Concept explainers

Videos

T accounts,

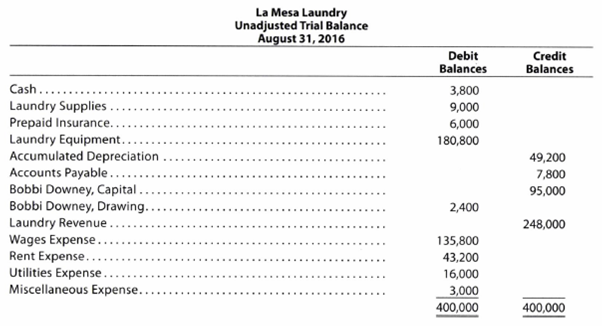

The unadjusted

The data needed to determine year-end adjustments are as follows:

a. Wages accrued but not paid at August 31 are $2,200.

b.

c. Laundry supplies on hand at August 31 are $2,000.

d. Insurance premiums expired during the year are $5,300.

Instructions

1. For each account listed in the unadjusted trial balance, enter the balance in a T account. Identify the balance as “Aug. 31 Bal.” In addition, add T accounts for Wages Payable, Depreciation Expense, Laundry Supplies Expense, Insurance Expense, and Income Summary.

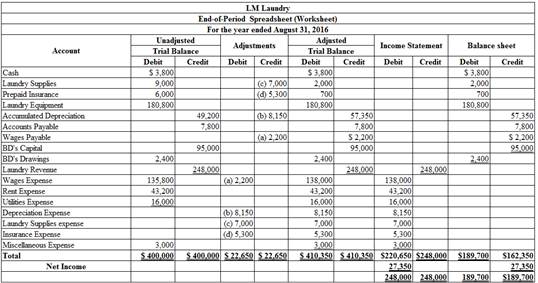

2. (Optional) Enter the unadjusted trial balance on an end-of-period spreadsheet and complete the spreadsheet. Add the accounts listed in part (1) as needed.

3. Journalize and post the adjusting entries. Identify the adjustments by “Adj.” and the new balances as “Adj. Bal.”

4. Prepare an adjusted trial balance.

5. Prepare an income statement, a statement of owner's equity (no additional investments were made during the year), and a balance sheet.

6. Journalize and

7. Prepare a post-closing trial balance.

1, 3, and 6

Journal:

Journal is the book of original entry. Journal consists of the day-to-day financial transactions in a chronological order. The journal has two aspects; they are debit aspect and the credit aspect.

T-Accounts:

T-accounts are referred as T-account because its format represents the letter “T”. The T-accounts consists of the following:

- The title of accounts.

- The debit side (Dr) and,

- The credit side (Cr).

Adjusted trial balance:

The unadjusted trial balance is the summary of all the ledger accounts that appears on the ledger accounts before making adjusting journal entries.

Adjusting entries:

An adjusting entry is prepared when the trial balance is not up-to-date, and complete, and they are usually prepared at the end of the accounting period. This adjusting entry is essential for preparing the financial statements of the business.

Spreadsheet:

A spreadsheet is a worksheet. It is used while preparing a financial statement. It is a type of form having multiple columns and it is used in the adjustment process. The use of a worksheet is optional for any organization. A worksheet can neither be considered as a journal nor a part of the general ledger.

Statement of owners’ equity:

This statement reports the beginning owner’s equity and all the changes, which led to ending owners’ equity. Additional capital, net income from income statement is added to and drawing is deducted from beginning owner’s equity to arrive at the end result, ending owner’s equity.

Income statement:

An income statement is one of the financial statements which shows the revenues, and expenses of the company. The income statement is prepared to ascertain the net income/loss of the company, by deducting the expenses from the revenues.

Balance sheet:

A balance sheet is a financial statement consists of the assets, liabilities, and the stockholder’s equity of the company. The balance of the assets account must be equal to that of the liabilities and the stockholder’s equity account.

Closing entries:

Closing entries are recorded in order to close the temporary accounts such as incomes and expenses by transferring them to the permanent accounts. It is passed at the end of the accounting period, to transfer the final balance.

Post-Closing Trial Balance:

After passing all the journal entries and the closing entries of the permanent accounts and then further posting them to each of the respective accounts, a post-closing trial balance is prepared which consists of a list of all the permanent accounts. A post-closing trial balance serves as an evidence to prove that the balance of the permanent accounts is equal.

To prepare: The T-accounts.

Explanation of Solution

Record the transactions directly in their respective T-accounts, and determine their balances.

| Cash | |||||||||||

| August 31 | Balance | 3,800 | |||||||||

| Laundry Supplies | |||||||||||

| August 31 | Balance | 9,000 | August 31 | Adjusted | 7,000 | ||||||

| August 31 | Adjusted balance | 2,000 | |||||||||

| Prepaid Insurance | |||||||||||

| August 31 | Balance | 6,000 | August 31 | Adjusted | 5,300 | ||||||

| Adjusted balance | 700 | ||||||||||

| Laundry Equipment | |||||||||||

| August 31 | Balance | 180,800 | |||||||||

| Accumulated Depreciation | |||||||||||

| August 31 | Balance | 49,200 | |||||||||

| August 31 | Adjusted | 8,150 | |||||||||

| August 31 | Adjusted balance | 57,350 | |||||||||

| Accounts Payable | |||||||||||

| August 31 | Balance | 7,800 | |||||||||

| Wages Payable | |||||||||||

| August 31 | Adjusted | 2,200 | |||||||||

| BD, Capital | |||||||||||

| August 31 | Closing | 2,400 | August 31 | Balance | 95,000 | ||||||

| August 31 | Closing | 27,350 | |||||||||

| August 31 | Balance | 119,950 | |||||||||

| BD, Drawing | |||||||||||

| August 31 | Balance | 2,400 | August 31 | Closing | 2,400 | ||||||

| Laundry Revenue | |||||||||||

| August 31 | Closing | 248,000 | August 31 | Balance | 248,000 | ||||||

| Wages Expense | |||||||||||

| August 31 | Balance | 135,800 | August 31 | Closing | 138,000 | ||||||

| August 31 | Adjusted | 2,200 | |||||||||

| August 31 | Adjusted balance | 138,000 | |||||||||

| Rent Expense | |||||||||||

| August 31 | Balance | 43,200 | August 31 | Closing | 43,200 | ||||||

| Utilities Expense | |||||||||||

| August 31 | Balance | 16,000 | August 31 | Closing | 16,000 | ||||||

| Depreciation Expense | |||||||||||

| August 31 | Adjusted | 8,150 | August 31 | Closing | 8,150 | ||||||

| Laundry Supplies Expense | |||||||||||

| August 31 | Adjusted | 7,000 | August 31 | Closing | 7,000 | ||||||

| Insurance Expense | |||||||||||

| August 31 | Adjusted | 5,300 | August 31 | Closing | 5,300 | ||||||

| Miscellaneous Expense | |||||||||||

| August 31 | Balance | 3,000 | August 31 | Closing | 3,000 | ||||||

Table (1)

2.

To enter: The unadjusted trial balance on an end-of-period spreadsheet, and complete the spreadsheet.

Explanation of Solution

Table (2)

Hence, the unadjusted trial balance on an end-of-period spreadsheet is prepared and completed.

3.

To Journalize and post: The adjusting entries.

Explanation of Solution

| Date | Description | Debit ($) | Credit ($) | |

| 2016 | Wages expense | 2,200 | ||

| August | 31 | Wages payable | 2,200 | |

| (To record the wages accrued) | ||||

Table (3)

- Wages expense is an expense account, and it is increased. Hence, debit the wages expense account by $2,200.

- Wages payable is a liability account, and it is increased. Hence, credit the wages payable account by $2,200.

| Date | Description | Debit ($) | Credit ($) | |

| 2016 | Depreciation expense | 8,150 | ||

| August | 31 | Accumulated depreciation | 8,150 | |

| (To record the equipment depreciation) | ||||

Table (4)

- Depreciation expense is an expense account, and it is increased. Hence, debit the wages expense account by $8,150.

- Accumulated depreciation is a contra asset account, and it is increased. Hence, credit the accumulated depreciation account by $8,150.

| Date | Description | Debit ($) | Credit ($) | |

| 2016 | Laundry supplies expense | 7,000 | ||

| August | 31 | Laundry supplies |

7,000 | |

| (To record the equipment depreciation) | ||||

Table (5)

- Laundry supplies expense is an expense account, and it is increased. Hence, debit the laundry supplies expense account by $7,000.

- Laundry supplies are the asset account, and it is increased. Hence, credit the laundry supplies account by $7,000.

| Date | Description | Debit ($) | Credit ($) | |

| 2016 | Insurance expense | 5,300 | ||

| August | 31 | Prepaid insurance |

5,300 | |

| (To record the equipment depreciation) | ||||

Table (6)

- Insurance expense is an expense account, and it is increased. Hence, debit the insurance expense account by $5,300.

- Prepaid insurance is an asset account, and it is decreased. Hence, credit the prepaid insurance account by $5,300.

4.

To prepare: An unadjusted trial balance for Laundry LM, as of August 31, 2016.

Explanation of Solution

Prepare an unadjusted trial balance for Laundry LM, as of August 31, 2016.

| Laundry LM | ||

| Unadjusted Trial Balance | ||

| August 31, 2016 | ||

| Accounts | Debit Balances | Credit Balances |

| Cash | 3,800 | |

| Laundry Supplies | 2,000 | |

| Prepaid Insurance | 700 | |

| Laundry Equipment | 180,800 | |

| Accumulated depreciation | 57,350 | |

| Accounts payable | 7,800 | |

| Wages Payable | 2,200 | |

| BD, Capital | 95,000 | |

| BD, Drawing | 2,400 | |

| Laundry revenue | 248,000 | |

| Wages expense | 138,000 | |

| Rent expense | 43,200 | |

| Utilities Expense | 16,000 | |

| Depreciation Expense | 8,150 | |

| Laundry supplies expense | 7,000 | |

| Insurance Expense | 5,300 | |

| Miscellaneous Expense | 3,000 | |

| $410,350 | $410,350 | |

Table (7)

5.

The net income or net loss of Laundry LM for the month of August.

Answer to Problem 4.3BPR

Prepare the balance sheet of LM Laundry at August 31, 2016.

| LM Laundry | ||

| Balance Sheet | ||

| For the year ended August 31, 2016 | ||

| Assets | ||

| Current Assets: | ||

| Cash | $3,800 | |

| Laundry Supplies | 2,000 | |

| Prepaid Insurance | 700 | |

| Total Current Assets | $6,500 | |

| Property, plant and equipment: | ||

| Laundry equipment | $180,800 | |

| Less: Accumulated Depreciation | 57,350 | |

| Total property, plant, and equipment | 123,450 | |

| Total Assets | $129,950 | |

| Liabilities | ||

| Current Liabilities: | ||

| Accounts Payable | $7,800 | |

| Wages Payable | 2,200 | |

| Total Liabilities | $10,000 | |

| Owner’s Equity | ||

| BD’s capital | 119,950 | |

| Total Liabilities and Owners’ Equity | $129,950 | |

Table (9)

Explanation of Solution

| LM Laundry | ||

| Income Statement | ||

| For the year ended August 31, 2016 | ||

| Particulars | Amount ($) | Amount ($) |

| Revenue: | ||

| Laundry revenue | $248,000 | |

| Expenses: | ||

| Wages Expense | $138,000 | |

| Rent Expense | 43,200 | |

| Utilities Expense | 16,000 | |

| Depreciation Expense | 8,150 | |

| Laundry supplies Expense | 7,000 | |

| Insurance Expense | 5,300 | |

| Miscellaneous Expense | 3,000 | |

| Total Expenses | 220,650 | |

| Net Income | $27,350 | |

Table (7)

Hence, the net income of Laundry LM for the month of August r is $27,350.

6.

To Journalize: The closing entries for LM Laundry.

Answer to Problem 4.3BPR

Closing entry for revenue and expense accounts:

| Date | Accounts title and Explanation | Post Ref. | Debit ($) |

Credit ($) |

| August 31, 2016 | Laundry Revenue | 248,000 | ||

| Income Summary | 248,000 | |||

| (To record the closure of revenues account ) | ||||

| August 31, 2016 | Income Summary | 220,650 | ||

| Wages Expense | 138,000 | |||

| Rent Expense | 43,200 | |||

| Utilities Expense | 16,000 | |||

| Depreciation Expense | 8,150 | |||

| Laundry supplies Expense | 7,000 | |||

| Insurance Expense | 5,300 | |||

| Miscellaneous Expense | 3,000 | |||

| (To close the expenses account. Then the balance amount are transferred to income summary account) | ||||

| August 31, 2016 | Income Summary | 27,350 | ||

| BD’s Capital | 27,350 | |||

| (To close balance of income summary are transferred to owners’ capital account) | ||||

| August 31, 2016 | BD’s Capital | 2,400 | ||

| BD’ Drawing | 2,400 | |||

| (To Close the capital and drawings account) | ||||

Table (4)

Explanation of Solution

- Laundry revenue is revenue account. Since the amount of revenue is closed, and transferred to BD’s capital account. Here, LM Laundry earned an income of $248,000. Therefore, it is debited.

- Wages Expense, Rent Expense, Insurance Expense, Utilities Expense, Laundry Supplies Expense, Depreciation Expense, BD Capital, and Miscellaneous Expense are expense accounts. Since the amount of expenses are closed to Income Summary account. Therefore, it is credited.

- Owner’s capital is a component of owner’s equity. Thus, owners ‘equity is debited since the capital is decreased on owners’ drawings.

- Owner’s drawings are a component of owner’s equity. It is credited because the balance of owners’ drawing account is transferred to owners ‘capital account.

7.

To prepare: The post–closing trial balance of LM Laundry for the month ended August 31, 2016.

Explanation of Solution

Prepare a post–closing trial balance of LM Laundry for the month ended August 31, 2016 as follows:

|

Laundry LM Post-closing Trial Balance August 31, 2016 |

||

| Particulars | Debit $ | Credit $ |

| Cash | 3,800 | |

| Laundry Supplies | 2,000 | |

| Prepaid insurance | 700 | |

| Laundry Equipment | 180,800 | |

| Accumulated depreciation | 57,350 | |

| Accounts payable | 7,800 | |

| Wages payable | 2,200 | |

| BD’s Capital | 119,950 | |

| Total | $187,300 | $187,300 |

Table (5)

The debit column and credit column of the post–closing trial balance are agreed, both having balance of $187,300.

Want to see more full solutions like this?

Chapter 4 Solutions

2 Semester Cengage Now, Warren Accounting

- Prepare adjusting journal entries, as needed, considering the account balances excerpted from the unadjusted trial balance and the adjustment data. A. supplies actual count at year end, $6,500 B. remaining unexpired insurance, $6,000 C. remaining unearned service revenue, $1,200 D. salaries owed to employees, $2,400 E. depreciation on property plant and equipment, $18,000arrow_forwardThe following accounts appear in the ledger of Celso and Company as of June 30, the end of this fiscal year. The data needed for the adjustments on June 30 are as follows: ab.Merchandise inventory, June 30, 54,600. c.Insurance expired for the year, 475. d.Depreciation for the year, 4,380. e.Accrued wages on June 30, 1,492. f.Supplies on hand at the end of the year, 100. Required 1. Prepare a work sheet for the fiscal year ended June 30. Ignore this step if using CLGL. 2. Prepare an income statement. 3. Prepare a statement of owners equity. No additional investments were made during the year. 4. Prepare a balance sheet. 5. Journalize the adjusting entries. 6. Journalize the closing entries. 7. Journalize the reversing entry as of July 1, for the wages that were accrued in the June adjusting entry. Check Figure Net income, 14,066arrow_forwardAssume the following data for Oshkosh Company before its year-end adjustments: Journalize the adjusting entries for the following: a. Estimated customer refunds and allowances b. Estimated customer returnsarrow_forward

- Adjusting and Closing EntriesAccount balances taken from the ledger of Builders’ Supply Corporation on December31, 2013, before adjustment, follow information relating to adjustments on December31, 2013:(a) Allowance for Bad Debts is to be increased to a balance of $3,000.(b) Buildings are depreciated at the rate of 5% per year.(c) Accrued selling expenses are $3,840.(d) There are supplies of $780 on hand.(e) Prepaid insurance relating to 2014 totals $720.(f) Accrued interest on long-term investments is $240.(g) Accrued real estate and payroll taxes are $900.(h) Accrued interest on the mortgage is $480.(i) Income taxes are estimated to be 30% of the income before income taxes.Cash . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 24,000Accounts Receivable . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 72,000Allowance for Bad…arrow_forwardAdjusting and Closing EntriesAccount balances taken from the ledger of Builders’ Supply Corporation on December31, 2013, before adjustment, follow information relating to adjustments on December31, 2013:(a) Allowance for Bad Debts is to be increased to a balance of $3,000.(b) Buildings are depreciated at the rate of 5% per year.(c) Accrued selling expenses are $3,840.(d) There are supplies of $780 on hand.(e) Prepaid insurance relating to 2014 totals $720.(f) Accrued interest on long-term investments is $240.(g) Accrued real estate and payroll taxes are $900.(h) Accrued interest on the mortgage is $480.(i) Income taxes are estimated to be 30% of the income before income taxes.Cash . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 24,000Accounts Receivable . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 72,000Allowance for Bad…arrow_forwardJournalizing adjusting entries and analyzing their effect on the income statement The following data at July 31, 2018, are given for RCO: Depreciation, $600. Prepaid rent expires, $200. Interest expense accrued, $700. Employee salaries owed for Monday through Thursday of a five-day workweek; weekly payroll, $8,000. Unearned revenue earned $1,000. Office supplies used $150. Requirements Journalize the adjusting entries needed on July 31, 2018. Suppose the adjustments made in Requirement 1 were not made. Compute the overall overstatement or understatement of net income as a result of the omission of these adjustments.arrow_forward

- Adjusting and Closing EntriesAccount balances taken from the ledger of Builders’ Supply Corporation on December31, 2013, before adjustment, follow information relating to adjustments on December31, 2013:(a) Allowance for Bad Debts is to be increased to a balance of $3,000.(b) Buildings are depreciated at the rate of 5% per year.(c) Accrued selling expenses are $3,840.(d) There are supplies of $780 on hand.(e) Prepaid insurance relating to 2014 totals $720.(f) Accrued interest on long-term investments is $240.(g) Accrued real estate and payroll taxes are $900.(h) Accrued interest on the mortgage is $480.(i) Income taxes are estimated to be 30% of the income before income taxes.Cash . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 24,000Accounts Receivable . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 72,000Allowance for Bad…arrow_forwardRequired 1. Prepare and complete a 10-column work sheet for fiscal year 2019, starting with the unadjusted trial balance and including adjustments based on these additional facts. a. The supplies available at the end of fiscal year 2019 had a cost of $7,900. b. The cost of expired insurance for the fiscal year is $10,600. c. Annual depreciation on equipment is $7,000. d. The April utilities expense of $800 is not included in the unadjusted trial balance because the bill arrived after the trial balance was prepared. The $800 amount owed needs to be recorded. e. The company’s employees have earned $2,000 of accrued and unpaid wages at fiscal year-end. f. The rent expense incurred and not yet paid or recorded at fiscal year-end is $3,000. g. Additional property taxes of $550 have been assessed for this fiscal year but have not been paid or recorded in the accounts. h. The $300 accrued interest for April on the long-term notes payable has not yet been paid or recorded. 2. Using information…arrow_forwardSafety First Company completed all of its October 31,2020 adjustments in preparation for preparing its financial statements which resulted in the following trial balance Other information: All accounts have normal balances $26,400 of the Notes payable balance is due by October 31, 2021 The final task in the year end process was to access the assets for impairment, which resulted in the following schedule Required: Prepare the entries to record any impairment losses at October 31, 2020. Assume the company recorded no impairment losses in the previous years Prepare a classified balance sheet at October 31, 2020 What is the impact on the financial statements of an impairment loss?arrow_forward

- vd subject-Accounting EnviroWaste’s year-end is December 31. The information in (a) to (e) is available at year-end for the preparation of adjusting entries: Of the $17,600 balance in Unearned Revenue, $2,600 remains unearned. The annual building depreciation is $13,700. The Spare Parts Inventory account shows an unadjusted balance of $1,020. A physical count reveals a balance on hand of $890. Unbilled and uncollected services provided to customers totalled $13,700. The utility bill for the month of December was received but is unpaid; $1,200. The accrued revenues of $13,700 recorded in (d) were collected on January 4, 2024. The $1,200 utility bill accrued in (e) was paid on January 14, 2024. Required: Prepare the required adjusting entries at December 31, 2023, for (a) to (e) and the subsequent cash entries required for (f) and (g).arrow_forwardInstructions: Prepare an Income Statement. Your guide is the new ending balance after adjustments for each account. Additional Information a. Physical count of unused supplies on December 31 were conducted and amounted to P900. b. Equipment is being depreciated over a 10 year period without salvage value. The equipment was purchased two years ago. c. Prepaid rent reflected in the unadjusted trial balance was paid on September 1 to cover six-month period. d. Last two-week salary at P2,750 per week for the month of December will be paid on January 3 of the following year. e. The balance of unearned fees at December 31 should be P5,500. f. Lopez additional fee of P12,250 from his last client was still unrecorded and remained uncollected at year-end.arrow_forwarda. Unrecorded depreclation on the trucks at the end of the year is $9,054. b. The total amount of accrued Interest expense at year-end is $8.000. c. The cost of unused office supplies still avallable at year-end is $1,500. 1. Use the above Information about the company's adjustments to complete a 10-column work sheet. 2a. Prepare the year-end closing entries for Dylan Delivery Company as of December 31. 2b. Determine the capital amount to be reported on the December 31, balance sheet. Note: S. Dylan, Capital was $129,560 on December 31 of the prior year. Complete this question by entering your answers in the tabs below. Req 1 Req 2A Req 28 Use the above information about the company's adjustments to complete a 10-column work sheet. DYLAN DELIVERY COMPANY Work Sheet For Year Ended December 31 Adjusted Trial Balance Balance Sheet and Statement of Owner's Equity Unadjusted Trial Balance Adjustments Income Statement Account Title Dr Cr Dr Cr Dr Cr Dr Cr Dr Cr Cash 16,500 S 17,500 17,500…arrow_forward

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage

Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning