Videos

The City of Lynnwood was recently incorporated and had the following transactions for the fiscal year ended December 31.

- 1. The city council adopted a General Fund budget for the fiscal year. Revenues were estimated at $2,000,000 and appropriations were $1,990,000.

- 2. Property taxes in the amount of $1,940,000 were levied. It is estimated that $9,000 of the taxes levied will be uncollectible.

- 3. A General Fund transfer of $25,000 in cash and $300,000 in equipment (with

accumulated depreciation of $65,000) was made to establish a central duplicating internal service fund. - 4. A citizen of Lynnwood donated marketable securities with a fair value of $800,000. The donated resources are to be maintained in perpetuity with the city using the revenue generated by the donation to finance an afterschool program for children, which is sponsored by the culture and recreation function. Revenue earned and received as of December 31 was $40,000.

- 5. The city’s utility fund billed the city’s General Fund $125,000 for water and sewage services. As of December 31, the General Fund had paid $124,000 of the amount billed.

- 6. The central duplicating fund purchased $4,500 in supplies.

- 7. Cash collections recorded by the general government function during the year were as follows:

- 8. During the year, the internal service fund billed the city’s general government function $15,700 for duplicating services and it billed the city’s utility fund $8,100 for services.

- 9. The city council decided to build a city hall at an estimated cost of $5,000,000. To finance the construction, 6 percent bonds were sold at the face value of $5,000,000. A contract for $4,500,000 has been signed for the project; however, no expenditures have been incurred as of December 31.

- 10. The general government function issued a purchase order for $32,000 for computer equipment. When the equipment was received, a voucher for $31,900 was approved for payment and payment was made.

Required

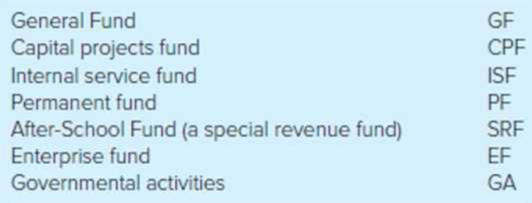

Prepare all journal entries to properly record each transaction for the fiscal year ended December 31. Use the following funds and government-wide activities, as necessary:

Each

Your answer sheet should be organized as follows:

Prepare necessary journal entries to properly record each transaction for the fiscal year ended December 31.

Explanation of Solution

Government-wide financial statement: This statement provides a combined summary of the net position and the changes in the net position of the government.

Fund financial statement: The fund financial statement provides detail financial information on the governmental, proprietary and fiduciary activities of the primary government.

Prepare necessary journal entries to properly record each transaction for the fiscal year ended December 31.

| Transaction Number | Fund or Activity | Account Title | Debit ($) | Credit ($) |

| 1. | GF | Estimated Revenues | 2,000,000 | |

| Appropriations | 1,990,000 | |||

| Budgetary fund balance | 10,000 | |||

| (To record the general fund receipt) | ||||

| 2. | GF | Taxes receivable-current | 1,940,000 | |

| Allowance for uncollectible current taxes | 9,000 | |||

| Revenues | 1,931,000 | |||

| (To record the property tax levy and uncollectible portion) | ||||

| GA | Taxes receivable- Current | 1,940,000 | ||

| Allowance for uncollectible current taxes | 9,000 | |||

| General revenues-property taxes | 1,931,000 | |||

| (To record the amount of property tax and amount of general revenue) | ||||

| 3. | GF | Interfund transfers out | 25,000 | |

| Cash | 25,000 | |||

| (To record the general fund transfer) | ||||

| ISF | Cash | 25,000 | ||

| Equipment | 300,000 | |||

| Accumulated Depreciation | 65,000 | |||

| Interfund Transfer In | 260,000 | |||

| (To record the inter-fund Transfer In) | ||||

| 4. | PF | Investment –marketable securities | 800,000 | |

| Revenues-contributions for endowment | 800,000 | |||

| (To record the donated marketable security) | ||||

| Cash | 40,000 | |||

| Revenues –Investment earnings | 40,000 | |||

| (To record the revenue at the end) | ||||

| PF | Interfund Transfer Out | 40,000 | ||

| Cash | 40,000 | |||

| (To record the Inter-fund Transfer Out) | ||||

| SRF | Cash | 40,000 | ||

| Interfund Transfers In | 40,000 | |||

| (To record the Inter-fund Transfer In) | ||||

| GA | Investment –marketable securities | 800,000 | ||

| General revenues-contributions for endowment | 800,000 | |||

| (To record marketable securities and general revenues) | ||||

| Cash | 40,000 | |||

| Programs revenues-culture and recreation- operating grants and contributions | 40,000 | |||

| (To record the donation made on culture and creation) | ||||

| 5. | EF | Due from other funds | 125,000 | |

| Charges for services | 125,000 | |||

| (To record the general fund for sewage and water services) | ||||

| Cash | 124,000 | |||

| Due from other funds | 124,000 | |||

| (To record the amount paid) | ||||

| GF | Expenditures | 125,000 | ||

| Due from other funds | 125,000 | |||

| (To record the actual due amount) | ||||

| Due from other funds | 124,000 | |||

| Cash | 124,000 | |||

| (To record the funds due to other funds) | ||||

| GA | Expense-general government | 125,000 | ||

| Internal balances | 125,000 | |||

| (To record the internal balance) | ||||

| Internal balances | 124,000 | |||

| Cash | 124,000 | |||

| (To record the cash settlement) | ||||

| 6. | ISF & GA | Inventory of supplies | 4,500 | |

| Cash | 4,500 | |||

| (To record the purchase of central duplicating fund) | ||||

| 7. | GF | Cash | 1,988,000 | |

| Taxes receivable-current | 1,925,000 | |||

| Revenues | 63,000 | |||

| (To record the cash collection) | ||||

| GA | Cash | 1,988,000 | ||

| Taxes receivable-current | 1,925,000 | |||

| Program revenue-general government-charges for services | 63,000 | |||

| (To record the cash collection) | ||||

| 8. | ISF | Due from other funds | 23,800 | |

| Billings to departments | 23,800 | |||

| (To record the total funds due from department) | ||||

| EF | Expense-administrative | 8,100 | ||

| Due to other funds | 8,100 | |||

| (To record the City’s utility fund) | ||||

| GF | Expenditures-General government | 15,700 | ||

| Due to other funds | 15,700 | |||

| (To record the internal service fund) | ||||

| GA | Internal balances | 8,100 | ||

| Program revenues-general government-charges for services | 8,100 | |||

| (To record the government charges for service) | ||||

| 9. | CPF | Cash | 5,000,000 | |

| Proceeds of bonds | 5,000,000 | |||

| (To record the sale of bond) | ||||

| Encumbrance | 4,500,000 | |||

| Encumbrances outstanding | 4,500,000 | |||

| (To record the amount of contract) | ||||

| GA | Cash | 5,000,000 | ||

| Bond payable | 5,000,000 | |||

| (To record the cash receipt on bond) | ||||

| 10. | GF | Encumbrance | 32,000 | |

| Encumbrances outstanding | 32,000 | |||

| (To record the issue of purchase order) | ||||

| Encumbrance Outstanding | 32,000 | |||

| Expenditures | 31,900 | |||

| Encumbrances | 32,000 | |||

| Cash | 31,900 | |||

| (To record the cash payment of purchase) | ||||

| GA | Equipment | 31,900 | ||

| Cash | 31,900 | |||

| (To record the purchase of equipment on cash) |

(Table 1)

Want to see more full solutions like this?

Chapter 9 Solutions

Accounting For Governmental & Nonprofit Entities

- As of January 1, 20X2, the City Council approved and the mayor signed a budget calling for $8,000,000 in estimated imposed and derived non-exchange revenues, $600,000 in estimated state grants, $6,000,000 in estimated expenditures and $1,500,000 to be transferred to debt service funds for the payment of principal and interest.Journal Entry would be?arrow_forwardThe county legislature approved the budget for the current year. Revenues from property taxes are budgeted at $800,000. According to the county assessor, the assessed valuation of all of the property in the county is $50,000,000. Of this amount, property worth $10,000,000 belongs to the federal government or to religious organizations and, therefore, is not subject to property taxes. In addition, certificates for the following exemptions have been filed: Homestead $2,500,000 Veterans 1,000,000 Old age, blindness, etc. 500,000 In the past, uncollectible property taxes averaged about 3 percent of the levy. This rate is not expected to change in the foreseeable future. Requirement: Calculate the levy on a piece of property that was assessed for $100,000 (after exemptions).arrow_forwardThe following information pertains to the City of Williamson for 2020, its first year of legal existence. For convenience, assume that all transactions are for the general fund, which has three separate functions: general government, public safety, and health and sanitation. Receipts: Property taxes $320,000 Franchise taxes 42,000 Charges for general government services 5,000 Charges for public safety services 3,000 Charges for health and sanitation services 42,000 Issued long-term note payable 200,000 Receivables at end of year: Property taxes (90% estimated to be collectible) 90,000 Payments: Salary: General government 66,000 Public safety 39,000 Health and sanitation 22,000 Rent: General government 11,000 Public safety 18,000 Health and sanitation 3,000 Maintenance: General government 21,000 Public safety 5,000 Health and sanitation 9,000 Insurance: General government 8,000 Public safety ($2,000 still prepaid…arrow_forward

- The following transactions occurred during the 2020 fiscal year for the City of Evergreen. For budgetary purposes, the city reports encumbrances in the Expenditures section of its budgetary comparison schedule for the General Fund but excludes expenditures chargeable to a prior year’s appropriation. The budget prepared for the fiscal year 2020 was as follows: Estimated Revenues: Taxes $ 1,957,000 Licenses and permits 374,000 Intergovernmental revenue 399,000 Miscellaneous revenues 64,000 Total estimated revenues 2,794,000 Appropriations: General government 475,200 Public safety 890,200 Public works 654,200 Health and welfare 604,200 Miscellaneous 88,000 Total appropriations 2,711,800 Budgeted increase in fund balance $ 82,200 Encumbrances issued against the appropriations during the year were as follows: General government $ 60,000 Public safety 252,000 Public works 394,000 Health and…arrow_forwardThe City of Fenton levied $3,000,000 of General Fund property taxes for the fiscal year ending December 31, 2011, with an estimated uncollectible amount of $200,000. During 2011 and January and February of 2012, $2,500,000 of the levy is expected to be collected; however, $300,000 of the levy is not expected to be collected until after February 2012. The amount of property tax revenues to be recognized in FY 2011 is:?arrow_forwardThe following information is provided about some of the Town of Truesdale’s General Fund operating statement and budgetary accounts for the fiscal year ended June 30. Estimated revenues $ 3,150,000 Revenues 3,190,000 Appropriations 3,185,000 Expenditures 3,175,000 Estimated other financing sources 400,000 Encumbrances 20,000 Encumbrances outstanding 20,000 Budgetary fund balance (calculate) The Town of Truesdale will honor all of its outstanding encumbrances in the next fiscal period. Prepare the journal entry(ies) to close budgetary accounts required to be closed at the fiscal year end using the information provided.arrow_forward

- Chesterfield County had the following transactions. A budget is passed for all ongoing activities. Revenue is anticipated to be $939,750, with approved spending of $594,000 and operating transfers out of $275,000. A contract is signed with a construction company to build a new central office building for the government at a cost of $6,000,000. The county previously recorded the budget for this project. Bonds are issued for $6,000,000 (face value) to finance construction of the new office building. The new building is completed. An invoice for $6,000,000 is received by the county and paid. Previously unrestricted cash of $1,350,000 is set aside by county officials to begin paying the bonds issued in (c). A portion of the bonds comes due, and $1,350,000 is paid. Of this total, $235,000 represents interest. The interest had not been previously accrued. Property tax levies are assessed. Total billing for this tax is $885,000. On this date, the assessment is a legally enforceable claim…arrow_forwardThe City of South Pittsburgh maintains its books so as to prepare fund accounting statements and records worksheet adjustments in order to prepare government-wide statements. Deferred inflows of resources—property taxes of $51,200 at the end of the previous fiscal year were recognized as property tax revenue in the current year’s Statement of Revenues, Expenditures, and Changes in Fund Balance. The City levied property taxes for the current fiscal year in the amount of $10,000,000. When making the entries, it was estimated that 2 percent of the taxes would not be collected. At year-end, $200,000 is thought to be uncollectible, $349,000 would likely be collected during the 60-day period after the end of the fiscal year, and $53,800 would be collected after that time. The City had recognized the maximum of property taxes allowable under modified accrual accounting. In addition to the expenditures recognized under modified accrual accounting, the City computed that $29,000 should be…arrow_forwardFor each of the following events or transactions, prepare the necessacry journal entries and identify the fund or funds that will be affected. 1. A governmental unit collects fees totaling $4,500 at the municipal pool. The fees are charged to recover costs of pool operation and maintenance 2. A county government that serves as a tax collection agency for all towns and cities located within the county collects county sales taxes totaling $125,000 for the month. 3. A $1,000,000 bond offering was issued, with a premium of $50,000, to subsidize the construction of a city visitor center. 4. A town receives a donation of $50,000 in bonds. The bonds should be held indefinitely, but bond income is to be donated to the local zoo. The zoo is associated with the town. 5. A central printing shop is established with a $150,000 nonreciprocal transfer from the general fund. 6. A $1,000,000 revenue bond offering was issued at par by a fund that provides water and sewer services to…arrow_forward

- For each of the following events or transactions, prepare the necessacry journal entries and identify the fund or funds that will be affected. 1. A governmental unit collects fees totaling $4,500 at the municipal pool. The fees are charged to recover costs of pool operation and maintenance 2. A county government that serves as a tax collection agency for all towns and cities located within the county collects county sales taxes totaling $125,000 for the month. 3. A $1,000,000 bond offering was issued, with a premium of $50,000, to subsidize the construction of a city visitor center. 4. A town receives a donation of $50,000 in bonds. The bonds should be held indefinitely, but bond income is to be donated to the local zoo. The zoo is associated with the town. 5. A central printing shop is established with a $150,000 nonreciprocal transfer from the general fund. 6. A $1,000,000 revenue bond offering was issued at par by a fund that provides water and sewer services to…arrow_forwardThe following transactions relate to the General Fund of the City of Buffalo Falls for the year ended December 31, 2020: Beginning balances were: Cash, $94,000; Taxes Receivable, $191,000; Accounts Payable, $53,000; and Fund Balance, $232,000. The budget was passed. Estimated revenues amounted to $1,240,000 and appropriations totaled $1,237,200. All expenditures are classified as General Government. Property taxes were levied in the amount of $920,000. All of the taxes are expected to be collected before February 2021. Cash receipts totaled $890,000 for property taxes and $300,000 from other revenue. Contracts were issued for contracted services in the amount of $97,000. Contracted services were performed relating to $87,000 of the contracts with invoices amounting to $85,200. Other expenditures amounted to $968,000. Accounts payable were paid in the amount of $1,100,000. The books were closed. Required:a. Prepare journal entries for the above transactions.b. Prepare a Statement of…arrow_forwardThe following information is available for the preparation of the government-wide financial statements for the City of Northern Pines for the year ended June 30, 2020: Expenses: General government $ 12,060,000 Public safety 24,509,000 Public works 11,578,000 Health and sanitation 6,163,000 Culture and recreation 4,509,000 Interest on long-term debt, governmental type 739,000 Water and sewer system 10,977,000 Parking system 418,000 Revenues: Charges for services, general government 1,340,000 Charges for services, public safety 214,800 Operating grant, public safety 816,300 Charges for services, health and sanitation 2,409,000 Operating grant, health and sanitation 1,237,600 Charges for services, culture and recreation 2,248,100 Charges for services, water and sewer 11,852,000 Charges for services, parking system 396,700 Property taxes 27,719,800 Sales taxes…arrow_forward

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning

Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning Survey of Accounting (Accounting I)AccountingISBN:9781305961883Author:Carl WarrenPublisher:Cengage Learning

Survey of Accounting (Accounting I)AccountingISBN:9781305961883Author:Carl WarrenPublisher:Cengage Learning