Concept explainers

Videos

Compute equivalent units in second department (Learning Objectives 2 & 5)

Refer to the Arctic Springs Bottling Department Data Set.

- 1. Draw a time line.

- 2. Complete the first two steps of the

process costing procedure for the Bottling Department: summarize the physical flow of units and then compute the equivalent units of direct materials and conversion costs.

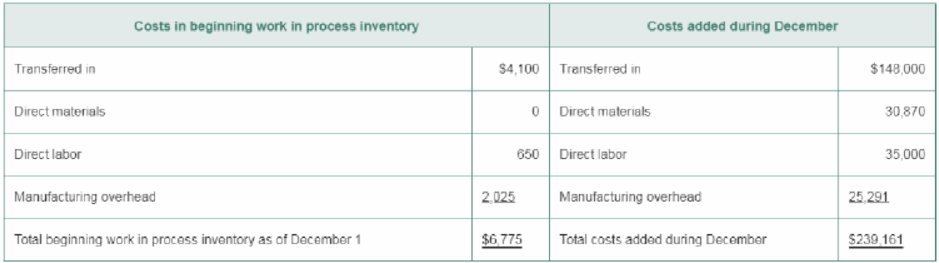

Arctic Springs Data Set: Bottling Department

Arctic Springs produces premium bottled water. The preceding Short Exercises considered the first process in bottling premium water— Filtration. We now consider Arctic Springs’ second process—Bottling. In the Bottling Department, workers bottle the filtered water and pack the bottles into boxes. Conversion costs are incurred evenly throughout the Bottling process, but packaging materials are not added until the end of the process.

December data from the Bottling Department follow:

| Beginning work in process inventory (45% of the way through the process) | 9,000 liters |

| Transferred in from Filtration | 160,000 liters |

| Completed and transferred out to Finished Goods Inventory in December | 147,000 liters |

| Ending work in process inventory (85% of the way through the bottling process) | 22,000 liters |

The Filtration Department completed and transferred out 160,000 liters at a total cost of $148,000.

Want to see the full answer?

Check out a sample textbook solution

Chapter 5 Solutions

Managerial Accounting (5th Edition)

- Calculating and Interpreting Activity-Based Costing Data Hiram’s Lakeside is a popular restaurant located on Lake Washington in Seattle. The owner of the restaurant has been trying to better understand costs at the restaurant and has hired a student intern to conduct an activity-based costing study. The intern, in consultation with the owner, identified three major activities and then completed the first-stage allocations of costs to the activity cost pools. The results appear below. The above costs include all of the costs of the restaurant except for organization-sustaining costs such as rent, property taxes, and top-management salaries. Some costs, such as the cost of cleaning the linens that cover the restaurant’s tables, vary with the number of parties served. Other costs, such as washing plates and glasses, depend on the number of diners served or the number of drinks served. Prior to the activity-based costing study, the owner knew very little about the costs of the restaurant.…arrow_forwardFor each of the following activities, select the most appropriate cost driver. Each cost driver may be used only once. Activity Cost Driver 1. Pay vendors Answer 2. Evaluate vendors Answer 3. Inspect raw materials Answer 4. Plan for purchases of raw materials Answer 5. Packaging Answer 6. Supervision Answer 7. Employee training Answer 8. Clean tables Answer 9. Machine maintenance Answer 10. Move in-process product from one work station to the next Answerarrow_forwardI have the following information: direct materials $250 and total manufacturing cost $700. Overhead applied to jobs at a rate of 200% of direct labor cost. This is for Chapter 2 job costing in managerial accounting. I am supposed to figure out conversion cost, direct labor cost, and manufacturing overhead. I know the formula for conversion cost= direct labor + manufacturing OH Prime cost= direct labor + direct materials How do I figure out direct labor cost with the given information? The learning objective states calcualte predetermined overhead rate, but I do not have estimated manufacturing cost and estimated labor. Can you please help? Thanks, Erica Gordonarrow_forward

- In Class Assignment 1 AlSaleh has assigned overhead on a plantwide basis to its two products (Tables and Chairs) using direct labor hours which are estimated to be 200,000 for the current year. The company has decided to experiment with activity-based costing and has created two activity cost pools and related activity cost drivers. These two cost pools are Ordering and receiving (cost driver is Purchase orders) and machine setup (cost driver is number of setups). Overhead allocated to the ordering and receiving cost pool is $200,000, and $800,000 is allocated to the machine setup cost pool. Additional information related to these pools is as follows: Cost Drivers Tables Chairs Purchase orders 30,000 10,000 number of setups 10,000 30,000 a. Determine the amount of overhead assigned to the table product line and the chairs product line using activity-based costing. b. What amount of overhead would be assigned to the tables and chairs product lines using the traditional approach,…arrow_forwardE-LEARNING SERVICES SQU LIBRARIES -LEARNING SYSTEM (ACADEMIC) Process costing: Time left 1:55:02 O a. allocates applied manufacturing overhead cost to product cost. O b. is normally used by companies which produce shoes. O C. All the given answers are correct. O d. uses the manufacturing accounts, including Manufacturing Overhead, Raw Materials, Work in Process, and Finished Goods. O e. assigns direct materials cost, direct labor cost, and manufacturing overhead costs to products to compute product cost per unit. Company XYZ made total sales revenue of $200,000. The variable manufacturing costs were $75,000 while the fixed manufacturing costs were $20,000. The variable selling and administrative expenses were $45,000 while the fixed selling and administrative expenses were $10,000. How much was the total contribution margin ($)? O a. 125,000 O b. 105,000 Fi O C. 145,000 O d. None of the given answers O e. 80,00Oarrow_forwardFor all Problems, assume the weighted-average method is to be used unless you are told otherwise. Preparing a production cost report, second department, with beginning WIP and transferred in costs; journal entries; FIFO method Happy Colors manufactures crayons in a three-step process: mixing, molding packaging. The Mixing Department combines the direct materials of paraffin wax and pigments. The heated mixture is pumped to the Molding Department, where it is poured into molds. After the molds cool, the crayons are removed from the molds and are transferred to the Packaging Department, where paper wrappers are added and the crayons are boxed. In the Mixing Department, the direct materials are added at the beginning of the process and the conversion costs are incurred evenly throughout the process. Work in process of the Mixing Department on April 1, 2018, consisted of 300 batches of crayons that were 30% of the way through the production process. The beginning balance in Work-in-Process…arrow_forward

