Videos

AKL Foundry manufactures metal components for different kinds of equipment used by the aerospace, commercial aircraft, medical equipment, and electronic industries. The company uses investment casting to produce the required components. Investment casting consists of creating, in wax, a replica of the final product and pouring a hard shell around it. After removing the wax, molten metal is poured into the resulting cavity. What remains after the shell is broken is the desired metal object ready to be put to its designated use.

Metal components pass through eight processes: gating, shell creating, foundry work, cutoff, grinding, finishing, welding, and strengthening. Gating creates the wax mold and clusters the wax pattern around a sprue (a hole through which the molten metal will be poured through the gates into the mold in the foundry process), which is joined and supported by gates (flow channels) to form a tree of patterns. In the shell-creating process, the wax molds are alternately dipped in a ceramic slurry and a fluidized bed of progressively coarser refractory grain until a sufficiently thick shell (or mold) completely encases the wax pattern. After drying, the mold is sent to the foundry process. Here, the wax is melted out of the mold, and the shell is fired, strengthened, and brought to the proper temperature. Molten metal is then poured into the dewaxed shell. Finally, the ceramic shell is removed, and the finished product is sent to the cutoff process, where the parts are separated from the tree by the use of a band saw. The parts are then sent to the grinding process, where the gates that allowed the molten metal to flow into the ceramic cavities are ground off using large abrasive grinders. In the finishing process, rough edges caused by the grinders are removed by small handheld pneumatic tools. Parts that are flawed at this point are sent to welding for corrective treatment. The last process uses heat to treat the parts to bring them to the desired strength.

In 20X1, the two partners who owned AKL Foundry decided to split up and divide the business. In dissolving their business relationship, they were faced with the problem of dividing the business assets equitably. Since the company had two plants—one in Arizona and one in New Mexico—a suggestion was made to split the business on the basis of geographic location. One partner would assume ownership of the plant in New Mexico, and the other would assume ownership of the plant in Arizona. However, this arrangement had one major complication: the amount of WIP inventory located in the Arizona plant.

The Arizona facilities had been in operation for more than a decade and were full of WIP. The New Mexico facility had been operational for only 2 years and had much smaller WIP inventories. The partner located in New Mexico argued that to disregard the unequal value of the WIP inventories would be grossly unfair.

Unfortunately, during the entire business history of AKL Foundry, WIP inventories had never been assigned any value. In computing the cost of goods sold each year, the company had followed the policy of adding

During 20X1, the Arizona plant had sales of $2,028,670. The cost of goods sold is itemized as follows:

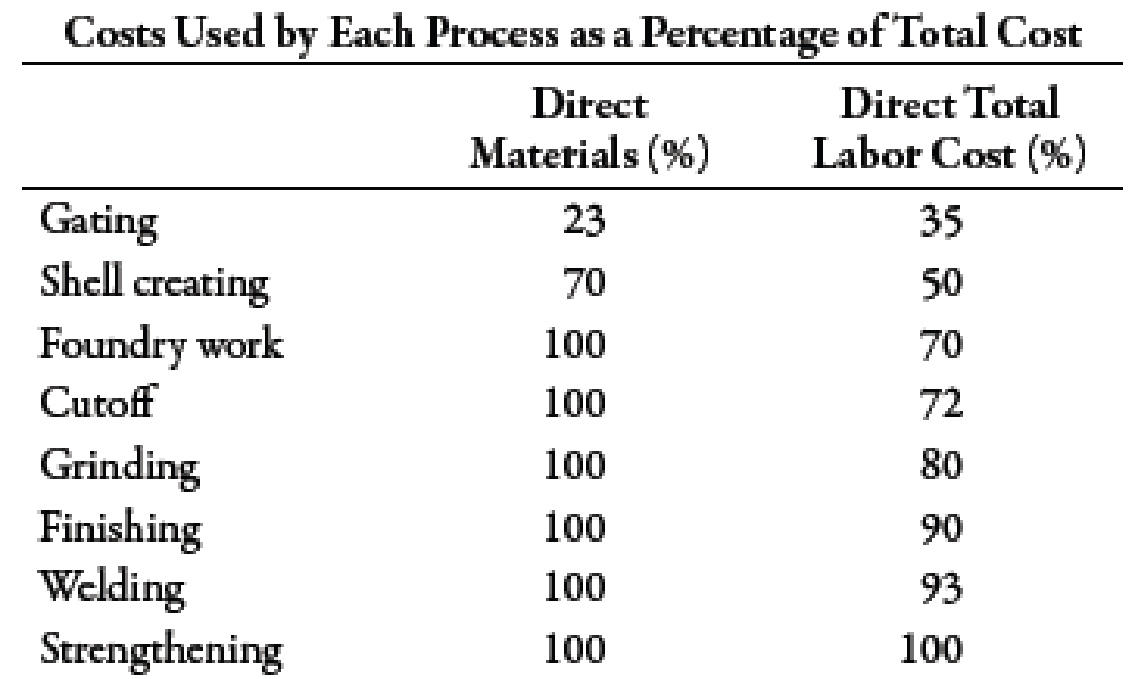

Upon request, the owners of AKL provided the following supplementary information (percentages are cumulative):

Gating had 10,000 units in BWIP, 60% complete. Assume that all materials are added at the beginning of each process. During the year, 50,000 units were completed and transferred out. The ending inventory had 11,000 unfinished units, 60% complete.

Required:

- 1. The partners of AKL want a reasonable estimate of the cost of WIP inventories. Using the gating department’s inventory as an example, prepare an estimate of the cost of the EWIP. What assumptions did you make? Did you use the FIFO or weighted average method? Why? (Note: Round unit cost to two decimal places.)

- 2. Assume that the shell-creating process has 8,000 units in BWIP, 20% complete. During the year, 50,000 units were completed and transferred out. (Note: All 50,000 units were sold; no other units were sold.) The EWIP inventory had 8,000 units, 30% complete. Compute the value of the shell-creating department’s EWIP. What additional assumptions had to be made?

1.

Provide an estimate of the ending WIP of gating process. Also, explain the method used to measure WIP and reason for such selection.

Explanation of Solution

Process Costing:

Process costing is a system in which an organization ascertains costs associated which specific processes undertaken within the company.

Step 1: Physical flow analysis:

| Particulars | Units |

| Units to account for: | |

| Units in beginning WIP | 10,000 |

| Add: Units started during the period1 | 51,000 |

| Units to account for | 61,000 |

| Units accounted for: | |

| Units completed and transferred | 50,000 |

| Add: Units in ending WIP | 11,000 |

| Units accounted for | 61,000 |

Table (1)

Step 2: Computation of equivalent units:

| Particulars | Material | Conversion |

| Units started and completed | 40,000 | 40,000 |

|

Equivalent units of beginning WIP | 4,000 | |

|

Equivalent units of ending WIP | 11,000 | 6,600 |

| Equivalent units | 51,000 | 50,600 |

Table (2)

Step 3: Computation of unit cost:

| Particulars | Material ($) | Conversion ($) |

| Material cost | 86,940 | |

| Labor cost | 185,605 | |

| Overhead cost | 225,231 | |

| Total cost | 86,940 | 410,836 |

| Equivalent units | 51,000 | 50,600 |

| Unit cost | 1.70 | 8.12 |

Table (3)

Step 4: Valuation of ending inventory:

| Particulars | Amount ($) |

| Equivalent units of material | 18,700 |

| Equivalent units for conversion | 53,592 |

| Total value | 72,292 |

Table (4)

FIFO method has been used since, costs associated with beginning inventory is to be removed from the equivalent units so that current period’s cost can be correctly allocated amongst the equivalent units for computation of unit cost.

Working Notes:

1. Computation of units started during the period:

2.

Provide an estimate of the ending WIP of shell-creating process.

Explanation of Solution

Step 1: Physical flow analysis:

| Particulars | Units |

| Units to account for: | |

| Units in beginning WIP | 8,000 |

| Add: Units started during the period1 | 50,000 |

| Units to account for | 58,000 |

| Units accounted for: | |

| Units completed and transferred | 50,000 |

| Add: Units in ending WIP | 8,000 |

| Units accounted for | 58,000 |

Table (5)

Step 2: Computation of equivalent units:

| Particulars | Material | Conversion |

| Units started and completed | 42,000 | 42,000 |

|

Equivalent units of beginning WIP | 6,400 | |

|

Equivalent units of ending WIP | 8,000 | 2,400 |

| Equivalent units | 50,000 | 50,800 |

Table (6)

Step 3: Computation of unit cost:

| Particulars | Material ($) | Conversion ($) |

| Material cost | 177,660 | |

| Labor cost | 79,545 | |

| Overhead cost | 96,528 | |

| Total cost | 177,660 | 176,073 |

| Equivalent units | 50,000 | 50,800 |

| Unit cost | 3.55 | 3.47 |

Table (7)

Step 4: Valuation of ending inventory:

| Particulars | Amount ($) |

| Equivalent units of material | 28,400 |

| Equivalent units for conversion | 8,328 |

| Transferred in | 78,560 |

| Total value | 115,288 |

Table (8)

Working Notes:

1.

Computation of units started during the period:

Want to see more full solutions like this?

Chapter 6 Solutions

EBK MANAGERIAL ACCOUNTING: THE CORNERST

- Reducir, Inc., produces two different types of hydraulic cylinders. Reducir produces a major subassembly for the cylinders in the Cutting and Welding Department. Other parts and the subassembly are then assembled in the Assembly Department. The activities, expected costs, and drivers associated with these two manufacturing processes are given below. Note: In the assembly process, the materials-handling activity is a function of product characteristics rather than batch activity. Other overhead activities, their costs, and drivers are listed below. Other production information concerning the two hydraulic cylinders is also provided: Required: 1. Using a plantwide rate based on machine hours, calculate the total overhead cost assigned to each product and the unit overhead cost. 2. Using activity rates, calculate the total overhead cost assigned to each product and the unit overhead cost. Comment on the accuracy of the plantwide rate. 3. Calculate the global consumption ratios. 4. Calculate the consumption ratios for welding and materials handling (Assembly) and show that two drivers, welding hours and number of parts, can be used to achieve the same ABC product costs calculated in Requirement 2. Explain the value of this simplification. 5. Calculate the consumption ratios for inspection and engineering, and show that the drivers for these two activities also duplicate the ABC product costs calculated in Requirement 2.arrow_forwardHales Company produces a product that requires two processes. In the first process, a subassembly is produced (subassembly A). In the second process, this subassembly and a subassembly purchased from outside the company (subassembly B) are assembled to produce the final product. For simplicity, assume that the assembly of one final unit takes the same time as the production of subassembly A. Subassembly A is placed in a container and sent to an area called the subassembly stores (SB stores) area. A production Kanban is attached to this container. A second container, also with one subassembly, is located near the assembly line (called the withdrawal store). This container has attached to it a withdrawal Kanban. Required: 1. Explain how withdrawal and production Kanban cards are used to control the work flow between the two processes. How does this approach minimize inventories? 2. Explain how vendor Kanban cards can be used to control the flow of the purchased subassembly. What implications does this have for supplier relationships? What role, if any, do continuous replenishment and EDI play in this process?arrow_forwardRecently, Mewah Designs expanded its market by becoming an original equipment supplier toJee Wrangler. Mewah Designs produces factory upgraded speakers specifically for JeeWrangler. The Kicker components and speaker cabinets are outsourced with assemblyremaining in-house. Mewah Designs assemble the product by placing the speakers and othercomponents in cabinets that define an audio package upgrade and that can be placed into theJee Wrangler, producing the desired factory-installed appearance. Speaker cabinets andassociated Kicker components are added at the beginning of the assembly process.Assume that Mewah Designs uses the weighted-average method to cost out the audio package.The following are cost and production data for the assembly process for April: Production:Units in process, April 1, 60% complete 60,000Units completed and transferred out 150,000Units in process, April 30, 20% complete 30,000Costs:WIP, April 1:Cabinets RM 1,200,000Kicker components RM 12,600,000Conversion costs…arrow_forward

