Concept explainers

Videos

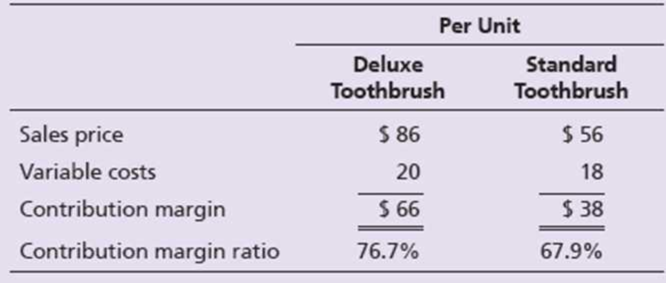

Brinn, located in Port St. Lucie, Florida, produces two lines of electric toothbrushes: deluxe and standard. Because Brinn can sell all the toothbrushes it can produce, the owners are expanding the plant. They are deciding which product line to emphasize. To make this decision, they assemble the following data:

After expansion, the factor will have a production capacity of 4,100 machine hours per month. The plant can manufacture either 50 standard electric toothbrushes or 35 deluxe electric toothbrushes per machine hour.

Requirements

- 1. Identify the constraining factor for Brinn.

- 2. Prepare an analysis to show which product line to emphasize.

Want to see the full answer?

Check out a sample textbook solution

Chapter 25 Solutions

Horngren's Financial & Managerial Accounting, The Managerial Chapters (6th Edition)

Additional Business Textbook Solutions

Horngren's Financial & Managerial Accounting, The Financial Chapters (6th Edition)

Financial Accounting, Student Value Edition (4th Edition)

Managerial Accounting: Creating Value in a Dynamic Business Environment

Fundamentals Of Financial Accounting

Financial Accounting (12th Edition) (What's New in Accounting)

Managerial Accounting (5th Edition)

- Blue Spruce Inc. has two divisions. Division A makes and sells student desks. Division B manufactures and sells reading lamps. Each desk has a reading lamp as one of its components. Division A can purchase reading lamps at a cost of $10 from an outside vendor. Division A needs 8,200 lamps for the coming year. Division B has the capacity to manufacture 41,000 lamps annually. Sales to outside customers are estimated at 32,800 lamps for the next year. Reading lamps are sold at $12 each. Variable costs are $7 per lamp and include $1 of variable sales costs that are not incurred if lamps are sold internally to Division A. The total amount of fixed costs for Division B is $65,600. Consider the following independent situations. (a) What should be the minimum transfer price accepted by Division B for the 8,200 lamps and the maximum transfer price paid by Division A? Minimum transfer price accepted by Division B Maximum transfer price paid by Division A $ $ per unit per unitarrow_forwardCrede Inc. has two divisions. Division A makes and sells student desks. Division B manufactures and sells reading lamps. Each desk has a reading lamp as one of its components. Division A can purchase reading lamps at a cost of $10.10 from an outside vendor. Division A needs 11,100 lamps for the coming year. Division B has the capacity to manufacture 49,600 lamps annually. Sales to outside customers are estimated at 38,500 lamps for the next year. Reading lamps are sold at $12.09 each. Variable costs are $6.87 per lamp and include $1.41 of variable sales costs that are not incurred if lamps are sold internally to Division A. The total amount of fixed costs for Division B is $75,900. Consider the following independent situations. What should be the minimum transfer price accepted by Division B for the 11,100 lamps and the maximum transfer price paid by Division A? (Round answers to 2 decimal places, e.g. 15.25.) Per unit Minimum transfer price accepted by Division B $_ Maximum transfer…arrow_forwardJamuna Group is evaluating the proposal of a new RMG factory called Jamuna Fabrics. Jamuna Group is renting a premise of 50,000 Square feet in Savar and Jamuna Fabrics is planning to use 10,000 Square feet from this facility. The rest of the premise will be used by another RMG factory of Jamuna Group called Jamuna Exclusive Fabrics. From these two factories, Jamuna Group expects to have a total output of 50,000 units of cloths at USD 3 per cloth and Jamuna Fabrics will have 40% of this total output. Total capital cost is USD 20,000 and is depreciated using the straight-line method over five years to a zero-salvage value. The monthly salary expense will be USD 2500, whereas annual utility and other expense will be USD 2,000. The annual total rent of 50,000 Square feet premise is USD 25,000. Jamuna Fabrics will need to annually pay USD 6000 as staff’s festival bonus. Variable costs are 10 per cent of annual sales revenue. Assume, initially you require USD 5,000 in working capital for…arrow_forward

- The process-control division expects to sell 1,250 process-control units this year. From the viewpoint of Sierra Inc. as a whole, should 1,250 Xcel-chips be transferred to the process-control division to replace circuit boards? Show your computations.arrow_forwardThe Sandstone Corporation uses an injection molding machine to make a plastic product, Z35, after receiving firm orders from its customers. Sandstone estimates that it will receive 60 orders for Z35 during the coming year. Each order of Z35 will take 100 hours of machine time. The annual machine capacity is 8,000 hours. Q. Sandstone is considering introducing a new product, Y21. The company expects it will receive 30 orders of Y21 in the coming year. Each order of Y21 will take 40 hours of machine time. Assuming the demand for Z35 will not be affected by the introduction of Y21, calculate (a) the average waiting time for an order received and (b) the average manufacturing cycle time per order for each product, if Sandstone introduces Y21.arrow_forwardPremo Pens, Inc., is in the process of developing a newpen to replace its existing top-of-the-line Executive Model.Market research has identified the critical features the pen must have, and it is estimated that customers would be will-ing to pay $30 for a pen with these features. Premo’s produc-tion manager estimates that with existing equipment it will cost $26 to produce the proposed model. The current Execu-tive Model sells for $24 and has a total production cost of $20. A competitor sells a pen similar to the proposed model,but without Premo’s patented easy retract feature, for $28. Itis estimated to cost the competitor $25 to produce. If Premoseeks to earn a 20 percent return on sales on the new model,which of the following represents the target cost for the newpen?a. $26.00.b. $22.40.c. $24.00.d. $19.80.arrow_forward

- Flounder Inc. has two divisions. Division A makes and sells student desks. Division B manufactures and sells reading lamps. Each desk has a reading lamp as one of its components. Division A can purchase reading lamps at a cost of $10 from an outside vendor. Division A needs 9,000 lamps for the coming year. Division B has the capacity to manufacture 45,000 lamps annually. Sales to outside customers are estimated at 36,000 lamps for the next year. Reading lamps are sold at $12 each. Variable costs are $7 per lamp and include $2 of variable sales costs that are not incurred if lamps are sold internally to Division A. The total amount of fixed costs for Division B is $72,000. Consider the following independent situations.arrow_forwardGermano Products, Incorporated, has a Pump Division that manufactures and sells a number of products, including a standard pump that could be used by another division in the company, the Pool Products Division, in one of its products. Data concerning that pump appear below: Capacity in units 72,500 Selling price to outside customers $ 79 Variable cost per unit $ 28 Fixed cost per unit (based on capacity) $ 32 The Pool Products Division is currently purchasing 17,000 of these pumps per year from an overseas supplier at a cost of $74 per pump. Assume that the Pump Division is selling all of the pumps it can produce to outside customers. Does there exist a transfer price that would make both the Pump and Pool Products Division financially better off than if the Pool Products Division were to continue buying its pumps from the outside supplier?arrow_forwardGuthrie Generators manufactures a solenoid that it uses in several of its products. Management is considering whether to continue manufacturing the solenoids or to buy them from an outside source. The following information is available: 1. The company needs 20,000 solenoids per year. The solenoids can be purchased from an outside supplier at a cost of $15 per unit. 2. The unit cost of manufacturing the solenoids is $20, computed as follows: Direct materials Direct labor Factory overhead: Variable Fixed Total manufacturing costs Cost per unit ($400,000 ÷ 20,000 units) 3. If the company decides not to manufacture the solenoids, it will eliminate all of the raw materials and direct labor costs but only 75 percent of the variable factory overhead costs. 4. If the solenolds are purchased from the outside source, machinery used in the production of solenoids will be sold at its book value. Accordingly, no gain or loss will be recognized. The sale of this machinery would also eliminate $5,000…arrow_forward

- Consider this problem for the next five questions: At Kahel Enterprises, a producer of orange crates sold to growers, they are able to produce 450 crates per 100 logs with their current equipment. They currently purchase 100 logs per day, and each log requires 1.5 labor hours to process. They believe that they can hire a professional buyer who can buy better-quality log at the same cost. If this is the case, they can increase their production to 480 crates per 100 logs. Their total labor hours, on the other hand, will increase by an additional 2 hours per day (this is due to the additional logistics operations needed with the professional buyer). Given below are the cost per component in the system, which includes the labor cost, material cost, capital cost, and energy and utility cost. Component Cost Labor Php 100/labor hour Material (Logs) Php 200/log Capital Php 500 / day Energy & Utility Php 350 / day Question 1: What is the current labor productivity? O 4.5 logs per labor hour O…arrow_forwardConsider this problem for the next five questions: At Kahel Enterprises, a producer of orange crates sold to growers, they are able to produce 450 crates per 100 logs with their current equipment. They currently purchase 100 logs per day, and each log requires 1.5 labor hours to process. They believe that they can hire a professional buyer who can buy better-quality log at the same cost. If this is the case, they can increase their production to 480 crates per 100 logs. Their total labor hours, on the other hand, will increase by an additional 2 hours per day (this is due to the additional logistics operations needed with the professional buyer). Given below are the cost per component in the system, which includes the labor cost, material cost, capital cost, and energy and utility cost. Cost Component Labor Php 100/labor hour Material (Logs) Php 200/log Capital Php 500 / day Energy & Utility Php 350 / day Question 1: What is the current labor productivity? 4.5 crates per labor hour 3…arrow_forwardConsider this problem for the next five questions: At Kahel Enterprises, a producer of orange crates sold to growers, they are able to produce 450 crates per 100 logs with their current equipment. They currently purchase 100 logs per day, and each log requires 1.5 labor hours to process. They believe that they can hire a professional buyer who can buy better-quality log at the same cost. If this is the case, they can increase their production to 480 crates per 100 logs. Their total labor hours, on the other hand, will increase by an additional 2 hours per day (this is due to the additional logistics operations needed with the professional buyer). Given below are the cost per component in the system, which includes the labor cost, material cost, capital cost, and energy and utility cost. Component Cost Labor Php 10/labor hour Material (Logs) Php 200/log Capital Php 500/day Energy & Utility Php 350/day Question 3: What is the current multifactor productivity? O 0.02013 crates per Php O…arrow_forward

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education