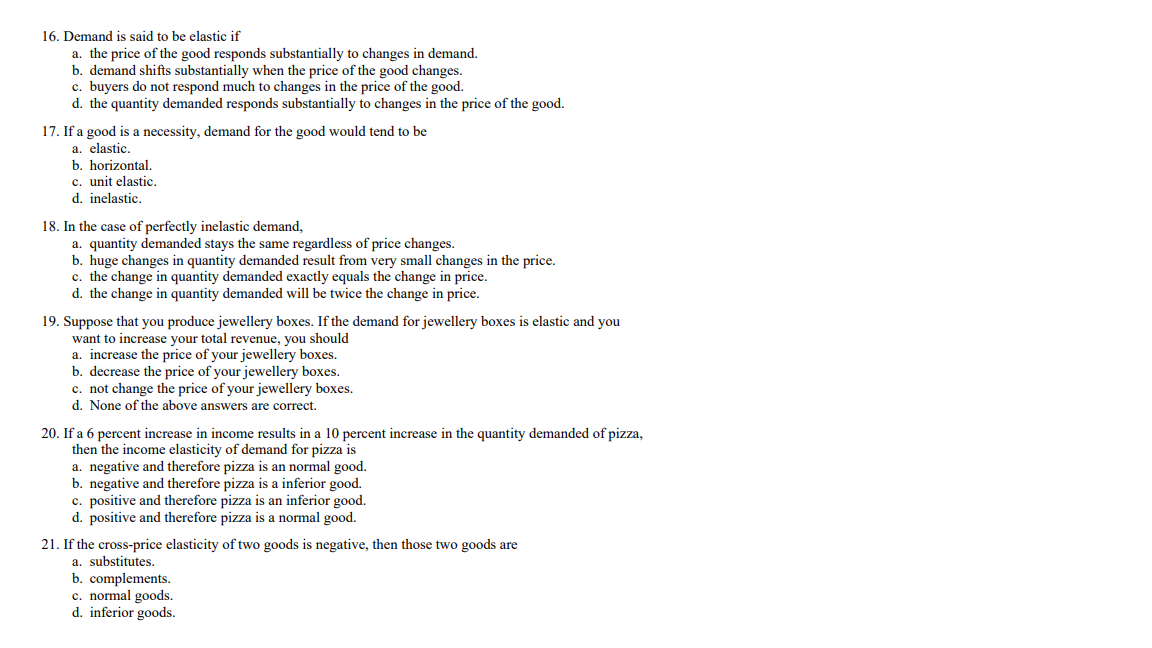

Transcribed Image Text:16. Demand is said to be elastic if

a. the price of the good responds substantially to changes in demand.

b. demand shifts substantially when the price of the good changes.

c. buyers do not respond much to changes in the price of the good.

d. the quantity demanded responds substantially to changes in the price of the good.

17. If a good is a necessity, demand for the good would tend to be

a. elastic.

b. horizontal.

c. unit elastic.

d. inelastic.

18. In the case of perfectly inelastic demand,

a. quantity demanded stays the same regardless of price changes.

b. huge changes in quantity demanded result from very small changes in the price.

c. the change in quantity demanded exactly equals the change in price.

d. the change in quantity demanded will be twice the change in price.

19. Suppose that you produce jewellery boxes. If the demand for jewellery boxes is elastic and you

want to increase your total revenue, you should

a. increase the price of your jewellery boxes.

b. decrease the price of your jewellery boxes.

c. not change the price of your jewellery boxes.

d. None of the above answers are correct.

20. If a 6 percent increase in income results na 10 percent increase in the quantity demanded of pizza,

then the income elasticity of demand for pizza is

a. negative and therefore pizza is an normal good.

b. negative and therefore pizza is a inferior good.

c. positive and therefore pizza is an inferior good.

d. positive and therefore pizza is a normal good.

21. If the cross-price elasticity of two goods is negative, then those two goods are

a. substitutes.

b. complements.

c. normal goods.

d. inferior goods.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Consider the supply of coal. What would make the supply of coal more elastic? The supply of coal would become more elastic if A. The time horizon becomes longer. B. It becomes a larger portion of a consumer's budget C. more substitutes were available. D. it were more of a luxury.arrow_forwarda. Explain what “cross-elasticity of demand” is. b. What is a “substitute good”? Give an example. Does it have a positive or negative cross-elasticity of demand?arrow_forward1. The price of a good rises from $6 to $8. Thus, the quantity demanded of that good falls from 150 to 75 units. Using the point-slope formula, calculate the Price Elasticity of Demand. Note: You’ll use this answer to help you with Question 2 & 3 (coming up next). A. -1.50 B. -0.66 C. -2 D. -0.04 E. -25 F. -1 2. Given your response in Question 1, classify the coefficient of the Price Elasticity of Demand. A. Elastic B. Inelastic C. Perfectly Elastic D. Perfectly Inelastic E. Unit Elastic 3. Which of the following statements is the best interpretation of the coefficient of the Price Elasticity of Demand in Question 1? A. There will be a 0.66 percent decrease in the Quantity Demanded. B. A 1 percent increase in the Price of a good corresponds to a 0.66 percent decrease in the Quantity Demanded for that good. C. A 1 percent increase in the Price of a good corresponds to a 1.55 percent increase in the Quantity Demanded for that good. D. Given the Price…arrow_forward

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education