- Confer Company produces two different metal components used in medical equipment (Component X and Component Y). The company has three processes: molding, grinding, and finishing. In molding, molds are created, and molten metal is poured into the shell. Grinding removes the gates that allowed the molten metal to flow into the molds cavities. In finishing, rough edges caused by the grinders are removed by small, handheld pneumatic tools. In molding, the setup time is one hour. The other two processes have no setup time required. The demand for Component X is 600 units per day, and the demand for Component Y is 1,000 units per day. The minutes required per unit for each product are as follows: The company operates one eight-hour shift. The molding process employs 24 workers (who each work eight hours). Two hours of their time, however, are used for setups (assuming both products are produced). The grinding process has sufficient equipment and workers to provide 400 grinding hours per shift. The Finishing Department is labor intensive and employs 70 workers, who each work eight hours per day. The only significant unit-level variable costs are materials and power. For Component X, the variable cost per unit is 40, and for Component Y, it is 50. Selling prices for X and Y are 90 and 110, respectively. Confers policy is to use two setups per day: an initial setup to produce all that is scheduled for Component X and a second setup (changeover) to produce all that is scheduled for Component Y. The amount scheduled does not necessarily correspond to each products daily demand. Required: 1. Calculate the time (in minutes) needed each day to meet the daily market demand for Component X and Component Y. What is the major internal constraint facing Confer Company? 2. Describe how Confer should exploit its major binding constraint. Specifically, identify the product mix that will maximize daily throughput. 3. Assume that manufacturing engineering has found a way to reduce the molding setup time from one hour to 10 minutes. Explain how this affects the product mix and daily throughput.arrow_forwardDestin Company produces water control valves, made of brass, that it sells primarily to builders for use in commercial real estate construction. These valves must meet rigid specifications (i.e., the quality tolerance is small). Valves that, upon inspection, get rejected are returned to the Casting Department; that is, they are returned to stage 1 of the four-stage manufacturing process. Rejected items are melted and then recast. As such, no new materials in Casting are required to rework these items. However, new materials must be added in the Finishing Department for all reworked valves. As the cost accountant for the company, you have prepared the following cost data regarding the production of a typical valve: Casting $ 220 Finishing $ 10 Inspection $ 0 Packing $ 10 Cost Total Direct materials $ 240 Direct labor 120 130 30 30 310 Variable manufacturing overhead 120 160 30 30 340 Allocated fixed overhead 80 90 50 20 240 $ 540 $ 390 $ 110 $ 90 $ 1,130 The company, spurred by intense…arrow_forwardDestin Company produces water control valves, made of brass, that it sells primarily to builders for use in commercial real estate construction. These valves must meet rigid specifications (i.e., the quality tolerance is small). Valves that, upon inspection, get rejected are returned to the Casting Department; that is, they are returned to stage 1 of the four-stage manufacturing process. Rejected items are melted and then recast. As such, no new materials in Casting are required to rework these items. However, new materials must be added in the Finishing Department for all reworked valves. As the cost accountant for the company, you have prepared the following cost data regarding the production of a typical valve: Cost Direct materials Direct labor Casting $ 220 Finishing $ 15 Inspection $ 0 Packing $ 10 Total $ 245 125 135 25 25 310 Variable manufacturing overhead Allocated fixed overhead 150 165 20 20 355 85 95 120 90 390 $ 580 2$ $ 410 $ 165 $ 145 $ 1,300 The company, spurred by…arrow_forward

