Concept explainers

Videos

Expected

Standard deviation is the financial measure of risk and stability on the

Coefficient of variance is a measure used to calculate the total risk per unit of return of an investment.

Explanation of Solution

Calculate the expected return as follows:

Therefore, the expected return is

Calculate the standard deviation as follows:

Therefore, the standard deviation is

Calculate the coefficient of variance as follows:

Therefore, the coefficient of variance is

Want to see more full solutions like this?

- Supposing the return from an investment has the following probability distribution Return Probability R (%) 8 0.2 10 0.2 12 0.5 14 0.1 Required: What is the expected return of the investment? What is the risk as measured by the standard deviation of expected returns?arrow_forwardPlease find the following: The investment's expected return as a percentage: The investment's standard deviation:arrow_forwardOn the basis of the utility formula below, which investment would you select if you were risk averse with A = 4? Investment Expected return E(r) Standard deviation σ 1 0.12 0.30 2 0.15 0.50 3 0.21 0.16 4 0.24 0.21arrow_forward

- Given the following probability distribution of returns: Probability Return 0.1 -15.0% 0.25 0.0% 0.3 8.5% 0.25 12.0% 0.1 32.0% what is the expected return?arrow_forwardThe standard deviation of return on investment a is 0.10, while the standard deviation of return on investment b is 0.04. If the correlation coefficient between the returns on A and B is_____________. A. -0.0447 B. -0.0020 C. 0.0020 D. 0.0447arrow_forwardWhat is the standard deviation of the following portfolio if the coefficient of the correlation between the two securities is equl to 0.5? Variance % Proportion of investment in the portfolio security 1 10 0.3 security 2 20 0.7arrow_forward

- Two investments generated the following annual returns (refer to image): a. What is the average annual return on each investment?b. What is the standard deviation of the return on investments X and Y?c. Based on the standard deviation, which investment was riskier?arrow_forwardWhat is the correlation coefficient between returns on any efficient portfolio and returns on the market portfolio in CAPM? 0.5 -0.5 -1 1 Oarrow_forwardConsider two assets. Suppose that the return on asset 1 has expected value 0.05 and standard deviation 0.1 and suppose that the return on asset 2 has expected value 0.02 and standard deviation 0.05. Suppose that the asset returns have correlation 0.4.Consider a portfolio placing weight w on asset 1 and weight 1-w on asset 2; let Rp denote the return on the portfolio. Find the mean and variance of Rp as a function of w.arrow_forward

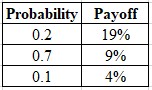

- Based on the following probability distribution, what is the security's expected return? State Probability 1 0.2 -5.0% 2 0.3 10.0 3 0.5 30.0 What is the expected return of the following investment? Probability Payoffarrow_forwardThe internal rate of return equals the rate that yields a profitability index of 1 for an investment. True O Falsearrow_forwardAssuming the following returns and corresponding probabilities for Asset D: Rate of Return Probability 10% 30% 15% 40% 20% 30% Compute for: a. Expected rate of return b. The standard deviation c. The coefficient of variationarrow_forward