Videos

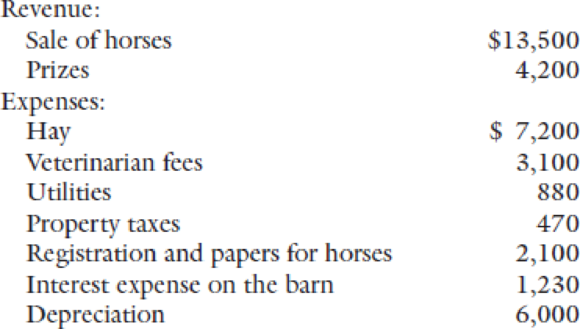

Allison and Paul are married and have no children. Paul is a lawyer who earns a salary of $80,000. In November 2017, Allison quit her job as a copy editor and began exploring the possibility of breeding and showing horses. She would run the business on their property. Allison expects to travel to nine or ten horse shows during the year. While researching the activity, she came across an article entitled: “IRS Cracking Down on Horse Breeding—Is It Really a Business or Is It a Hobby?” She is unsure of the tax ramifications discussed in the article and has come to you for advice on whether her activity will be considered a business or a hobby. Allison provides you with the following projections of the 2018 income and expense items for the horse breeding and showing activity:

Paul and Allison expect to receive $6,000 in interest and dividend income, they will have an $8,000 net long-term

Want to see the full answer?

Check out a sample textbook solution

Chapter 5 Solutions

Concepts in Federal Taxation 2019 (with Intuit ProConnect Tax Online 2017 and RIA Checkpoint 1 term (6 months) Printed Access Card)

- Your supervisor has asked you to research the following situation concerning Scott and Heather Moore. Scott and Heather are married and file a joint return. Scott works full-time as a wildlife biologist, and Heather is a full-time student enrolled at Online University. Scott’s earned income for the year is $36,000. Heather does not have a job and concentrates solely on her schoolwork. The university she is enrolled in offers courses only through the Internet. Scott and Heather have one child, Elizabeth (age 8), and pay $3,000 for child care expenses during the year.arrow_forwardHeather owns all of the shares of Thompson Consulting Ltd (TCL), an IT consulting firm with 10 employees. TCL has a December 31 st year-end. Heather delegates all of her oversight tasks to various managers because she is busy at home raising her family. On July 25, 2011, Heather borrowed $100,000 from TCL for the purchase of a new home on a non-interest bearing basis. A loan agreement is in place that requires her to repay the full amount in five years. She has never reported anything on her personal income tax return from the loan. Assuming that you are preparing Heather's personal tax return for the first time, which of the following statements is correct? A). There are no income tax consequences because the funds were borrowed for the purchase of a home and there is a bona fide arrangement to repay the loan. B). Heather will have a deemed interest benefit in 2011,2012 and 2013. C). Heather will have an income inclusion of $100,000 in 2013 and a deemed interest benefit in 2011, 2012…arrow_forwardAshley begins a very successful graphic design company on January 10, 2021. She decides not to incorporate and remains a sole proprietor, earning $80,000 in net business income. In the past she has never had business income, and is wondering if this will change, when she has to file her taxes. Her net tax owing in 2010 was $4,100 and in 2020 was $3,200. She expects her net owing in 2021 to be around $3,500 Required: Explain to Ashley if she will have to pay instalments? Explain to her whether instalments are required, and if applicable, why. 1 A BIG Provide your answer here: 1. 9-arrow_forward

- Unfortunately, Betty’s business was not profitable. She decided to sell the business andseek work in a different industry. She sold her business in May 2020 after spending$22,000 on advertising the sale with an estate agent. Unfortunately, the sales proceedswere not sufficient to discharge her existing bank loan and she was required to makeregular monthly interest payments on the outstanding balance.Please discuss whether the advertising expenses would be deductiblearrow_forwardTimmy, a CPA, caught “long COVID” early in 2020 and had to retire from his accounting firm job. One result was that he no longer could pay the mortgage on the 40-acre ranch he owned in Hunt County. (Timmy had never actually lived there, he’s always lived in Dallas – he was a “gentleman-rancher” only…) Of course once Timmy stopped making his mortgage payments, Friendly Nation-al Bank, the mortgage holder on the ranch, became very much less friendly. It foreclosed and took ownership of the ranch on November 1, 2020. Here are some additional facts: Timmy had purchased the ranch for $1,600,000 in 2016. The principal balance on the mortgage on Nov. 1, 2020, was $1,200,000. Timmy’s 2020 property tax bill for the ranch showed an appraised value of $900,000. In January 2021 the bank sent Timmy a Form 1099-C. In Box 2 (Amount of debt discharged) the bank entered $1,200,000. The bank left Box 7 (Fair market value of property) blank. Timmy was never actually insolvent (in the balance-sheet…arrow_forwardJulian Thomas, who is single, goes to graduate school part-time and works as a waiter at the Bay Grill in San Francisco. During 2018, his gross income was $20,700 in wages and tips. He has decided to prepare his own tax return because he cannot afford the services of a tax expert. After preparing his return, he comes to you for advice. Here's a summary of the figures he has prepared thus far: Gross income: Wages $12,700 Tips +8,000 Adjusted gross income (AGI) $20,700 Less: Standard deduction $12,000 Taxable income $8,700 Julian believes that if an individual's income falls below $23,000, the federal government considers him or her "poor" and allows both itemized deductions and a standard deduction. He has found $2,200 in potential itemized deductions. Calculate Julian Thomas' taxable income. Assume that the standard deduction for a single taxpayer is $12,000. Note that personal exemptions were suspended for 2018. $ Discuss Julian's…arrow_forward

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT