Concept explainers

Videos

Comprehensive Variance Analysis

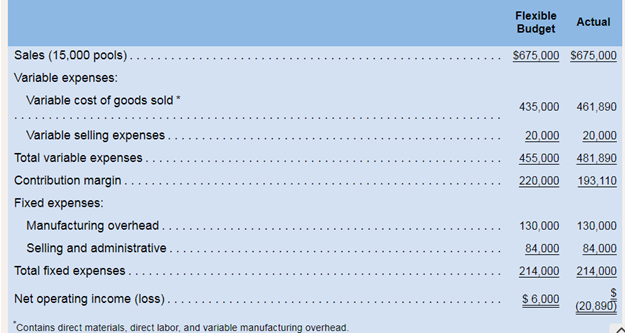

Miller Toy Company manufactures a plastic swimming pool at its Westwood Plant. The plant problems as shown by its June contribution format income statement below:

Janet Dunn. vio has just been appointed general mnagcr of the Westwood Plant. has been given instnctions to “get things under control. Upon reviewing the plants income statement. Ms. Dunn has concluded that the major problem lies in the variable cost of goods sold. She has been provided with the following

During June the plant produced 15,000 pools and incurred the following costs:

a. Purchased 60,000 pounds of materials at a cost of 54.95 per pound.

b. Used 49,200 pounds of materials in production. (Finished goods and work in process inventories are insignificant and can be ignored.)

c. Worked 11.800 direct labor-hours at a cost of 517.00 per hour.

d. Incurred variable

It is the company’s policy to close all variances to cost of goods solid on a monthly basis.

Required:

1. Compute the following variances for June:

a Materials price and quantity variances.

b. Labor rate and efficiency variances.

c. Variable overhead rate and efficiency variances.

2. Summarize the variances that you computed in (1) above by showing the net overall favorable or unfavorable variance for the month. What impact did this figure have on the company’s income statement? Show computations.

3. Pick out the two most significant variances that you computed in (1) above, Explain to Ms. Dunn possible causes of these variances.

1

Variances

A variance shows the difference between an actual amount and a budgeted or standard amount. Budgeted amount is calculated by a company using certain standards. A variance may either be favorable or unfavorable. It is usually considered as favorable if standard amount is higher than the actual amount.

To calculate: Value of various variances related to materials, labor and overheads.

Answer to Problem 18P

Material price variance is $3,000 Favorable and quantity variance is $3,200 Unfavorable.

Labor rate variance is calculated as $11,800Unfavorable and efficiency variance is $3,200 Favorable.

Overhead rate variance is calculated as $590Unfavorable and efficiency variance is $300 Favorable.

Explanation of Solution

Part a)

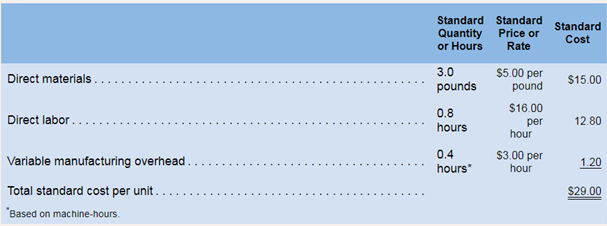

Calculation of material price and quantity variance:

Formula to calculate material price variance is

Here, actual quantity is given as 60,000 pounds, actual price is $4.95 per pound and standard price is $5 per pound. So, the variance will be:

Formula to calculate material quantity variance is

Here, actual quantity is given as 49,200, standard quantity is 45,000 (3.0 ponds * 15,000) and standard price is $5. So, the variance will be:

So, material price variance is $3,000 favorable and material quantity variance is $2,100 Unfavorable.

Part b)

Calculation of labor rate and efficiency variances:

Formula to calculate labor rate variance is

Here, actual hours are given as 11,800, actual rate is $17 and standard rate is $16. So, the variance will be:

Formula to calculate labor efficiency variance is

Here, standard rate is $16 per hour, actual hours are 11,800 and standard hours will be 12,000 (15,000 *0.8).So, variance will be:

Labor rate variance is calculated as $11,800unfavorable and efficiency variance is $3,200 Favorable.

Part c)

Calculation of variable overhead rate and efficiency variance:

Formula to calculate variable overhead rate variance is

Here, actual labor hours are 5,900 machine hours, actual rate is $3.10 ($18,290/5,900) and standard rate is $3.00. So, the variance will be:

Formula to calculate variable overhead efficiency variance is:

Here, standard rate is $3.00, actual hours are given as 5,900 and standard hours are 6,000 (15,000*0.4). So, the variance will be:

Variable overhead rate or spending variance is $590 Unfavorable and efficiency variance is $300 favorable.

2

Favorable or unfavorable variance

A variance is considered as a favorable variance if the actual amount is lower than the standard amount and it is considered unfavorable when actual amount is greater than the standard amount. After the calculation of all the variances, favorable or unfavorable amounts of all the variances are added to reach at the net overall effect.

To calculate: Amount of labor rate and efficiency variance.

Answer to Problem 18P

Overall, there is an unfavorable variance of $26,890.

Explanation of Solution

Net overall favorable or unfavorable variance will be calculated as:

| Variances | Amount | Net value |

| Material price variance | $3,000 F | |

| Material efficiency variance | $21,000 U | |

| Labor rate variance | $11,800 U | |

| Labor efficiency variance | $3,200 F | |

| Variable overhead rate or spending variance | $590 U | |

| Variable overhead efficiency variance | $300 F | |

| Net variance | $26,890 U |

There is a net unfavorable variance of $26,890. An unfavorable variance indicates that a company has incurred more, or extra cost as compare to its standard cost and therefore, it reduces the amount of profit earned by the company. This kind of variance alerts the management that profit of the company will be low than the expected profit. It should be detected at the earliest time possible and reasons of unfavorable variance should be fixed.

So, an unfavorable variance increase the cost and decreases the profit shown in the income statement.

3

Material efficiency variance

This variance represents the difference between the actual value of materials used by labor in producing goods and value that was budgeted to be used.

Labor rate variance

This variance represents the difference between actual value incurred on labors and value that was expected to be incurred.

To calculate: Amount of variable overhead rate and efficiency variance.

Answer to Problem 18P

Overhead rate variance is calculated as $280 unfavorable and efficiency variance is $480 Favorable.

Explanation of Solution

I am selecting the following two variances as most significant variances,

1 Material efficiency variance

2 Labor rate variance

I have selected theses two variances as they both have the highest unfavorable amount.

A material efficiency variance can be unfavorable because of several reasons, some of them are stated below:

1 When unskilled or unqualified labor is used.

2 When incorrect standards are used to calculate the standard cost.

2 When material having low quality is purchased.

3. When there is an increase in the wastages because of depreciation.

Labor rate variance can be unfavorable because of many reasons. Some of them are:

1 When incorrect standards are used to calculate the standard amount.

2 When some extra payments are being paid to labors.

3 When amount payable to labors include certain benefits.

4. When there some alterations are made in the product components.

Want to see more full solutions like this?

Chapter 9 Solutions

INTRO MGRL ACCT LL W CONNECT

- Refer to the information for Cinturon Corporation on the previous page. Required: 1. Break down the total variance for materials into a price variance and a usage variance using the columnar and formula approaches. 2. CONCEPTUAL CONNECTION Suppose the Boise plant manager investigates the materials variances and is told by the purchasing manager that a cheaper source of leather strips had been discovered and that this is the reason for the favorable materials price variance. Quite pleased, the purchasing manager suggests that the materials price standard be updated to reflect this new, less expensive source of leather strips. Should the plant manager update the materials price standard as suggested? Why or why not?arrow_forwardHaysbert Company provides management services for apartments and rental units. In general, Haysbert packages its services into two groups: basic and complete. The basic package includes advertising vacant units, showing potential renters through them, and collecting monthly rent and remitting it to the owner. The complete package adds maintenance of units and bookkeeping to the basic package. Packages are priced on a per-rental unit basis. Actual results from last year are as follows: Haysbert had budgeted the following amounts: Required: 1. Calculate the contribution margin variance. 2. Calculate the contribution margin volume variance. 3. Calculate the sales mix variance.arrow_forwardUse the following standard cost card for 1 gallon of ice cream to answer the questions. Actual direct costs incurred to make 50 gallons of ice cream: 275 quarts of cream at $1.05 per quart 832 ounces of sugar at $0.075 per ounce 165 minutes of labor at $37 per hour All materials used were bought during the current period. A. Compute the material and labor variances. B. comment on the results and possible causes of the variances.arrow_forward

- Iliff, Inc., produces and sells two types of countertop ovensthe toaster oven and the convection oven. Budgeted and actual data for the two models are shown below. Budgeted Amounts: Actual Amounts: Required: 1. Calculate the contribution margin variance. 2. What if actual units sold of the convection oven decreased? How would that affect the contribution margin variance? What if actual units sold of the convection oven increased? How would that affect the contribution margin variance?arrow_forwardMethod of Least Squares, Predicting Cost for Different Time Periods from the One Used to Develop a Cost Formula Refer to the information for Farnsworth Company on the previous page. However, assume that Tracy has used the method of least squares on the receiving data and has gotten the following results: Required: 1. Using the results from the method of least squares, prepare a cost formula for the receiving activity. 2. Using the formula from Requirement 1, what is the predicted cost of receiving for a month in which 1,450 receiving orders are processed? (Note: Round your answer to the nearest dollar.) 3. Prepare a cost formula for the receiving activity for a quarter. Based on this formula, what is the predicted cost of receiving for a quarter in which 4,650 receiving orders are anticipated? Prepare a cost formula for the receiving activity for a year. Based on this formula, what is the predicted cost of receiving for a year in which 18,000 receiving orders are anticipated?arrow_forwardSulert, Inc., produces and sells gel-filled ice packs. Sulerts performance report for April follows: Required: 1. Calculate the contribution margin variance and the contribution margin volume variance. 2. Calculate the market share variance and the market size variance. (CMA adapted)arrow_forward

- Absorption costing and production-volume variance—alternative capacity bases. Planet Light First (PLF), a producer of energy-efficient light bulbs, expects that demand will increase markedly over the next decade. Due to the high fixed costs involved in the business, PLF has decided to evaluate its financial performance using absorption costing income. The production-volume variance is written off to cost of goods sold. The variable cost of production is $2.40 per bulb. Fixed manufacturing costs are $1,170,000 per year. Variable and fixed selling and administrative expenses are $0.20 per bulb sold and $220,000, respectively. Because its light bulbs are currently popular with environmentally conscious customers, PLF can sell the bulbs for $9.80 each. PLF is deciding among various concepts of capacity for calculating the cost of each unit produced. Its choices are as follows: Calculate the inventoriable cost per unit using each level of capacity to compute fixed manufacturing cost per…arrow_forwardPlease redo this problem and show me steps on how to get the following questions correct, its stating I am wrong. Please help Direct Labor Variances The following data relate to labor cost for production of 6,600 cellular telephones: Actual: 4,480 hrs. at $16.10 $72,128 Standard: 4,410 hrs. at $16.40 $72,324 a. Determine the direct labor rate variance, direct labor time variance, and total direct labor cost variance. Enter all values as a positive number and then identify the variance (e.g. Favorable or Unfavorable) in the adjacent column. Rate variance $ Favorable Time variance $ Unfavorable Total direct labor cost variance $ Favorable b. The employees may have been less-experienced or poorly trained, thereby resulting in a lower labor rate than planned. The lower level of experience or training may have resulted in less efficient performance. Thus, the actual time required was more than standard. LIz Carrow_forwardThe managers of Sandusky Inc. have decided to use the month of January to determine the cost of producing their widget for the year. This will help determine proper product pricing and is important for control purposes. Using the data from January, the managers can determine the costs associated with material and labor. However, fixed indirect costs must still be determined. Management intends to use the prior year’s data to determine overhead costs. It is assumed that management will allocate an equal amount of estimated costs each month. Is this an appropriate decision by management? Should January be used as the reference point for the whole year?arrow_forward

- Standard Costing, Ethical Behavior, Usefulness of Costing Pat James, the purchasing agent for a local plant of the Oakden Electronics Division, was considering the possible purchase of a component from a new supplier. The component’s purchase price, $0.90 compared favorably with the standard price of $1.10. Given the quantity that would be purchased, Pat knew that the favorable price variance would help to offset an unfavorable variance for another component. By offsetting the unfavorable variance, his overall performance report would be impressive and good enough to help him qualify for the annual bonus. More importantly, a good performance rating this year would help him to secure a position at division headquarters at a significant salary increase. Purchase of the part, however, presented Pat with a dilemma. Consistent with his past behavior, Pat made inquiries regarding the reliability of the new supplier and the part’s quality. Reports were basically…arrow_forwardCarad Co. is an electronics company which makes two types of televisions – plasma screenTVs and LCD TVs. It operates within a highly competitive market and is constantly underpressure to reduce prices and develop new products. Carad Co. operates a standard costingsystem and performs a detailed variance analysis of both products on a monthly basis. Extracts from the management information for the month of November are shown below:NoteTotal number of units made and sold 1,400 1Material price variance $28,000 A 2 Notes.(1) The budgeted total sales volume for TVs was 1,180 units, consisting of an equal mixof plasma screen TVs and LCD screen TVs. Actual sales volume was 750 plasmaTVs and 650 LCD TVs. Standard sales prices are $350 per unit for the plasma TVsand $300 per unit for the LCD TVs. The actual sales prices achieved duringNovember were $330 per unit for plasma TVs and $290 per unit for LCD TVs. Thestandard contributions…arrow_forwardData table Month Total Cost Machine Hours January.. 3,420 1,090 February..... S 3,760 1,120 March .... $ 3,532 1,080 April ..... 3,720 1,220 May S 4,800 1,330 June 4,192 1,480 .. %24 %24arrow_forward

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College