- Destin Company produces water control valves, made of brass, that it sells primarily to builders for use in commercial real estate construction. These valves must meet rigid specifications (i.e., the quality tolerance is small). Valves that, upon inspection, get rejected are returned to the Casting Department; that is, they are returned to stage 1 of the four-stage manufacturing process. Rejected items are melted and then recast. As such, no new materials in Casting are required to rework these items. However, new materials must be added in the Finishing Department for all reworked valves. As the cost accountant for the company, you have prepared the following cost data regarding the production of a typical valve: Skipped Cost Direct materials Direct labor Variable manufacturing overhead Allocated fixed overhead Casting $ 250 135 Finishing $ 15 145 175 105 Inspection $ 0 20 Packing $ 10 20 20 35 Total $ 275 320 365 300 150 95 20 65 $630 $ 440 $105 $ 85 $ 1,260 The company, spurred by…arrow_forwardMany producers of complex products actually combine manufacturing processes with assembly duties. This means that they make some parts of the finished goods inventory, but they also purchase manufactured components from other manufacturers to include in their products. For example, an automobile manufacturer may purchase rolls of steel and manufacture the shell of the vehicle (hoods, fenders, and so forth). Auto makers also purchase some vehicle parts completed by other manufacturers to produce a finished vehicle. Car makers purchase tires, airbags, windshields, and many other components in their finished state to complete a vehicle. Discuss how you would determine the standard cost and actual cost of finished vehicle produced by a car maker that both manufactures its own parts and assembles parts manufactured by other companies.arrow_forwardMany producers of complex products actually combine manufacturing processes with assembly duties. This means that they make some parts of the finished goods inventory, but they also purchase manufactured components from other manufacturers to include in their products. For example, an automobile manufacturer may purchase rolls of steel and manufacture the shell of the vehicle (hoods, fenders, and so forth). Auto makers also purchase some vehicle parts completed by other manufacturers to produce a finished vehicle. Car makers purchase tires, airbags, windshields, and many other components in their finished state to complete a vehicle. Discuss how you would determine the standard cost and actual cost of finished vehicle produced by a car maker that both manufactures its own parts and assembles parts manufactured by other companies. Let's not go onto Chegg and us an answer from there! I already asked this question on Bartleby... but unfortunately the person used an answer from Chegg for…arrow_forward

- Operations Costing Sign It! makes outdoor advertising signs which it sells to advertising companies. The company uses operation costing and manufactures their outdoor signs in four operations. In the Cutting operation, the signs are cut into the correct size from large, unfinished sheets they acquire from an outside supplier. In Finishing, the edges are smoothed and a magnetic metal surface is added. In Framing, the signs are inserted into a metal frame and stand. In Packaging, the signs are inspected and packaged. Not all signs are framed as some customers prefer to insert the sign into their own frames. During January of the current year, the following conversion costs will be incurred by the company: Cutting Finishing Framing Packaging $280,000 $130,200 $84,000 $56,000 Sign It! computes conversion cost rates per unit each month. In January, the company will manufacture 70,000 signs, 20,000 of which will NOT be framed. Details of two work orders for January…arrow_forwardFrom the production process description provided, at what point do you think most of the direct materials are added to the process when manufacturing gummy bears?arrow_forwardGladden Dock Company manufactures boat docks on an assembly line. Its costing system uses two cost categories, direct materials and conversion costs. Each product must pass through the Assembly Department and the Finishing Department. This problem focuses on the Assembly Department. Direct materials are added at the beginning of the production process. Conversion costs are allocated evenly throughout production. The firm uses FIFO method and the controller prepared the following (correct) equivalent unit calculation. Unitscompleted Physical Units Direct Materials Conversion WIP, beginning 70 0 52.5 Started and completed 30 30 30 WIP, ending 10 10 5 Totals 110 40 87.5 Cost per Equiv Unit $4,000 $16,000 Work in process, beginning inventory: Current Costs:Direct materials $140,000 Direct materials $ 160,000Conversion costs $260,000 Conversion…arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College