- help mearrow_forwardActivity-based product costing Sweet Sugar Company manufactures three products (white sugar, brown sugar, and powdered sugar) in a continuous production process. Senior management has asked the controller to conduct an activity-based costing study. The controller identified the amount of factory overhead required by the critical activities of the organization as follows: Activity Production Setup Inspection Shipping Customer Service Total The activity bases identified for each activity are as follows: Activity Base Activity Production Setup Inspection Shipping Customer Service Budgeted Activity Cost Machine hours Number of setups Number of inspections Number of customer orders $418,900 298,900 85,800 112,000 91,700 $1,007,300 Number of customer service requests White sugar Brown sugar Powdered sugar Total The activity-base usage quantities and units produced for the three products were determined from corporate records and are as follows: 3,120 1,990 1,990 7,100 Number Number of…arrow_forwardexample paper for this weeks individual project This list contains costs that various organizations incur; they fall into three categories: direct materials (DM), direct labor (DL), or overhead (OH). Classify each of these items as direct materials, direct labor, or overhead, and provide the rationale for your classification decision. Glue used to attach labels to bottles containing a patented medicine. Compressed air used in operating paint sprayers for Student Painters, a company that paints houses and apartments. Insurance on a factory building and equipment. A production department supervisor’s salary. Rent on factory machinery. Iron ore in a steel mill. Oil, gasoline, and grease for forklift trucks in a manufacturing company’s warehouse. Services of painters in building construction. Cutting oils used in machining operations. Cost of paper towels in a factory employees’ washroom. Payroll taxes and fringe benefits related to direct labor. The plant electricians’ salaries. Crude…arrow_forward

- please answer within the format by providing formula the detailed workingPlease provide answer in text (Without image)Please provide answer in text (Without image)Please provide answer in text (Without image) Question Content Area Activity rates and product costs using activity-based costing Idris Inc. manufactures entry and dining room lighting fixtures. Five activities are used in manufacturing the fixtures. These activities and their associated budgeted activity costs and activity bases are as follows: Activity BudgetedActivity Cost Activity Base Casting $640,000 Machine hours Assembly 125,000 Direct labor hours Inspecting 30,000 Number of inspections Setup 28,000 Number of setups Materials handling 20,000 Number of loads Corporate records were obtained to estimate the amount of activity to be used by the two products. The estimated activity-base usage quantities and units produced follow: Activity Base Entry Dining Total Machine hours 7,500 12,500 20,000…arrow_forwardJoseph Fox, controller of Thorpe Company, has been in charge of a project to install an activity-based cost management system. This new system is designed to support the companys efforts to become more competitive. For the past six weeks, he and the project committee members have been identifying and defining activities, associating workers with activities, and assessing the time and resources consumed by individual activities. Now, he and the project committee are focusing on three additional implementation issues: (1) identifying activity drivers, (2) assessing value content, and (3) identifying cost drivers (root causes). Joseph has assigned a committee member the responsibilities of assessing the value content of five activities, choosing a suitable activity driver for each activity, and identifying the possible root causes of the activities. Following are the five activities with possible activity drivers: The committee member ran a regression analysis for each potential activity driver, using the method of least squares to estimate the variable and fixed cost components. In all five cases, costs were highly correlated with the potential drivers. Thus, all drivers appeared to be good candidates for assigning costs to products. The company plans to reward production managers for reducing product costs. Required: 1. What is the difference between an activity driver and a cost driver? In answering the question, describe the purpose of each type of driver. 2. For each activity, assess the value content and classify each activity as value-added or non-value-added (justify the classification). Identify some possible root causes of each activity, and describe how this knowledge can be used to improve activity performance. For purposes of discussion, assume that the value-added activities are not performed with perfect efficiency. 3. Describe the behavior that each activity driver will encourage, and evaluate the suitability of that behavior for the companys objective of becoming more competitive.arrow_forwardHealthway uses a process-costing system to compute the unit costs of the minerals that it produces. It has three departments: Mixing, Tableting, and Bottling. In Mixing, at the beginning of the process all materials are added and the ingredients for the minerals are measured, sifted, and blended together. The mix is transferred out in gallon containers. The Tableting Department takes the powdered mix and places it in capsules. One gallon of powdered mix converts to 1,600 capsules. After the capsules are filled and polished, they are transferred to Bottling where they are placed in bottles, which are then affixed with a safety seal and a lid and labeled. Each bottle receives 50 capsules. During July, the following results are available for the first two departments (direct materials are added at the beginning in both departments): Overhead in both departments is applied as a percentage of direct labor costs. In the Mixing Department, overhead is 200 percent of direct labor. In the Tableting Department, the overhead rate is 150 percent of direct labor. Required: 1. Prepare a production report for the Mixing Department using the weighted average method. Follow the five steps outlined in the chapter. Round unit cost to three decimal places. 2. Prepare a production report for the Tableting Department. Materials are added at the beginning of the process. Follow the five steps outlined in the chapter. Round unit cost to four decimal places.arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning