Concept explainers

Videos

Recording

North Star prepared the following unadjusted trial balance at the end of its second year of operations ending December 31.

| Account Titles | Debit | Credit |

| Cash | $12,000 | |

| Accounts Receivable | 6,000 | |

| Prepaid Rent | 2,400 | |

| Equipment | 21.000 | |

| Depreciation—Equipment |

$ 1,000 | |

| Accounts Payable | 1.000 | |

| Income Tax Pavable | 0 | |

| Common Stock | 24,800 | |

| 2,100 | ||

| Sales Revenue | 50.000 | |

| Salaries and Wages Expense Utilities Expense | 25,000 12.500 |

|

| Rent Expense | 0 | |

| Depreciation Expense Income Tax Expense | 0 0 |

|

| Totals | 578,900 | 578,900 |

Other data not yet recorded at December 31:

- a. Rent expired during the year, $1,200.

- b. Depreciation expense for the year, $ 1,000.

- c. Utilities owing, $9,000.

- d. Income tax expense, $390.

Required:

- 1. Using the format shown in the demonstration case, indicate the

accounting equation effects o each required adjustment. - 2. Prepare the adjusting

journal entries required at December 31. - 3. Summarize the adjusting journal entries in T-accounts. After entering the beginning balances and computing the adjusted ending balances, prepare an adjusted trial balance as o December 31.

- 4. Compute the amount of net income using (a) the preliminary (unadjusted) numbers, and (b) the final (adjusted) numbers. Had the adjusting entries not been recorded, would net income have been overstated or understated, and by what amount?

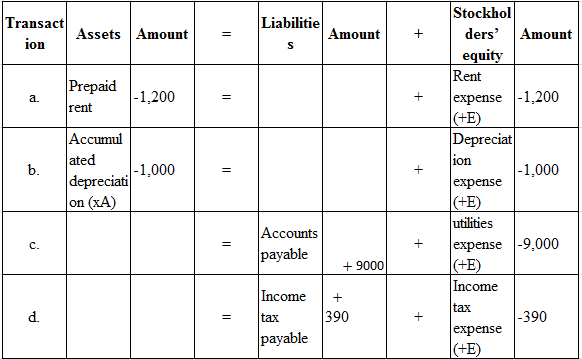

1.

Answer to Problem 15E

Following are the effects of accounting equation on the adjusting journal entries.

Figure (1)

Note:

E represents expenses

xA represents contra asset

Explanation of Solution

Accounting equation:

Accounting equation is an accounting tool expressed in the form of equation, by creating a relationship between the resources or assets of a company, and claims on the resources by the creditors and the owners. Accounting equation is expressed as shown below:

a.

- Prepaid rent is an asset. There is a decrease in the asset. Hence, the asset will be decreased by $1,200.

- Prepaid rent is an asset. Hence, there is no effect on liability account.

- Rent expense is an expense account which is a component of stockholders’ equity. There is an increase in the expense account which decreases the stockholders’ equity. Hence, the stockholders’ equity will be decreased by $1,200.

b.

- Accumulated depreciation is a contra asset. There is a decrease in the asset. Hence, the asset account will be decreased by $1,000.

- Accumulated depreciation is a contra asset. Hence, there is no effect on liability account.

- Depreciation expense is an expense account which is a component of stockholders’ equity. There is an increase in the expense account which decreases the stockholders’ equity. Hence, the stockholders’ equity is decreased by $1,000.

c.

- Accounts payable is a liability. Hence, there is no effect on the asset account.

- Accounts payable is a liability. There is an increase in the liability. Hence, the liability account will be increased by $9,000.

- Utilities expense is an expense account which is a component of stockholders’ equity. There is an increase in the expense account which decreases the stockholders’ equity. Hence, the stockholders’ equity will be decreased by $9,000.

d.

- Income tax payable is a liability. Hence, there is no effect on the asset account.

- Income tax payable is a liability. There is an increase in liability. Hence, the liability account will be increased by $390.

- Income tax expense is an expense account which is a component of stockholders’ equity. There is an increase in the expense account which decreases the stockholders’ equity. Hence, the stockholders’ equity is decreased by $390.

2.

To prepare: Adjusting journal entry required for each item at December 31.

Answer to Problem 15E

Prepare adjusted journal entries for each item at June 30:

| Date | Account Title and Explanation | Debit ($) | Credit ($) | |

| Rent expense (+E, -SE) (1) | 1,200 | |||

| Prepaid rent (-A) | 1,200 | |||

| (To record the adjusting entry for Rent expense) | ||||

| Depreciation expense (+E, -SE) | 1,000 | |||

| Accumulated Depreciation-Equipment(+xA, -A) | 1,000 | |||

| (To record adjusting entry for depreciation expense) | ||||

| Utilities expense (+E, -SE) | 9,000 | |||

| Accounts payable(+L) | 9,000 | |||

| (To record the adjusting entry for utilities expenses) | ||||

| Income tax expense(+E, -SE) | 390 | |||

| Income tax payable(+L) | 390 | |||

| (To record the adjusting entry for income tax expense) | ||||

a.

b.

c.

d.

Table (1)

Explanation of Solution

Adjusting entries:

Adjusting entries are the journal entries which are recorded at the end of the accounting period to correct or adjust the revenue and expense accounts, to concede with the accrual principle of accounting.

a.

- Prepaid rent is an asset and it increases. Hence, debit prepaid expenses account with $1,200.

- Cash is an asset and it decreases. Hence, credit cash account with $1,200.

b.

- Depreciation expense is an expense which is the component of stockholders’ equity. There is an increase in expense account which decreases the stockholders’ equity. Hence, debit Depreciation expense with $1,000.

- Accumulated depreciation is a contra asset. There is a decrease in the asset. Hence, credit the asset account by $1,000.

c.

- Utilities expense is an expense which is a component of stockholders’ equity. There is an increase in the expense account which decreases the stockholders’ equity. Hence, debit the utilities expense by $9,000.

- Accounts payable is a liability. There is an increase in the liability. Hence, credit the accounts payable account by $9,000.

d.

- Income tax expense is an expense which is a component of stockholders’ equity. There is an increase in the expense account which decreases the stockholders’ equity. Hence, debit the income tax expense by $390.

- Income tax payable is a liability. There is an increase in liability. Hence, credit the income tax payable account by $390.

3.

To Summarize: The adjusting journal entries in T-accounts after the beginning balances and computing the adjusted ending balances, and to prepare the adjusted trial balance as of December 31.

Explanation of Solution

T-account:

T-account refers to an individual account, where the increases or decreases in the value of specific asset, liability, stockholder’s equity, revenue, and expenditure items are recorded.

This account is referred to as the T-account, because the alignment of the components of the account resembles the capital letter ‘T’. An account consists of the three main components which are as follows:

(a)The title of the account

(b)The left or debit side

(c)The right or credit side

Post the adjusted entries in T-account:

| Prepaid rent (A) account | |||

| Balance | 2,400 | ||

| a | 1,200 | ||

| Ending balance | 1,200 | ||

|

Rent expense (E) account |

|||

| Balance | 0 | ||

| a | 1,200 | ||

| Ending balance | 1,200 | ||

| Accumulated DepreciationEquipment -(xA) account | |||

| Balance | 1,000 | ||

| b | 1,000 | ||

| Ending balance | 2,000 | ||

|

Depreciation expense (E) account |

|||

| Balance | 0 | ||

| b | 1,000 | ||

| Ending balance | 1,000 | ||

|

Accounts payable (L) account |

|||

| Balance | 1,000 | ||

| c | 9,000 | ||

| Ending balance | 10,000 | ||

|

Utilities expense(E) account |

|||

| Balance | 12,500 | ||

| c | 9,000 | ||

| Ending balance | 21,500 | ||

|

Income tax payable (L) account |

|||

| Balance | 0 | ||

| d | 390 | ||

| Ending balance | 390 | ||

| Income tax expense(E) account | |||

| Balance | 0 | ||

| d | 390 | ||

| Ending balance | 390 | ||

Prepare adjusted trial balance as of December 31:

| Company NS | ||

| Adjusted Trial balance | ||

| As of December 31 | ||

| Account Titles | Debit ($) | Credit ($) |

| Cash | 12,000 | |

| Accounts Receivable | 6,000 | |

| Prepaid Rent | 1,200 | |

| Equipment | 21,000 | |

| Accumulated Depreciation–Equipment | 2,000 | |

| Accounts Payable | 10,000 | |

| Income Taxes Payable | 390 | |

| Common Stock | 24,800 | |

| Retained Earnings | 2,100 | |

| Sales Revenue | 50,000 | |

| Salaries and Wages Expense | 25,000 | |

| Utilities Expense | 21,500 | |

| Rent Expense | 1,200 | |

| Depreciation Expense | 1,000 | |

| Income Tax Expense | 390 | |

| Totals | $ 89,290 | $ 89,290 |

Table (2)

4.

To Compute: The amount of net income using (a) the preliminary (unadjusted) numbers, and (b) the final (adjusted) numbers and to state without adjustments would net income have been overstated or understated and by what amount.

Explanation of Solution

- (a) Calculation of preliminary net income:

- (b) Calculation of adjusted net income:

Calculation of overstated preliminary net income:

Without adjustments, preliminary net income would have been overstated by $11,590.

Want to see more full solutions like this?

Chapter 4 Solutions

FUNDAMENTALS OF FINANCIAL ACCOUNTING

- Casebolt Company wrote off the following accounts receivable as uncollectible for the first year of its operations ending December 31: a. Journalize the write-offs under the direct write-off method. b. Journalize the write-offs under the allowance method. Also, journalize the adjusting entry for uncollectible accounts. The company recorded 5,250,000 of credit sales during the year. Based on past history and industry averages, % of credit sales are expected to be uncollectible. c. How much higher (lower) would Casebolt Companys net income have been under the direct write-off method than under the allowance method?arrow_forwardAs Perry Materials Supply was preparing for the year-end close, their balances were as follows: Accounts Receivable - $146000 (dr) Allowance for uncollectible accounts - $6200 (dr) Uncollected Account Expense - $0 Perry Materials uses the aging method and has completed the following analysis of the accounts receivable: Customer 1-30 Days 31-60 Days 61-90 Days Over 90 Days Total Balance Johnson $4,600 $3,200 $7,800 Hot Pots, Inc. 800 1,000 1,800 Potter 40,000 550 40,550 Harrison 3,600 900 4,500 Marx 2,000 50 2,050 Younger 65,000 65,000 Merry Maids 5,900 5,900 Acher 12,000 6,400 18,400 Totals $127,500 $13,750 $3,700 $1,050 $146,000 Uncollectible percentage 2% 10% 20% 40% Estimated uncollectible amount $2,550 $1,375 $740 $420 $5,085 Required: How much will the…arrow_forwardTaylor R incorporation reported the following balances after adjustment at the end of 2020 and 2019. total accounts receivable 2020 100,000 2019 95,000 net accounts receivable 2020 75,000 2019 85,000 During 2020 Taylor road of customer accounts, totaling 3000 and collected 750 on accounts written off In previous years, tailors doubtful accounts expense for the year ending December 3120 20 Isarrow_forward

- Required information Skip to question [The following information applies to the questions displayed below.] At December 31, Hawke Company reports the following results for its calendar year. Cash sales $ 640,000 Credit sales $ 1,600,000 In addition, its unadjusted trial balance includes the following items. Accounts receivable $ 480,000 debit Allowance for doubtful accounts $ 5,800 debit Required:1. Prepare the adjusting entry to record bad debts under each separate assumption. Bad debts are estimated to be 2% of credit sales. Bad debts are estimated to be 1% of total sales. An aging analysis estimates that 6% of year-end accounts receivable are uncollectible.arrow_forwardAccounting for Assets: Receivables Johnson company's financial year ended on December 31, 201o. All the transactions related to the company's uncollectible accounts are can be found below: Wrote of $44o account of Miller Company as uncollectible January 15 Re-establish the account of Louisa April 2nd Teller and record the collection of $1,050 as payment in full for her account which had been written off earlier Received 40% of the $700 balance owed by William John and wrote off the remainder as uncollectible July 31 Wrote off as uncollectible the accounts of Sherwin Company, $1,700 and V. Vasell $2,200 Received 25% of the $1,140 owed by Grant Company and wrote off the remainder as uncollectible August 15 September 26 Received $741 from M. Fuller in full payment of his account which had been written off earlier as uncollectible Estimated uncollectible accounts October 16 expense for the year to be 1.5% of net credit sales of $521,000 December 31 The accounts receivable account had a…arrow_forwardAccounting for Assets: Receivables Johnson company’s financial year ended on December 31, 2010. All the transactions related to the company’s uncollectible accounts are can be found below: January 15 Wrote of $440 account of Miller Company as uncollectible April 2nd Re-establish the account of Louisa Teller and record the collection of $1,050 as payment in full for her account which had been written off earlier July 31 Received 40% of the $700 balance owed by William John and wrote off the remainder as uncollectible August 15 Wrote off as uncollectible the accounts of Sherwin Company, $1,700 and V. Vasell $2,200 September 26 Received 25% of the $1,140 owed by Grant Company and wrote off the remainder as uncollectible October 16 Received $741 from M. Fuller in full payment of his account which had been written off earlier as uncollectible December 31 Estimated uncollectible accounts expense for the year to be 1.5% of net credit sales…arrow_forward

- The unadjusted trial balance of Fortune Company included the following accounts: Debit $ Sales (80% on credit) for the year ended 31 Dec 2023 Credit $ 900,500 Accounts Receivable 31 Dec 2023 209,070 Allowance for Impairment 1 Jan 2023 3,500 The aging of accounts receivable produced the following five groupings. Days Past Due Amount Estimated Uncollectible % of Not yet due 85,000 1% 1-30 days past due 56,000 3% 31-60 days past due 33,500 5% 61-90 days past due 18,570 10% Over 90 days past due 16,000 15% Required: Prepare the adjusting entries to record the impairment loss of receivable for the year 2023. If Fortune Company: (a) (b) uses the Statement of Financial Position Approach to estimate the uncollectible accounts. Show your workings. uses the Income Statement Approach to estimate the uncollectible accounts, and it is expected that 1% of the net credit sales for the year will be uncollectible.arrow_forwardAccounting for Assets: Receivables Johnson company’s financial year ended on December 31, 2010. All the transactions related to the company’s uncollectible accounts are can be found below: January 15 Wrote of $440 account of Miller Company as uncollectible April 2nd Re-establish the account of Louisa Teller and record the collection of $1,050 as payment in full for her account which had been written off earlier July 31 Received 40% of the $700 balance owed by William John and wrote off the remainder as uncollectible August 15 Wrote off as uncollectible the accounts of Sherwin Company, $1,700 and V. Vasell $2,200 September 26 Received 25% of the $1,140 owed by Grant Company and wrote off the remainder as uncollectible October 16 Received $741 from M. Fuller in full payment of his account which had been written off earlier as uncollectible December 31 Estimated uncollectible accounts expense for the year to be 1.5% of net credit sales…arrow_forwardAnalysis of Receivables Method At the end of the current year, Accounts Receivable has a balance of $630,000; Allowance for Doubtful Accounts has a debit balance of $5,500; and sales for the year total $2,840,000. Using the aging method, the balance of Allowance for Doubtful Accounts is estimated as $25,400. a. Determine the amount of the adjusting entry for uncollectible accounts. 22,900 X b. Determine the adjusted balances of Accounts Receivable, Allowance for Doubtful Accounts, and Bad Debt Expense. Accounts Receivable Allowance for Doubtful Accounts Bad Debt Expense c. Determine the net realizable value of accounts receivable. 601,200 X Feedback 630,000 ✓ 28,400 X 22,900 X Check My Work The analysis of receivables method is based on the assumption that the longer an account receivable is outstanding the less likely that it will be collected. The amount of the adjusting entry is the amount that will yield an adjusted balance for Allowance for Doubtful Accounts.arrow_forward

- Hunter, Inc. analyzed its accounts receivable balances at December 31, and arrived at the aged balances listed below, along with the percentage that is estimated to be uncollectible: % Considered Age Group Balance Uncollectible 0-30 days past due $90,000 1% 31-60 days past due 20,000 2% 61-120 days past due 11,000 5% 121-180 days past due 6,000 10% Over 180 days past due 4,000 25% $131,000 The company handles credit losses using the allowance method. The credit balance of the Allowance for Doubtful Accounts is $520 on December 31, before any adjustments. a. Determine the amount of the adjustment for estimated credit losses on December 31. $ 0 b. Determine the financial statement effect of a write off of the Rose Company's account on April 10 of the following year in the amount of $425. Use negative signs with answers, when appropriate. If a transaction increases and decreases the same Balance Sheet category, enter the increase amount in the first row and the decrease amount directly…arrow_forwardEffective the current year, Jeff Company adopted a new accounting method for estimating the allowance for doubtful accounts at the amount indicated by year-end aging of accounts receivable. Allowance for doubtful accounts on January 1, 250,000 Provision for doubtful accounts during the current year (2% of credit sales of P10,000,000) 2,000,000 Accounts written off 205,000 Estimated uncollectible accounts per aging on December 31 220,000 After year-end adjustments, what is the doubtful accounts expense for current year? a. P220,000 b. P205,000 c. P220,000 d. P175,000arrow_forwardprepare these entries for Sarah's plant services. prepare general journal entries for the needed balance dy adjustments for the year ending 30/6/21: A stocktake of the inventory on hand was completed on 30/6/21. The value of the stocktake was $17,000. The inventory asset account as at 30/6/21 before adjustments was $18.000 The allowance for Doubtful debts should be 5% of the balance of Accounts Receivable. The accounts receivable balance at 30/6/21 is $76,120 and the balance of the Allowance for Doubtful Debts was $3,450arrow_forward

Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage

Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT